Solar (SXP): Background and Timeline (2020–2023)

A factual chronology and contextual record compiled for transparency

Across the communications compiled here, the Foundation repeatedly sought clarity on three things: whether mainnet would be supported, how the treasury would be handled, and whether SXP could be used for card processing fees. Card processing fees alone recur across ten exhibits (A-002, A-003, A-004, A-008, A-009, A-020, A-027, A-030, A-031, A-033).

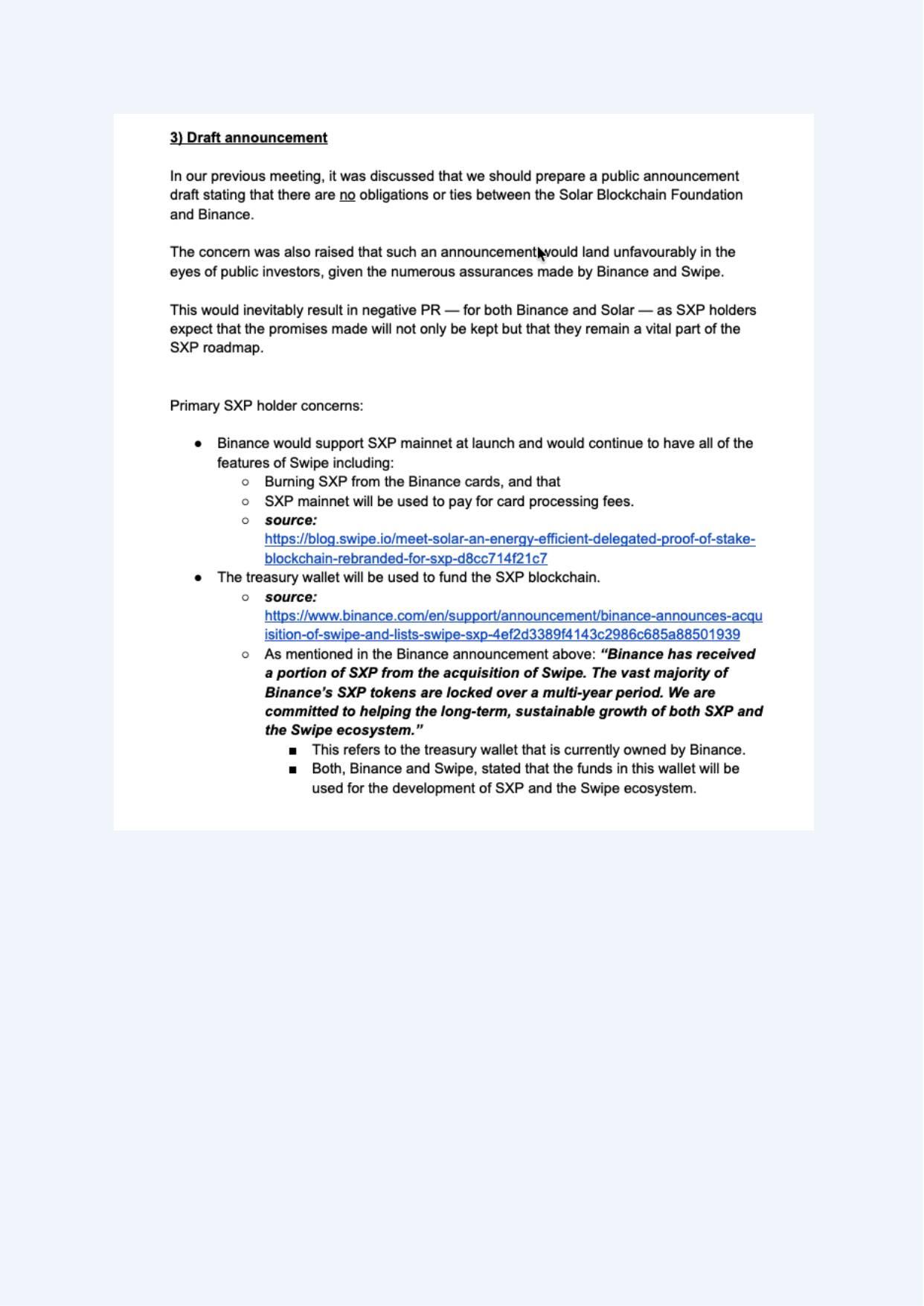

In the Foundation’s assessment of that record: questions about the project, the community, and later Core 5.0 went largely unanswered — while one subject was returned to consistently: the treasury. A public announcement describing the project as “decentralised / community-driven” was sought as a condition tied to mainnet support (Exhibit A-037), and concrete support for the mainnet listing appeared to materialise only after the Foundation signalled it would wind down swap support — at which point the remaining treasury was at stake.

That leads to the concern at the heart of this record: once the entire treasury has been transferred, there is little remaining incentive to keep SXP listed or supported — the tokens could simply be sold. This is the Foundation’s interpretation of the documents below; readers can review the exhibits and form their own view. The other parties have not responded publicly.

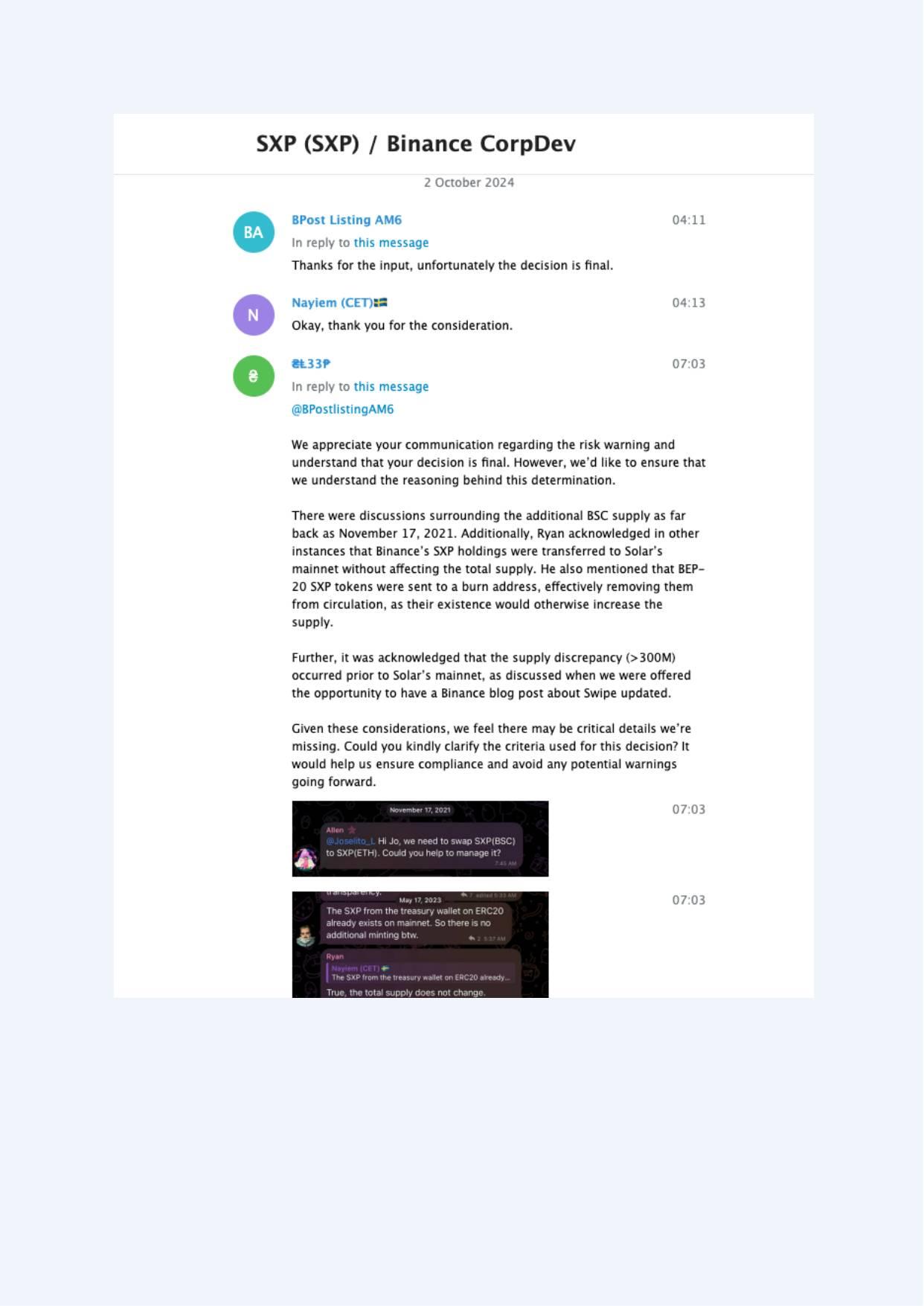

SXP began as one ERC-20 with a 300M hard cap. Today parallel supplies exist across chains: Ethereum ~285.4M, a separate “Binance-Peg” BSC BEP-20 ~289.7M (supply hard-coded, no mint function, deployed 5 Oct 2020 — after the July 2020 acquisition), and native Solar ~684M. The migration was lock-based, not burn-based, so ~575M SXP still exists on Ethereum + BSC alongside the native supply — despite the official “480M, 1:1, supply not increased” line. The existence of this parallel supply is verifiable; attributing it to a deliberate act is the Foundation’s position (Binance has not responded).

Verify: Etherscan · BscScan · api.solar.org · full breakdown in the FAQ.

Disclaimer

This document reflects my personal recollection, understanding, and interpretation of events based on materials available to me. It is not intended to allege wrongdoing, assert legal claims, or provide legal advice. Factual statements are presented to the best of my knowledge, and any evaluative or interpretive statements represent my opinions or assessments derived from those facts.

Background Context: Binance (Pre-2023 and After)

This document provides background context regarding events involving Binance up to mid-2023 that materially affected the Solar project.

By mid-2023, it had become apparent to me that Solar’s engagement with Binance was increasingly constrained, and that the practical scope for resolving outstanding issues through cooperative or informal means was narrowing. Over time, the operating environment evolved in ways that limited Solar’s ability to proceed independently.

Some materials referenced in this document include excerpts and screenshots from historical communications. I recognize that the disclosure of such materials may be viewed as sensitive. However, following an extended period of public criticism — including being labeled a scammer despite continued good-faith efforts — I concluded that continued silence was no longer an effective or fair approach. The purpose of this record is to provide context for decisions made under those circumstances, not to escalate disputes.

Throughout my involvement in prior crypto projects, I have consistently sought to avoid public conflict. My approach has been to focus on delivery, accept responsibility where appropriate, and restore credibility through tangible progress rather than confrontation. I applied the same approach to Solar.

Over time, this approach became increasingly difficult to sustain.

Multiple factors converged, including but not limited to:

constraints affecting card-related initiatives,

unresolved questions regarding control and use of the treasury wallet,

token supply-related complexities, and

limitations on development actions that could proceed without prior approval.

By the time the scope and durability of these constraints became fully clear to me, Solar was already deeply committed. Friends and family had invested in the project, and contributors from other ecosystems had been asked to leave stable employment to work on Solar. Reversing course at that stage would have caused immediate and significant harm to individuals who had placed trust in the project.

In that context, pursuing Core 5.0 represented the least harmful and most constructive path forward. Core 5.0 was conceived as a technical initiative intended to introduce additional utility and flexibility to Solar without reliance on card programs or other components that required external consent. It was designed as a protocol-level effort to restore a degree of operational agency to the network.

When Core 5.0 reached a functional internal testnet stage and was presented to Binance, the response I received was not framed as a technical evaluation. Instead, further progress was conditioned on:

the immediate transfer of the remaining treasury balance,

the removal or bypassing of existing timelock protections, and

execution of an agreement that would place personal liability on me individually rather than on the Solar entity.

Under those proposed terms, I would have assumed personal responsibility for a broad range of risks and obligations, while effective control would have remained external and without corresponding exposure. Based on my assessment, agreeing to those conditions would have undermined user trust, governance credibility, and my own legal position. For those reasons, I declined to proceed.

At that point, continuing under the existing structure was no longer viable. As outlined in my formal communications, I resigned from my executive role and redirected my forward-looking development efforts to Monolythium, an independent project that does not inherit Solar’s assets, governance framework, or obligations.

I acknowledge that publication of this document goes beyond what is strictly required under certain confidentiality arrangements. There exists additional information covering the period from 2023 to 2025 that has not been disclosed publicly. That information is materially more sensitive than what is presented here and will only be provided to regulators or official investigative bodies if formally requested.

Disclosing the full scope of post-2023 agreements and communications publicly would expose me to disproportionate personal and legal risk. I have therefore chosen to limit public disclosure and accept reputational criticism rather than escalate matters in a way that could place myself or others at risk.

Open Letter to the Solar (SXP) Community

This document is intended as a public, community-facing record describing how Solar’s leadership experienced and navigated constraints while attempting to advance Solar (SXP) following Binance’s acquisition of Swipe and its involvement in key areas such as exchange access, treasury custody, and infrastructure dependencies.

This document is not a legal filing and does not constitute legal advice. It is a transparency record: what is supported by documents and screenshots, and what remains uncertain or subject to interpretation.

What Occurred (High-Level Overview)

From 2020 to 2023, Solar (and earlier, Swipe/SXP) engaged with multiple Binance teams — including Research, Corporate Development, and Technical groups — to clarify:

whether SXP would receive sustained mainnet support,

whether SXP would be used for card-related utility and processing fees, and

how token supply and treasury constraints would be handled.

During this period, Binance communications at times referenced Swipe/SXP as part of its acquisition and card ecosystem, while later public messaging described Solar as an independent, community-driven project. At the same time, Solar leadership perceived that Binance retained practical leverage through exchange listings, treasury custody, and infrastructure dependencies.

Key Issues Raised by Solar Leadership (Contextual Summary)

The following points summarize concerns and observations raised internally by Solar leadership, based on available materials and communications:

Exchange listing and delisting considerations were perceived as materially influencing treasury-related decisions and public messaging.

Certain product paths, including card-related initiatives, appeared constrained by ticker and intellectual-property considerations, while public distancing from the project increased.

Public framing shifted from “Binance-acquired Swipe ecosystem” to “independent community-driven project” without full disclosure of continuing operational dependencies.

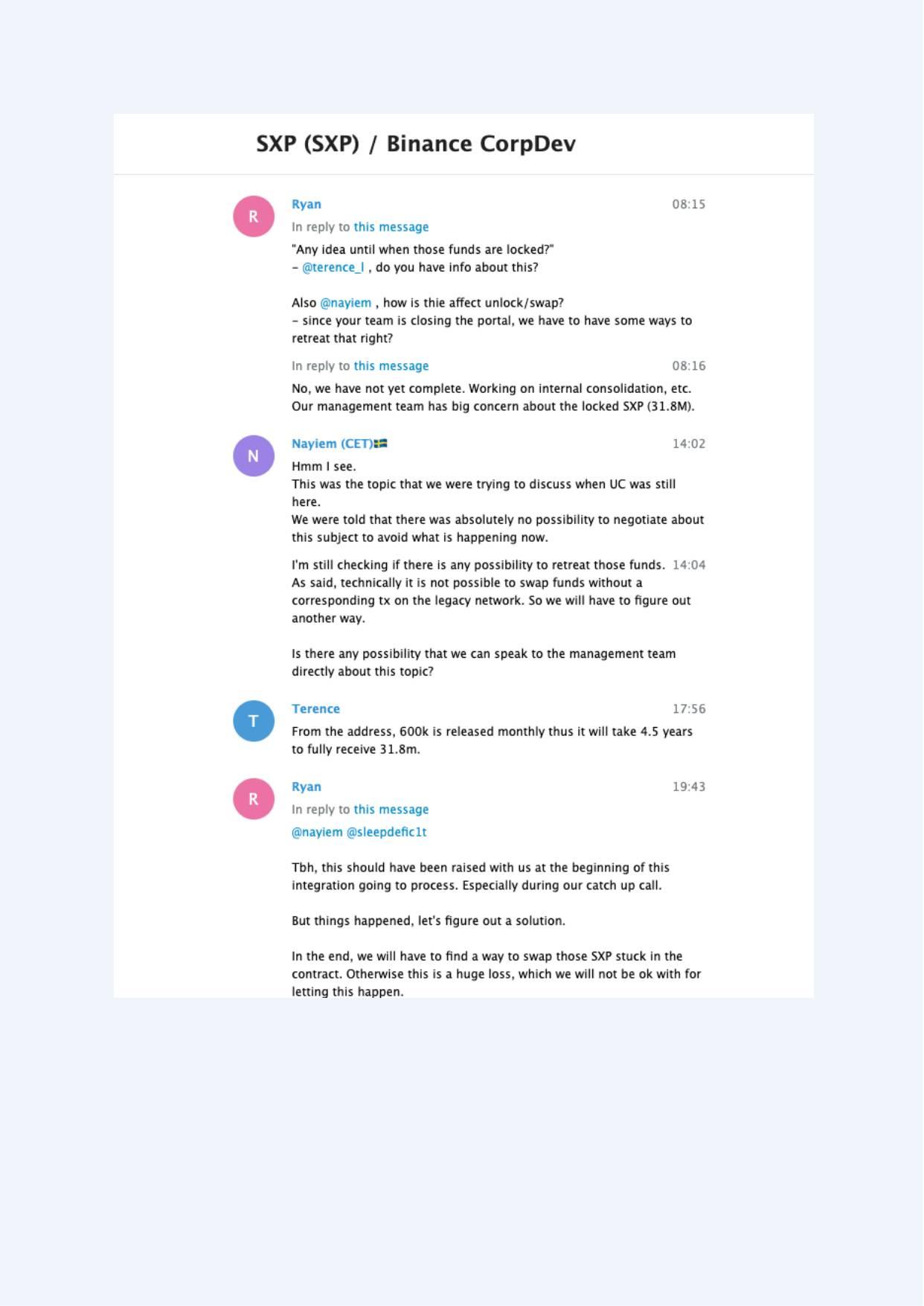

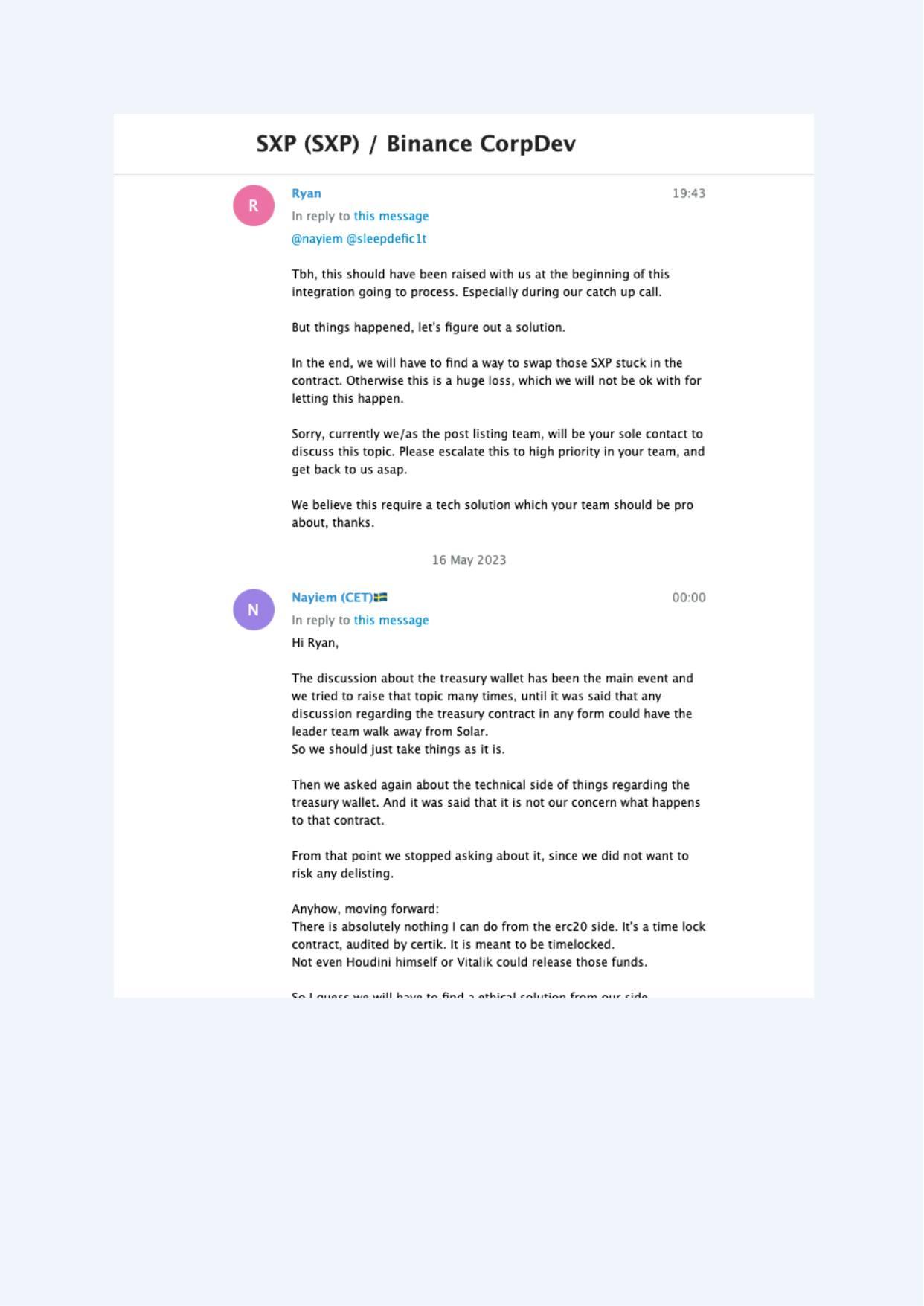

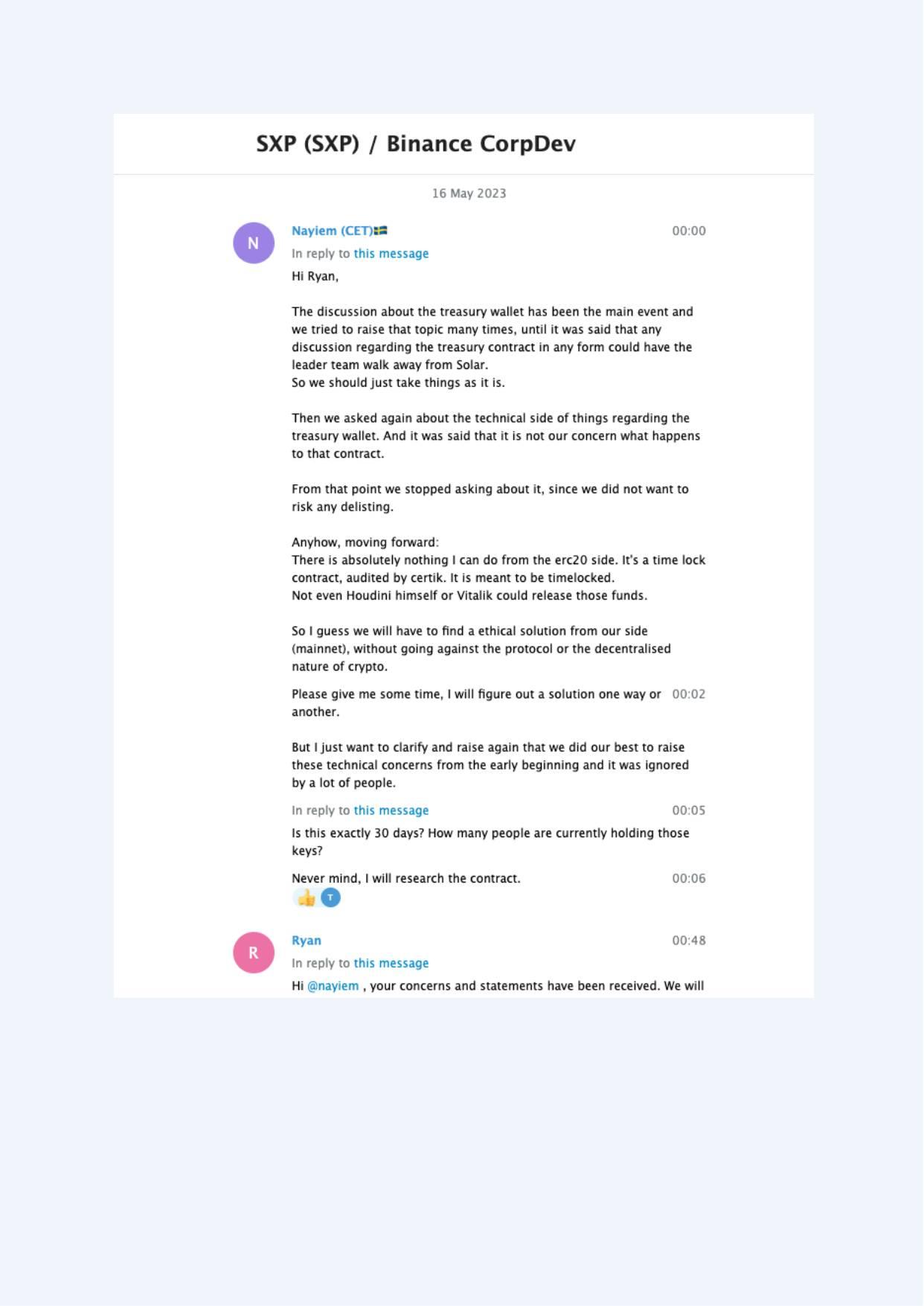

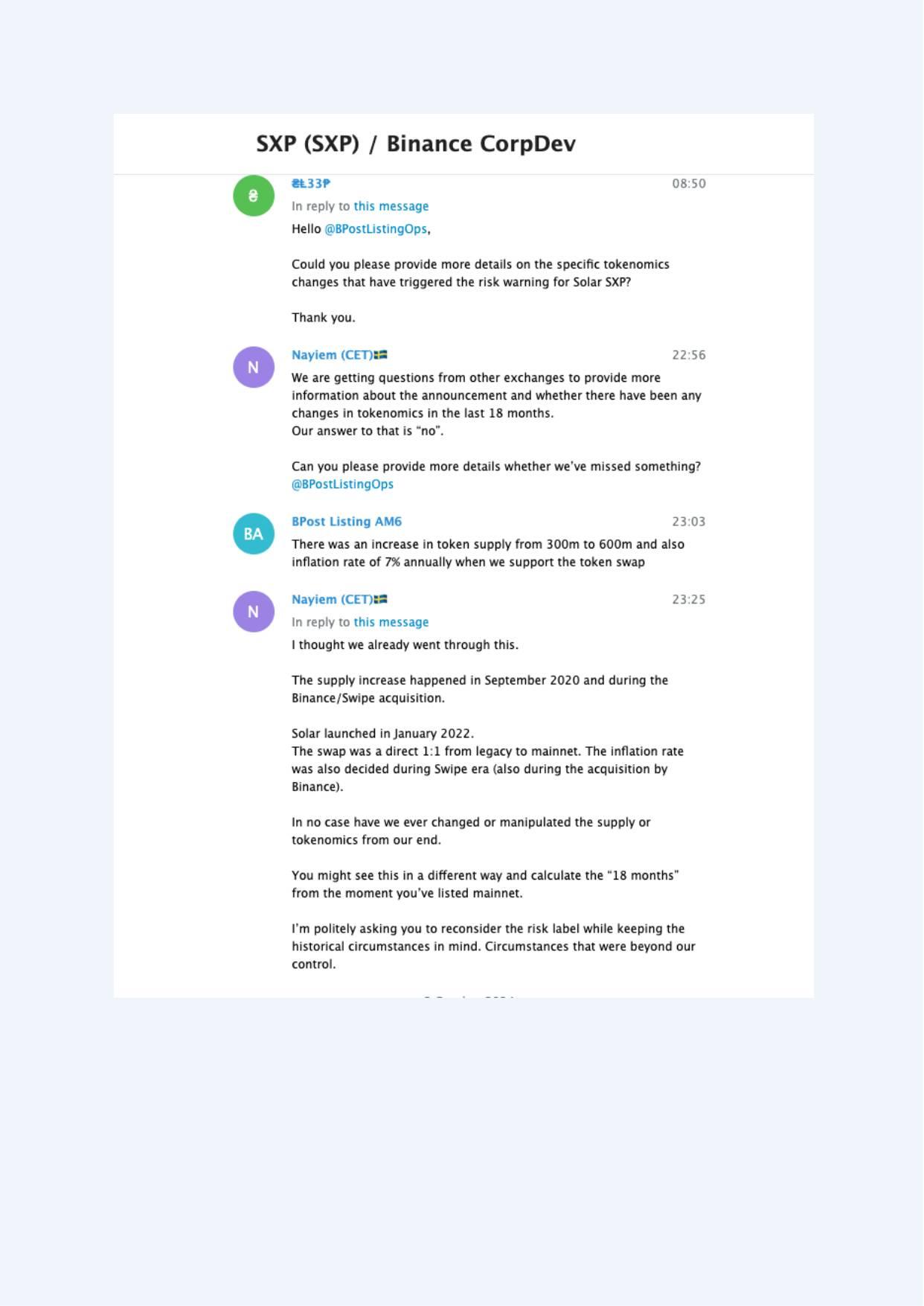

Questions regarding token supply mechanics and treasury custody coincided with increased reputational burden borne by the community.

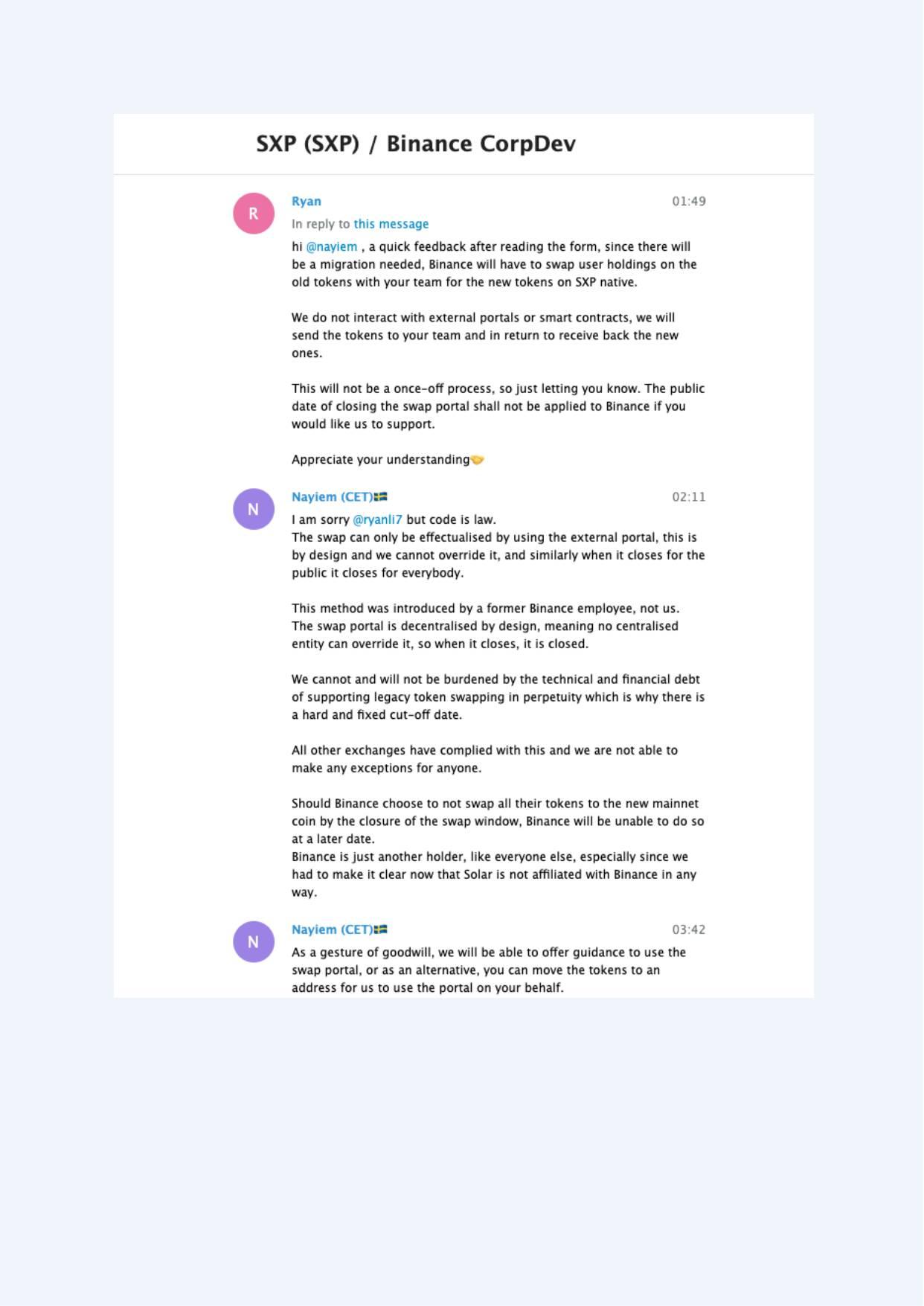

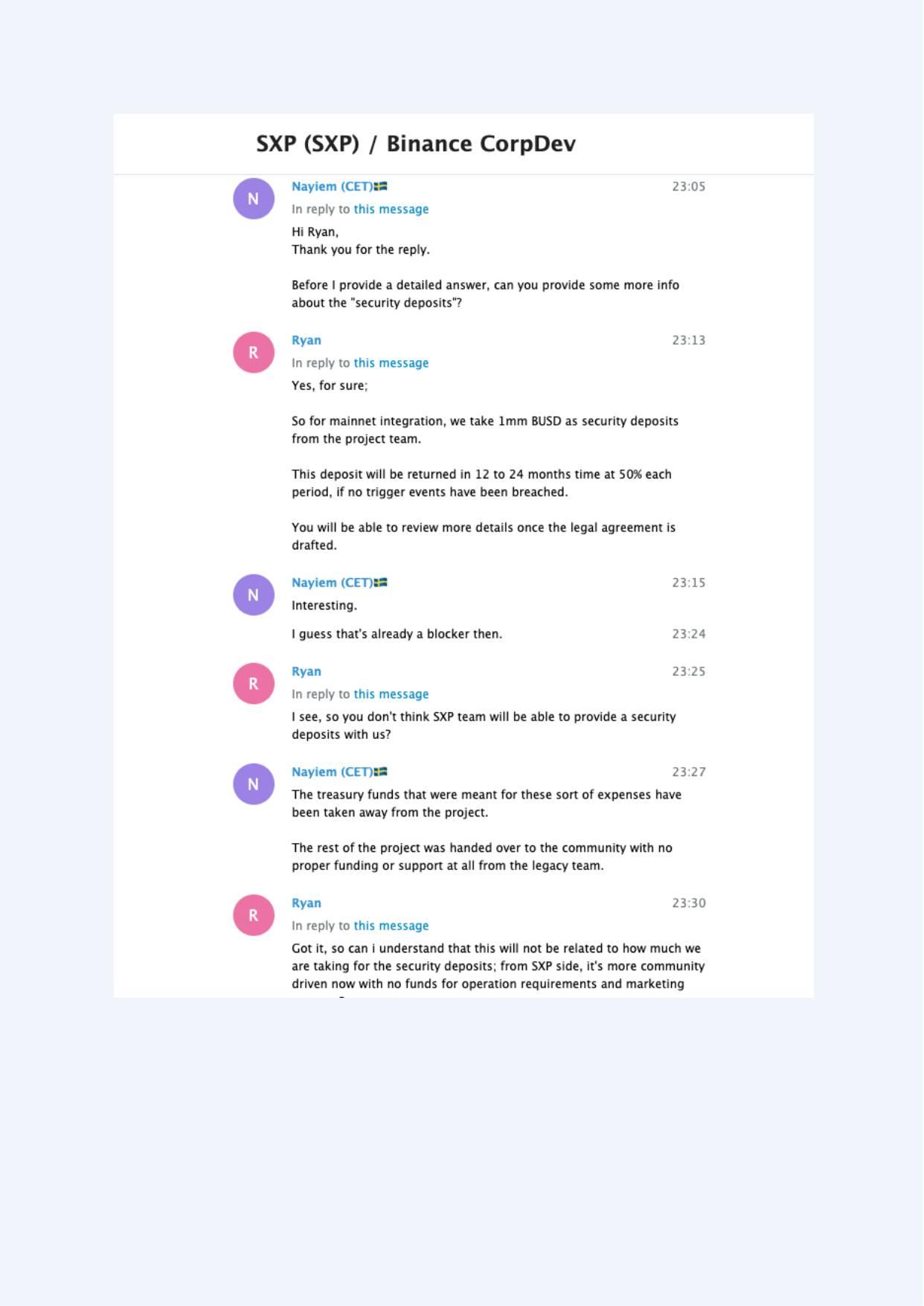

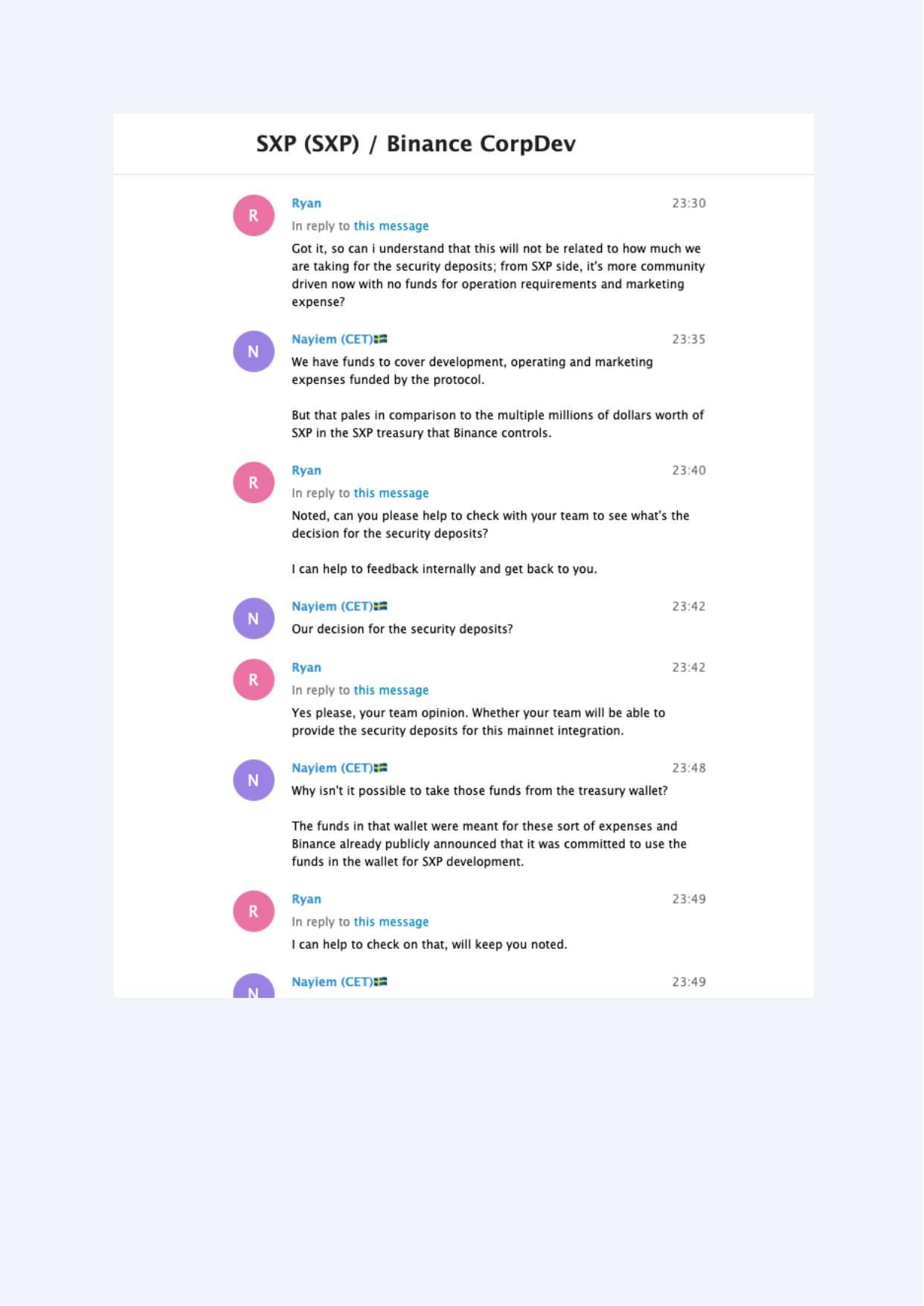

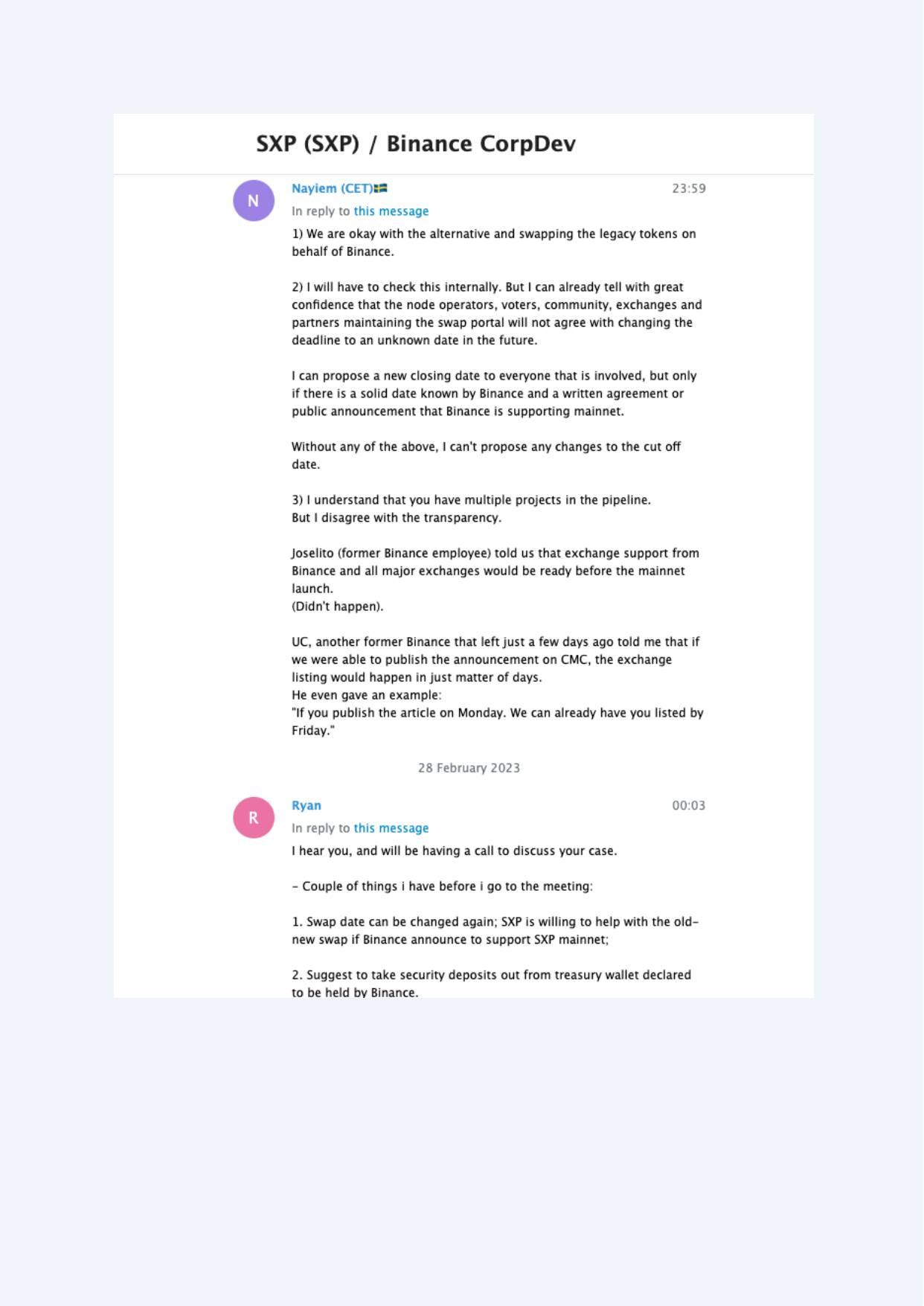

Draft contractual terms tied to listing or support were assessed as unusually one-sided, including provisions allowing suspension of swaps or retention of deposits.

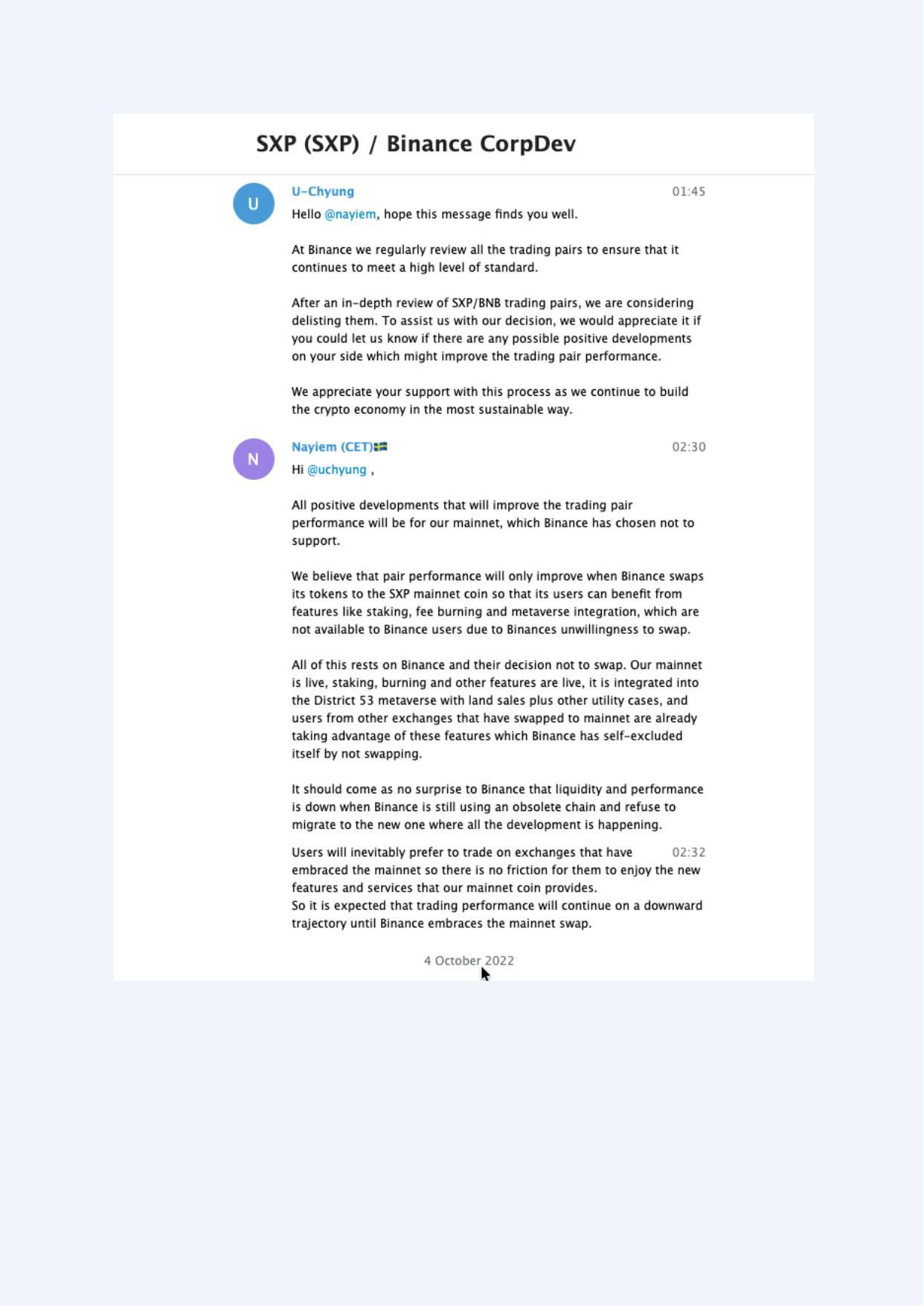

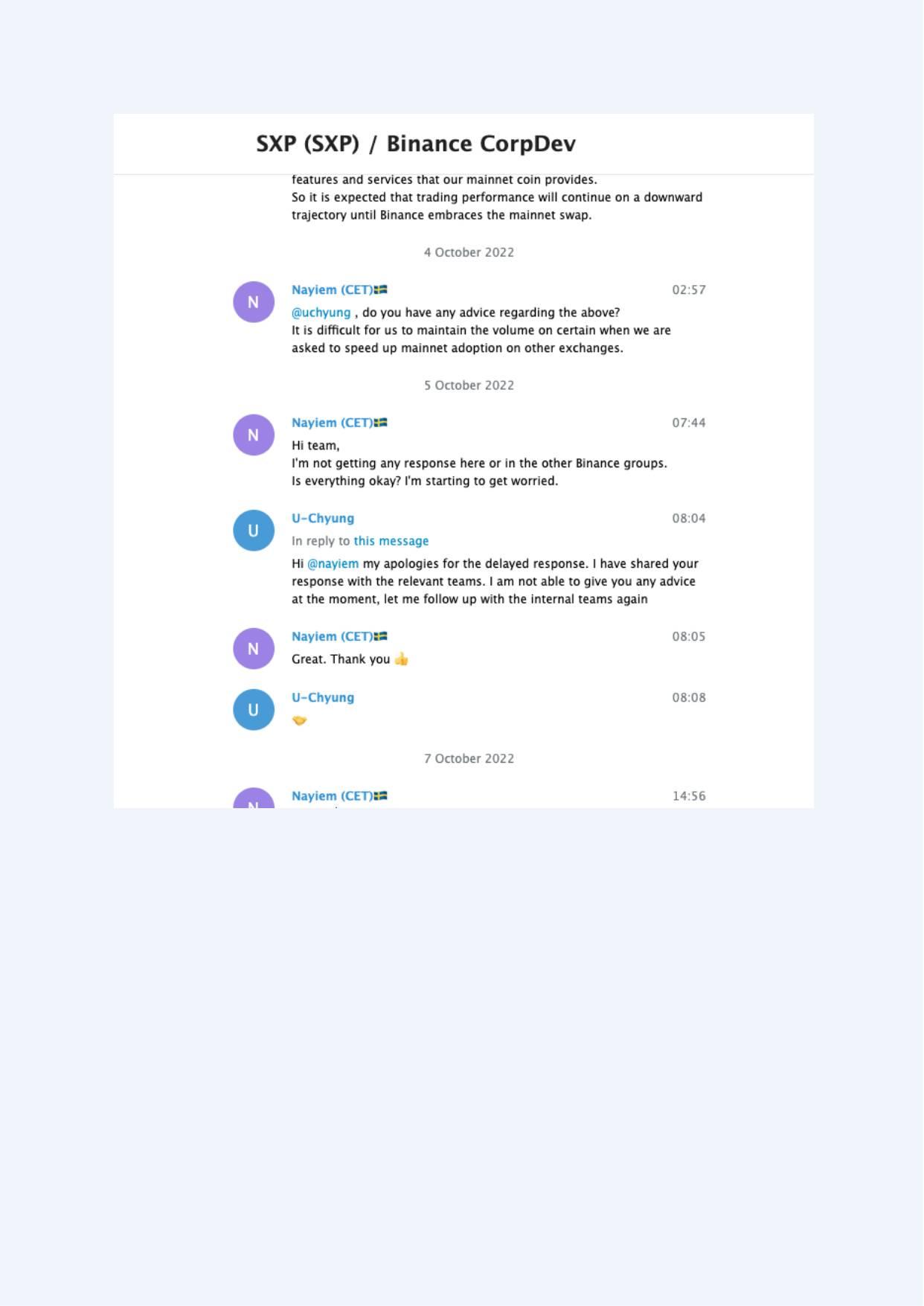

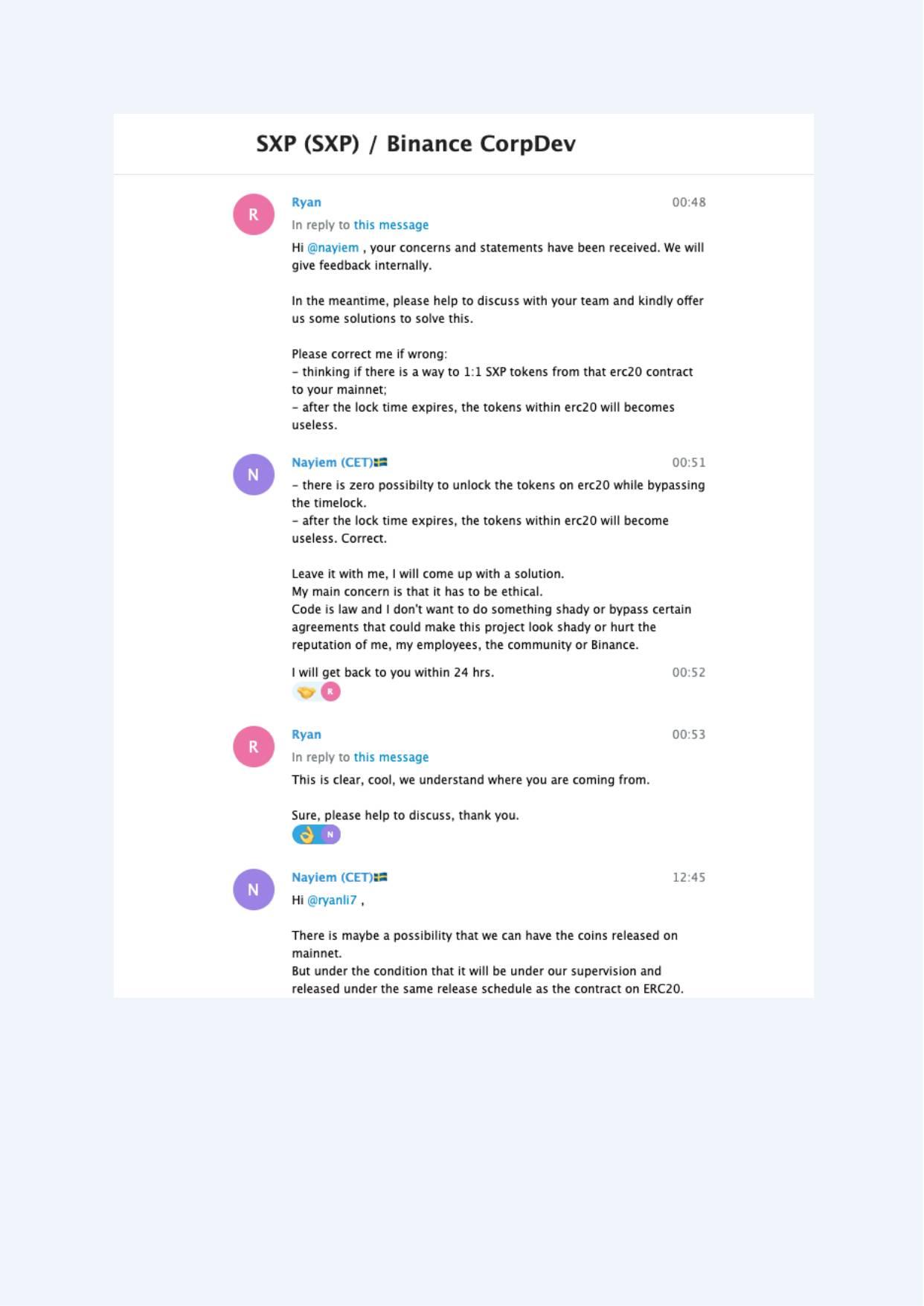

Practical support for upgrades and integrations appeared, from Solar’s perspective, to be conditioned on treasury outcomes without corresponding long-term guarantees.

These points are presented as contextual observations and assessments, not legal conclusions.

Potential Legal and Regulatory Considerations (Contextual)

The circumstances described above are sometimes discussed in public discourse using general legal or regulatory terminology. The references below are included solely to explain how similar fact patterns are often analyzed in abstract, not to assert that such standards were breached.

Included and Excluded Materials

Included:

Screenshot compilations of Binance communications (compiled in Binance Proof (1)),

relevant public Binance announcements and research materials,

the Swipe/SXP whitepaper, and

the March 2023 draft agreement.

Excluded:

post-2023 communications and agreements, which are preserved privately and will only be disclosed to regulators or official investigative bodies if formally requested.

How to Read This Record

References in this document use:

Exhibit A-###: pages from the screenshot compilation (Binance Proof (1).pdf),

Public Source P#: publicly available webpages,

Document D#: provided PDFs (whitepapers or agreements).

Selected Findings (Illustrative Examples)

Solar Card / Ticker Constraints

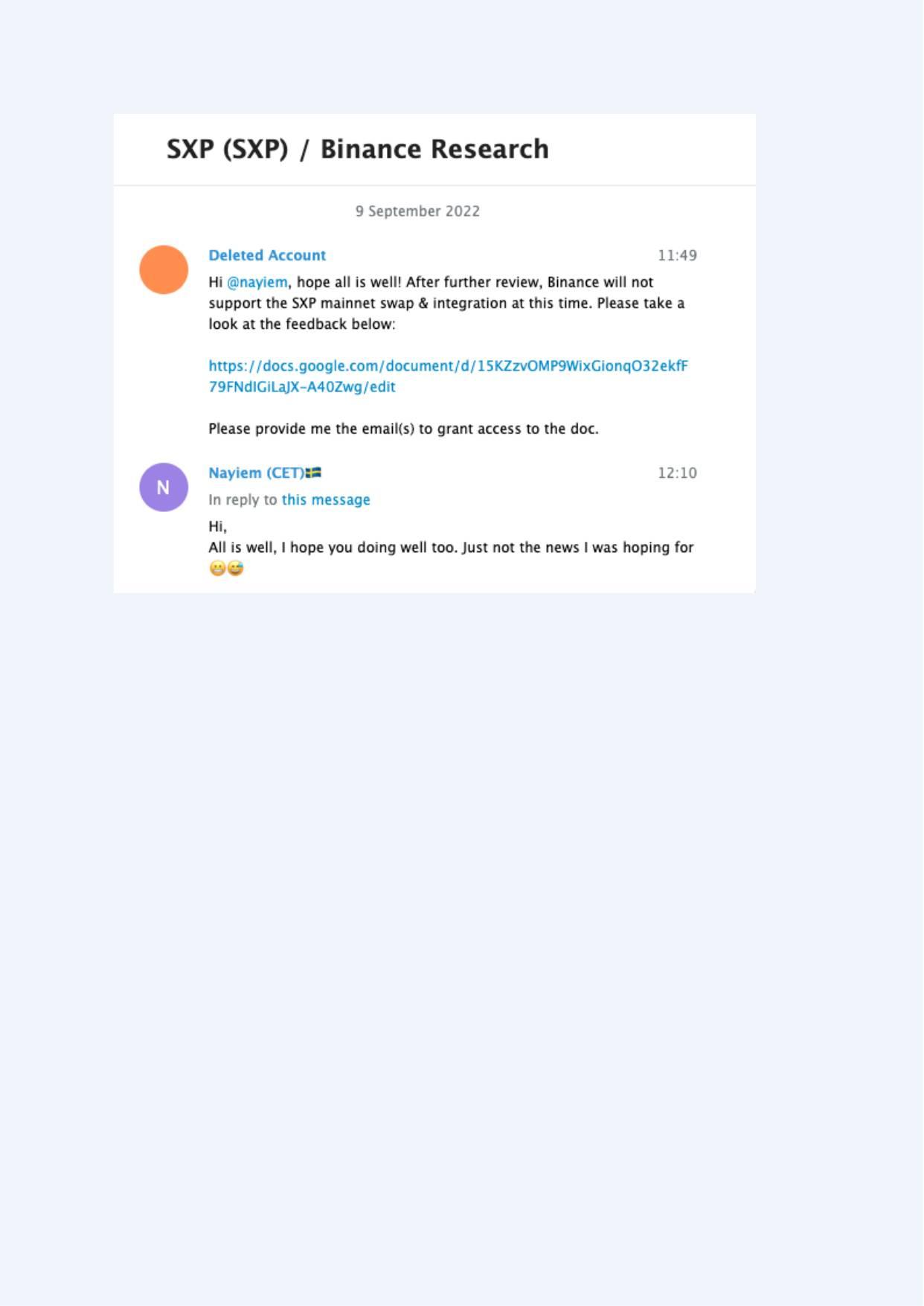

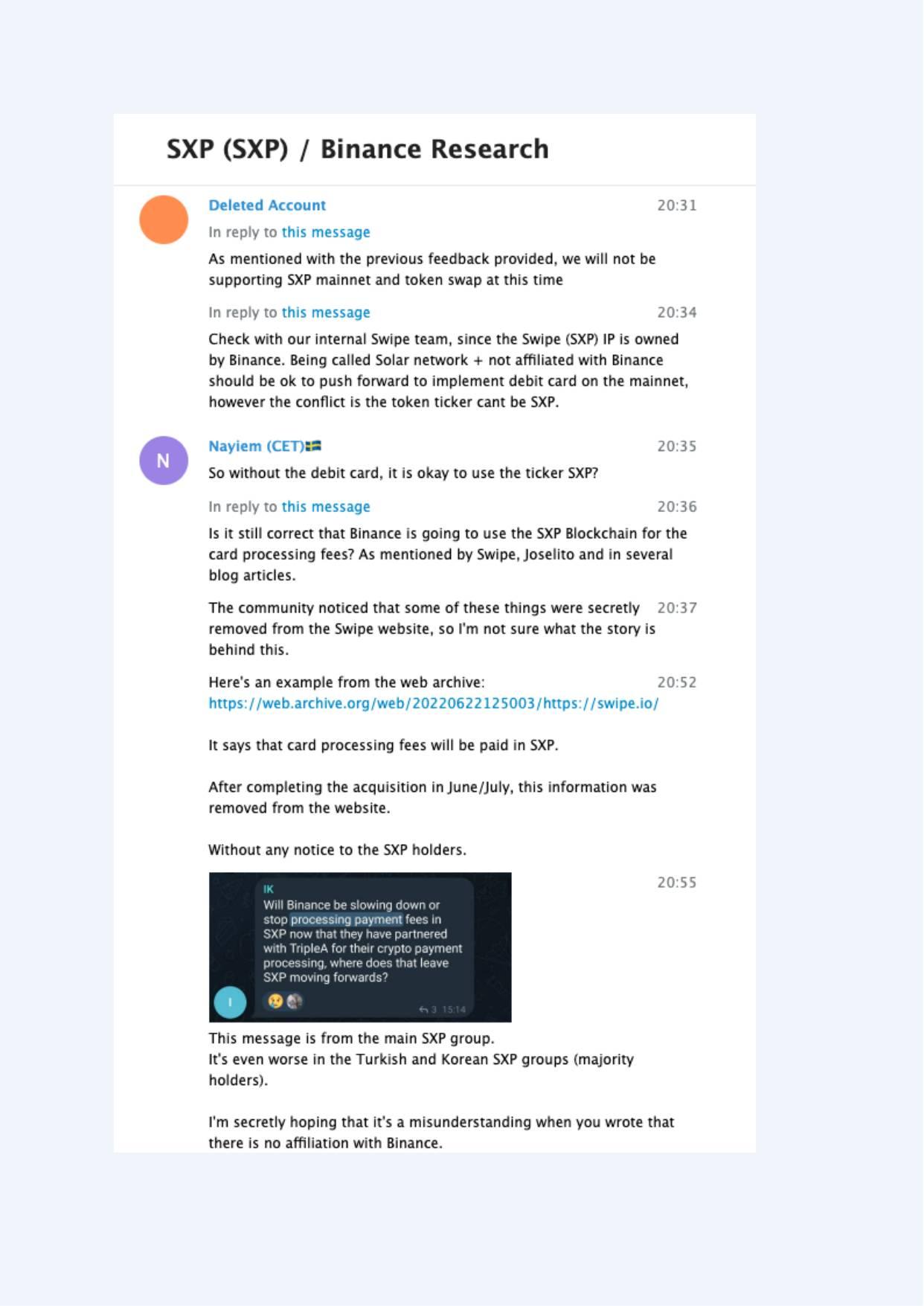

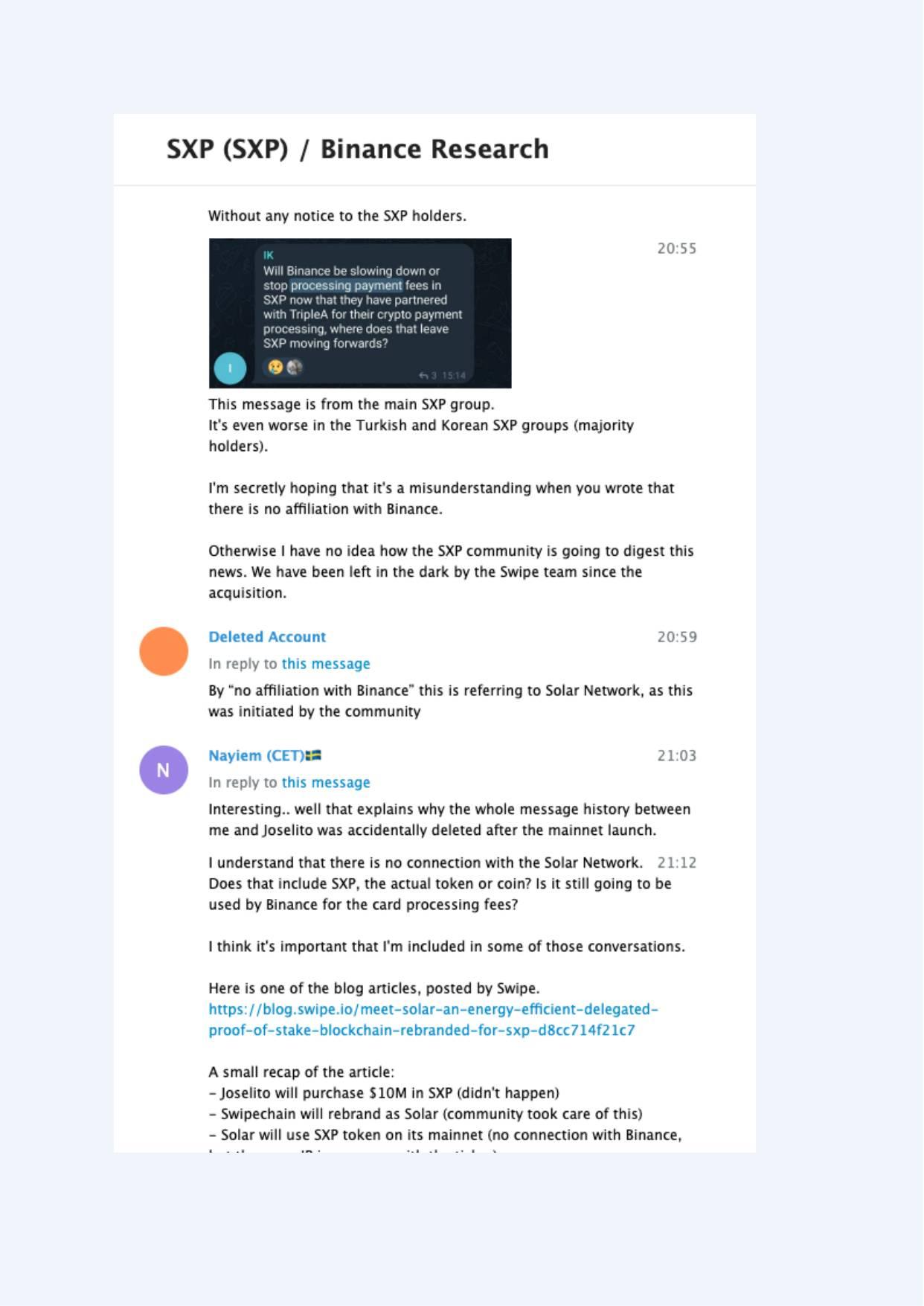

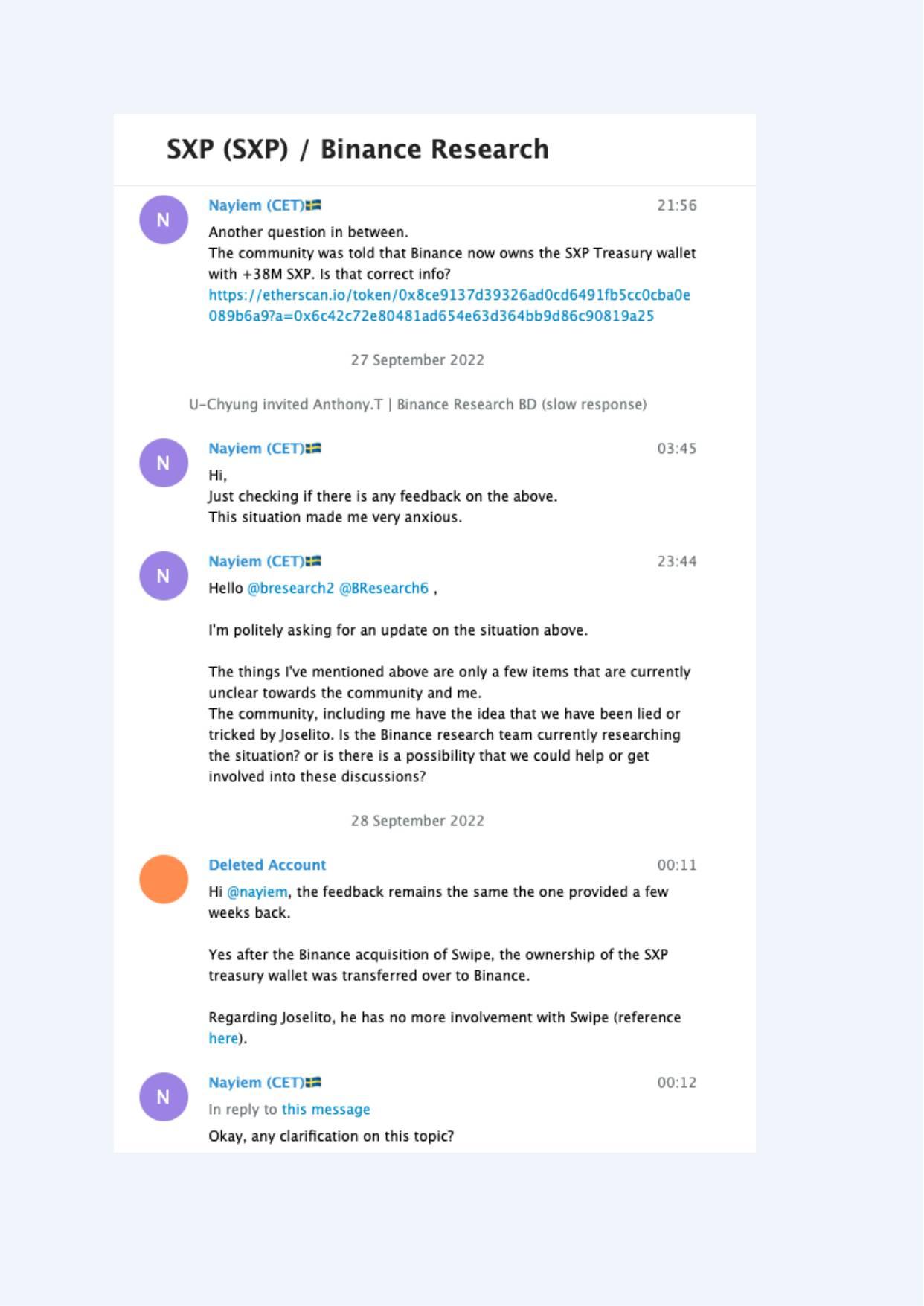

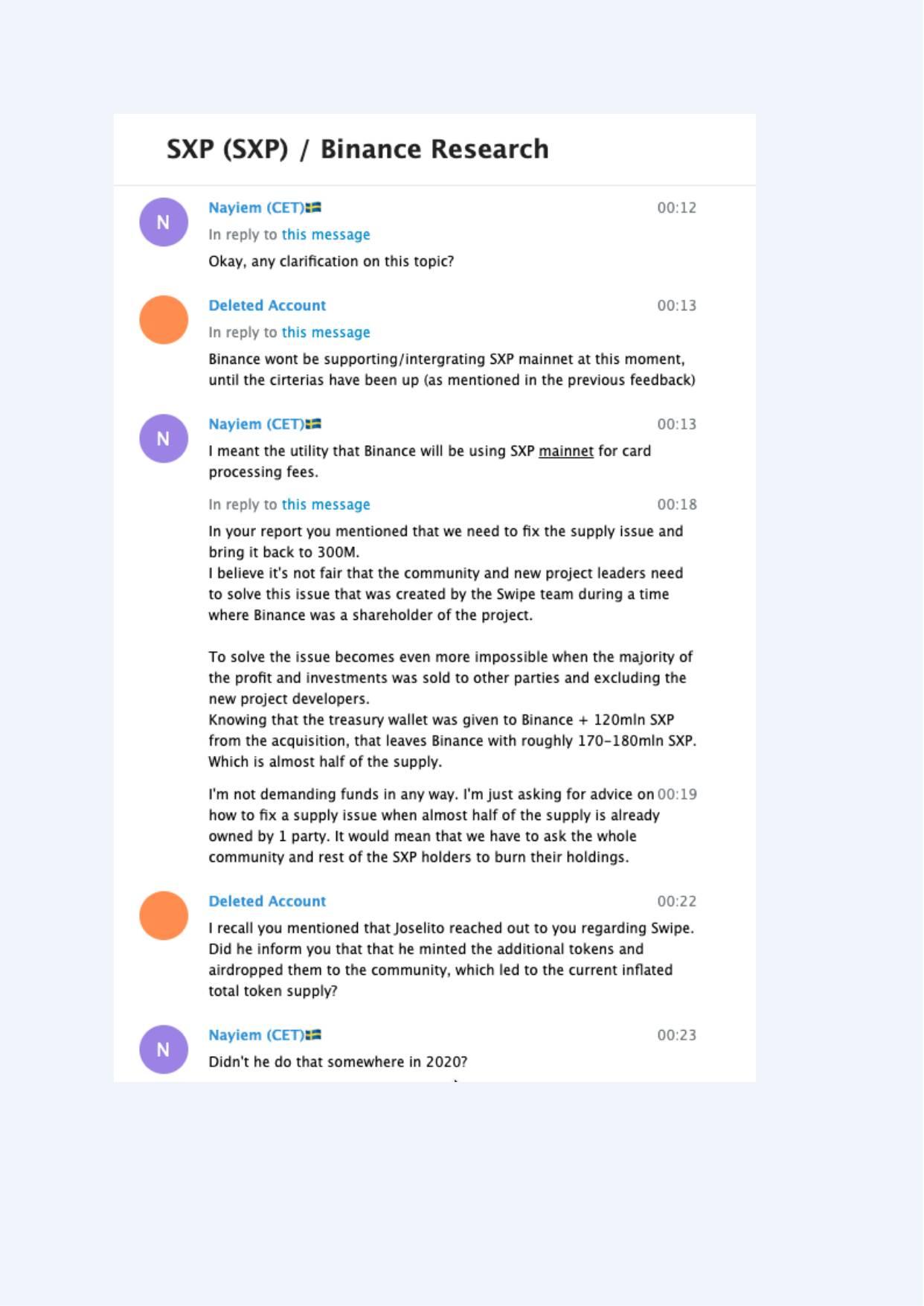

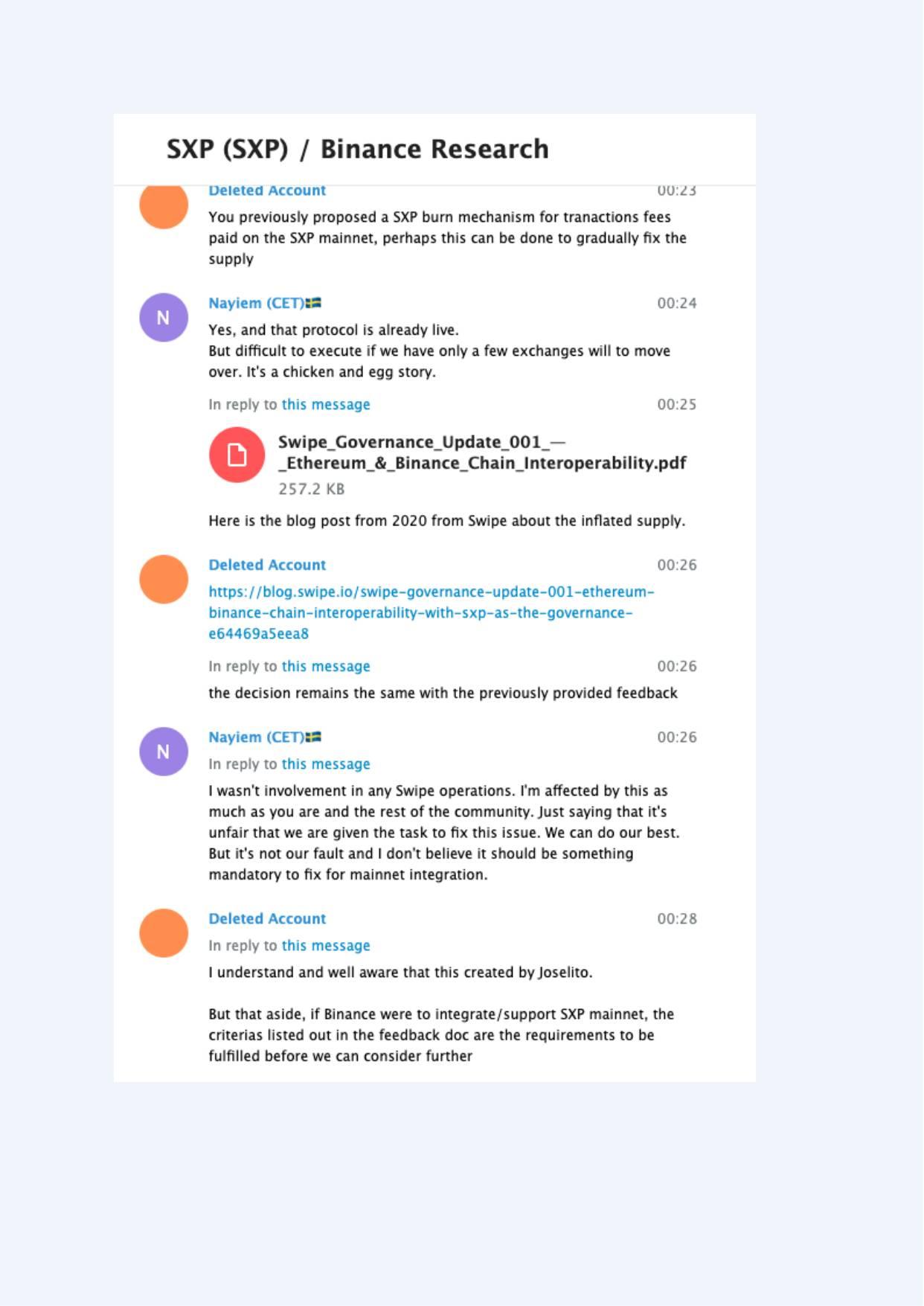

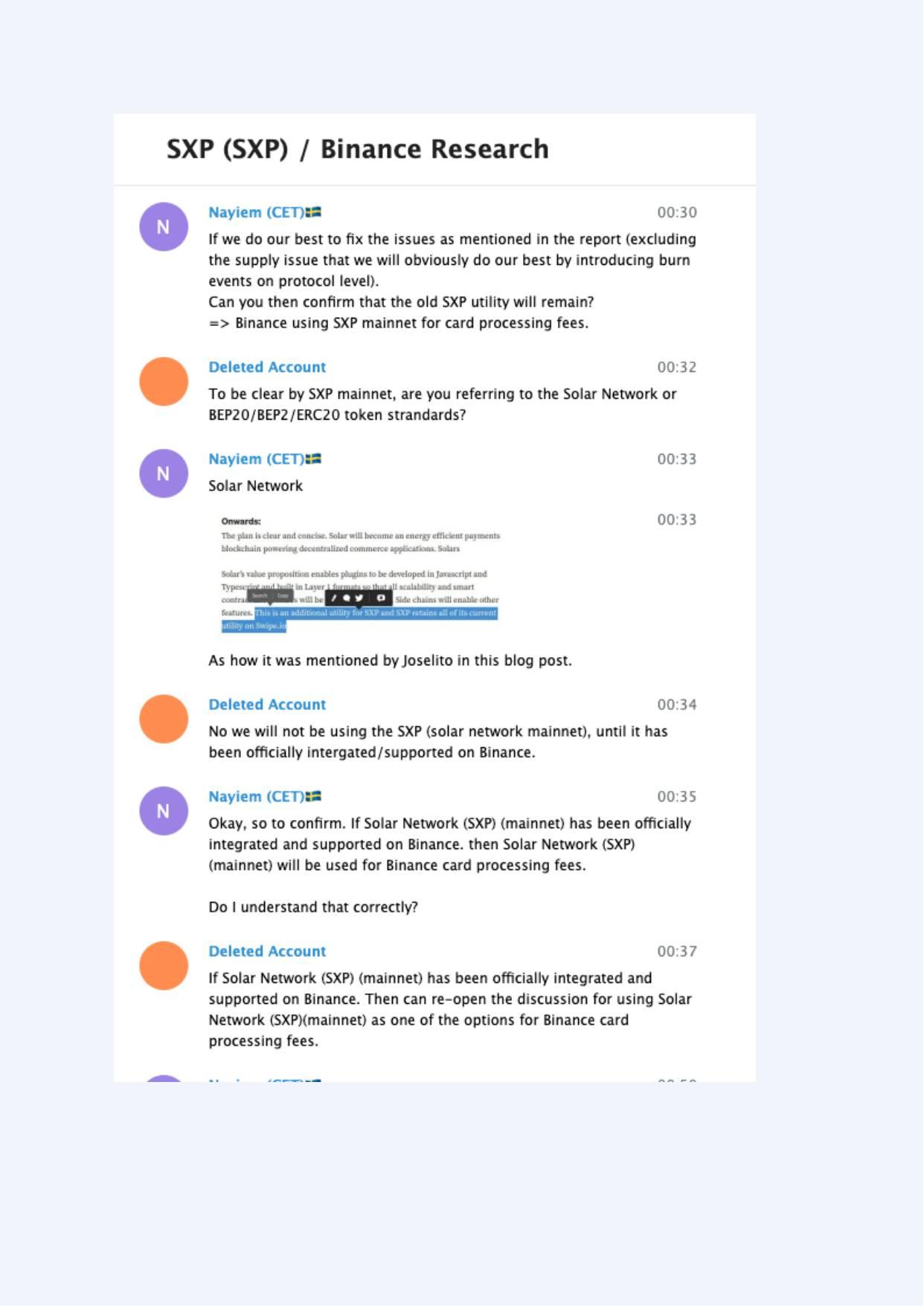

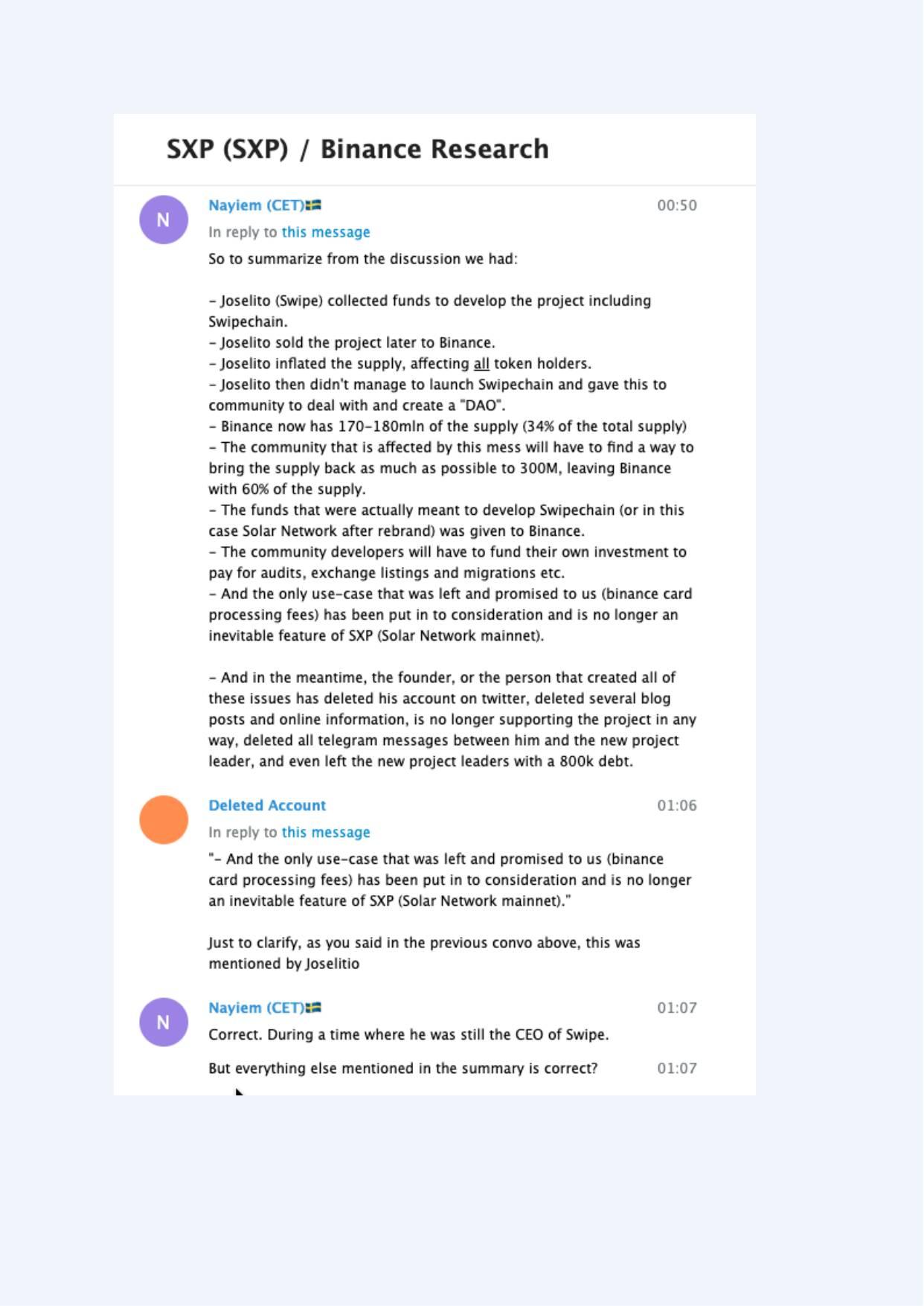

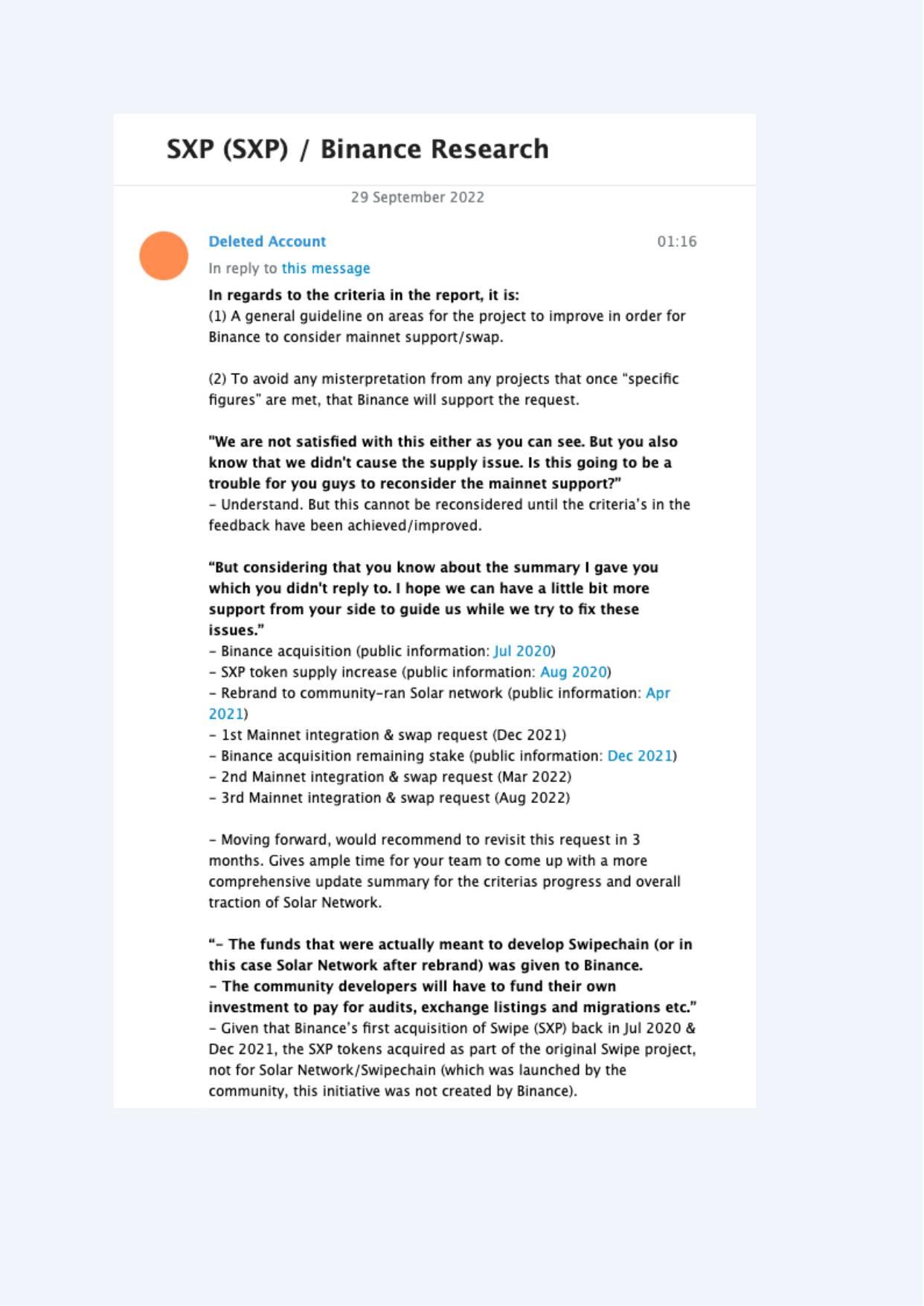

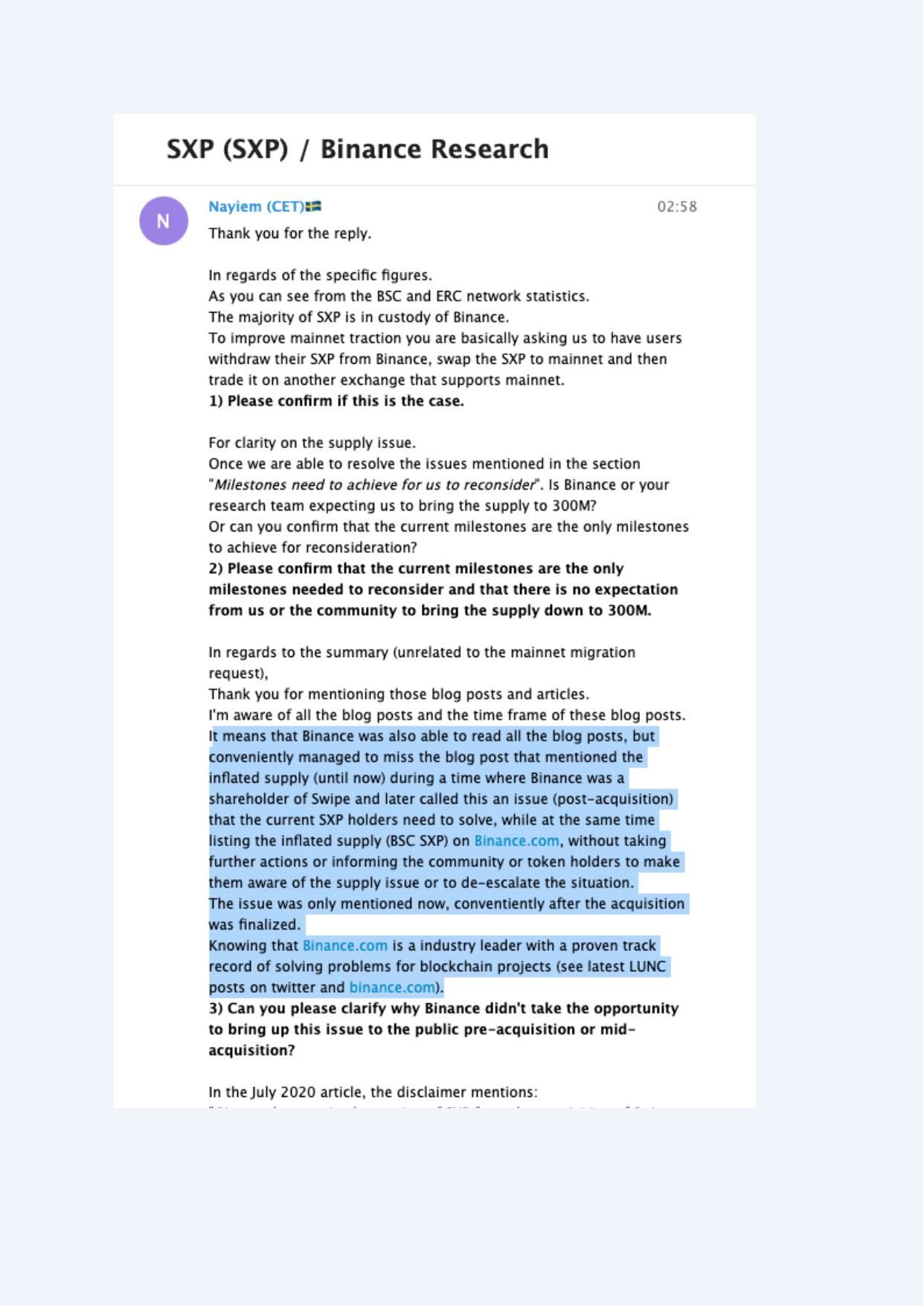

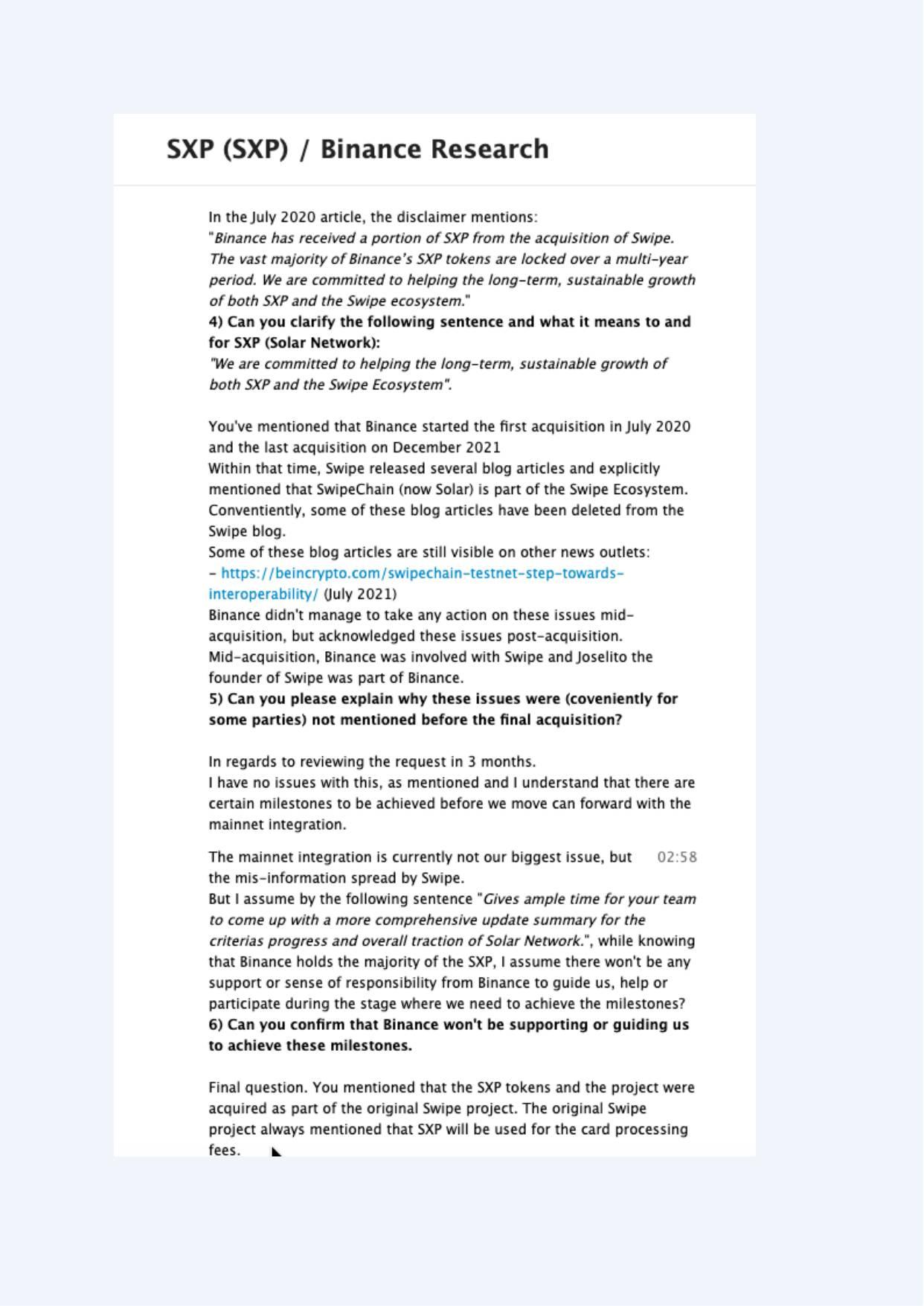

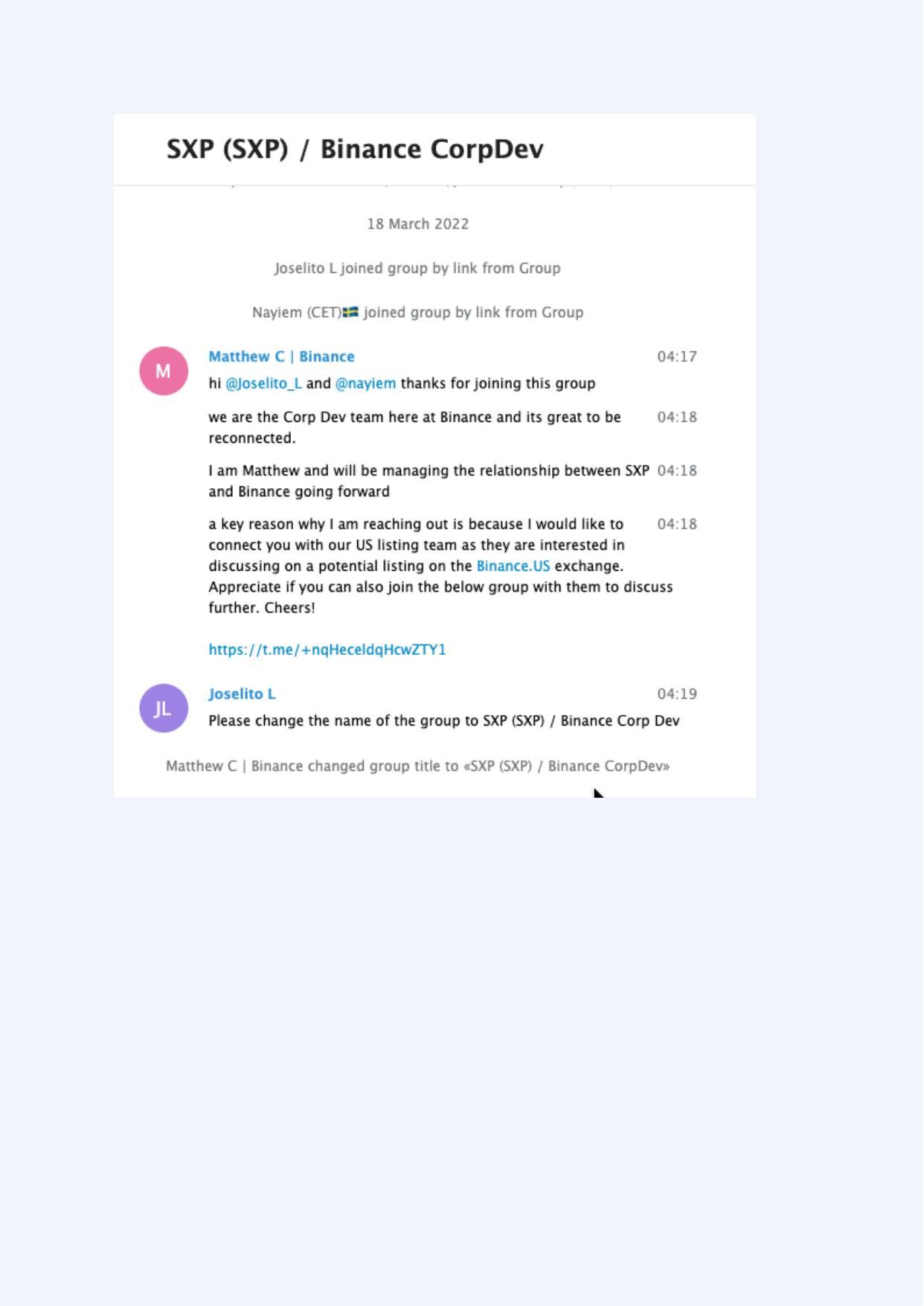

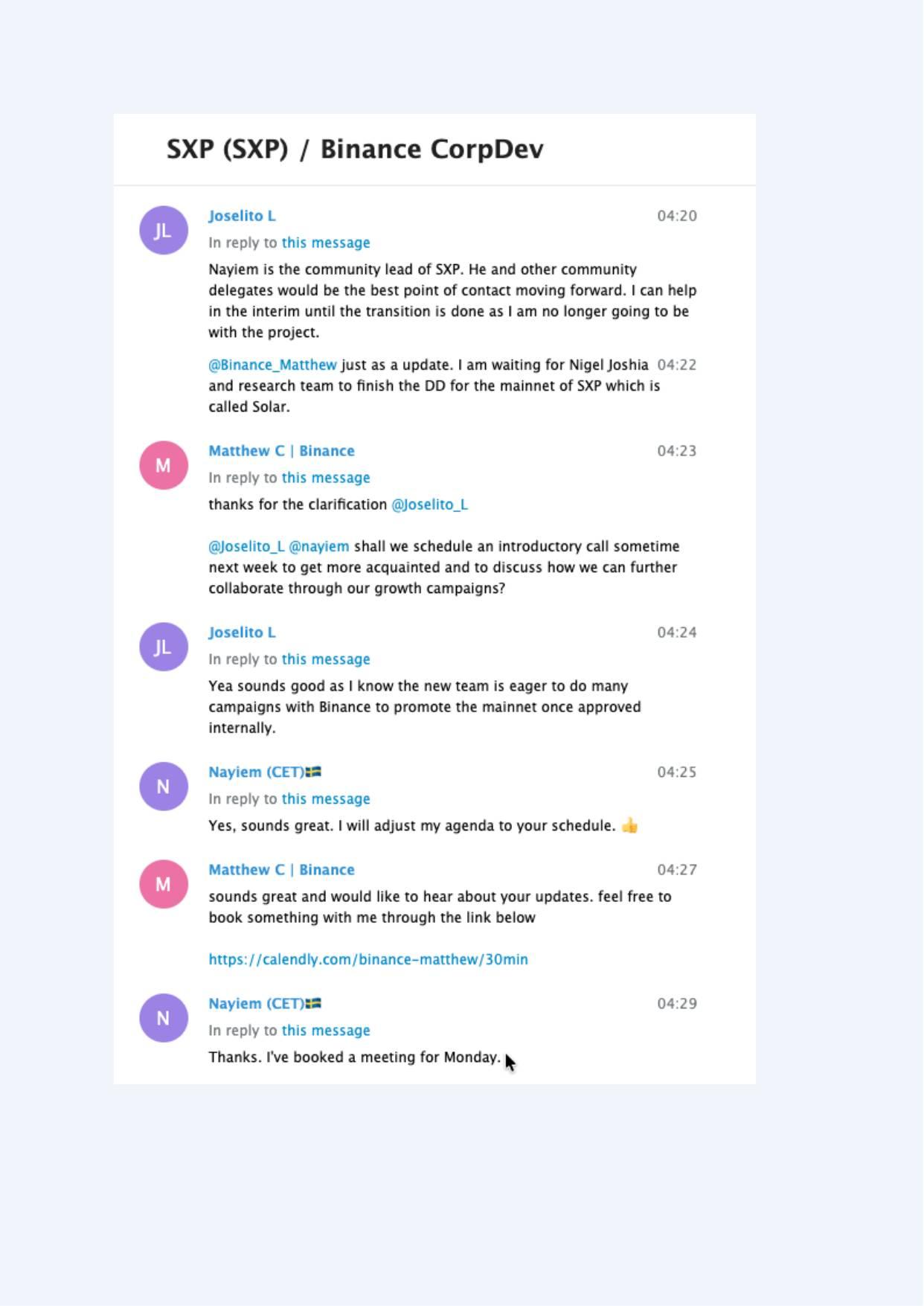

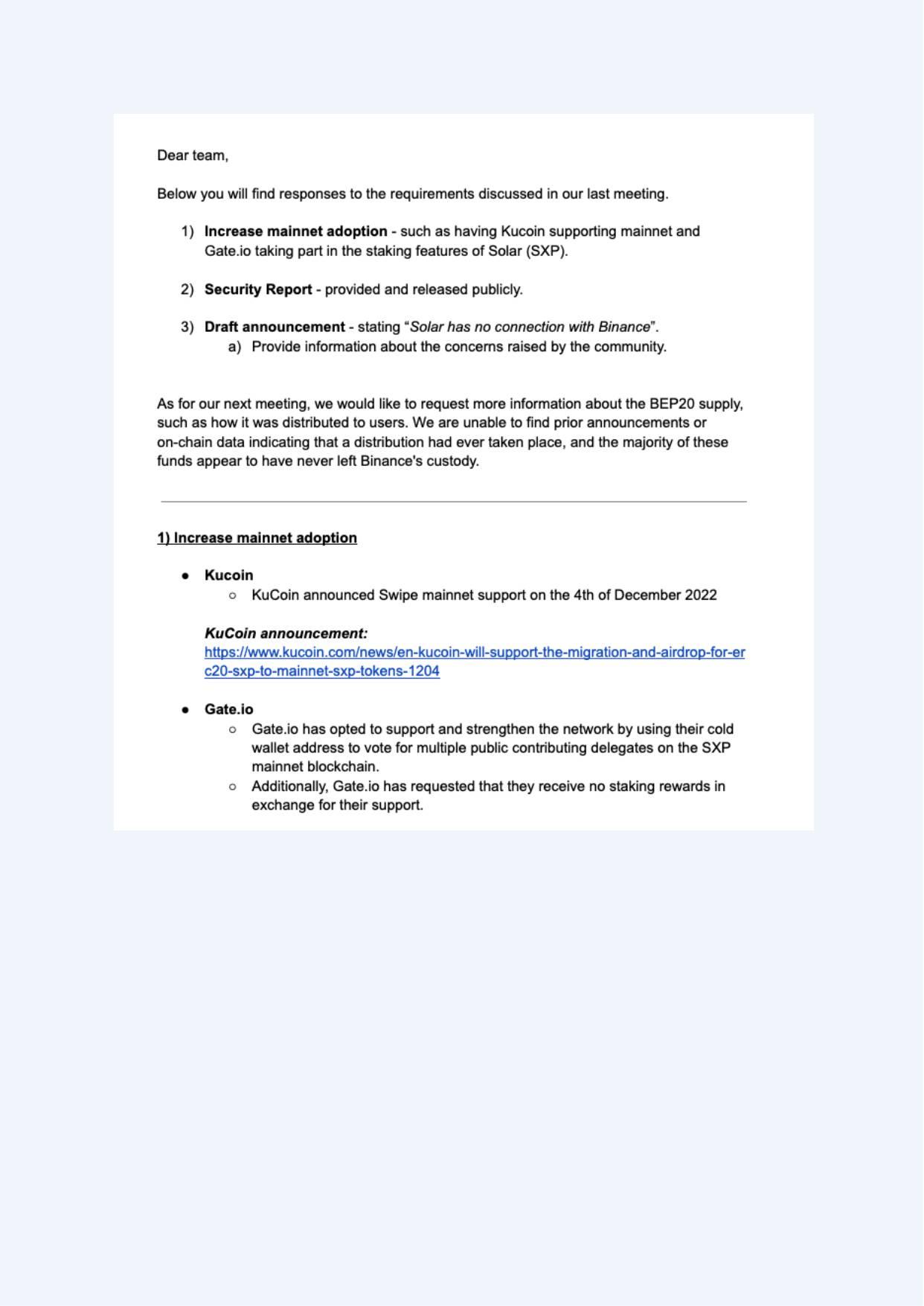

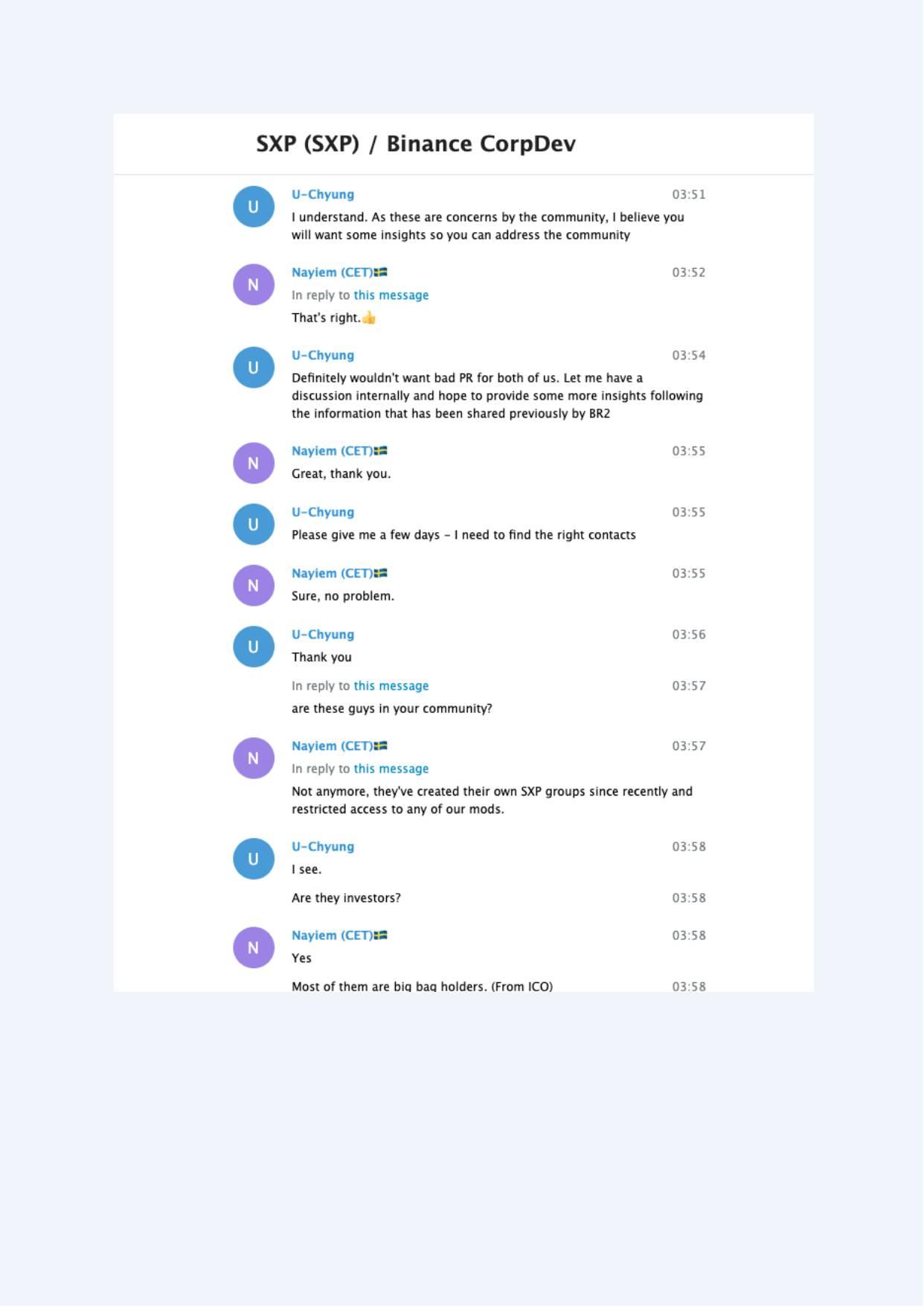

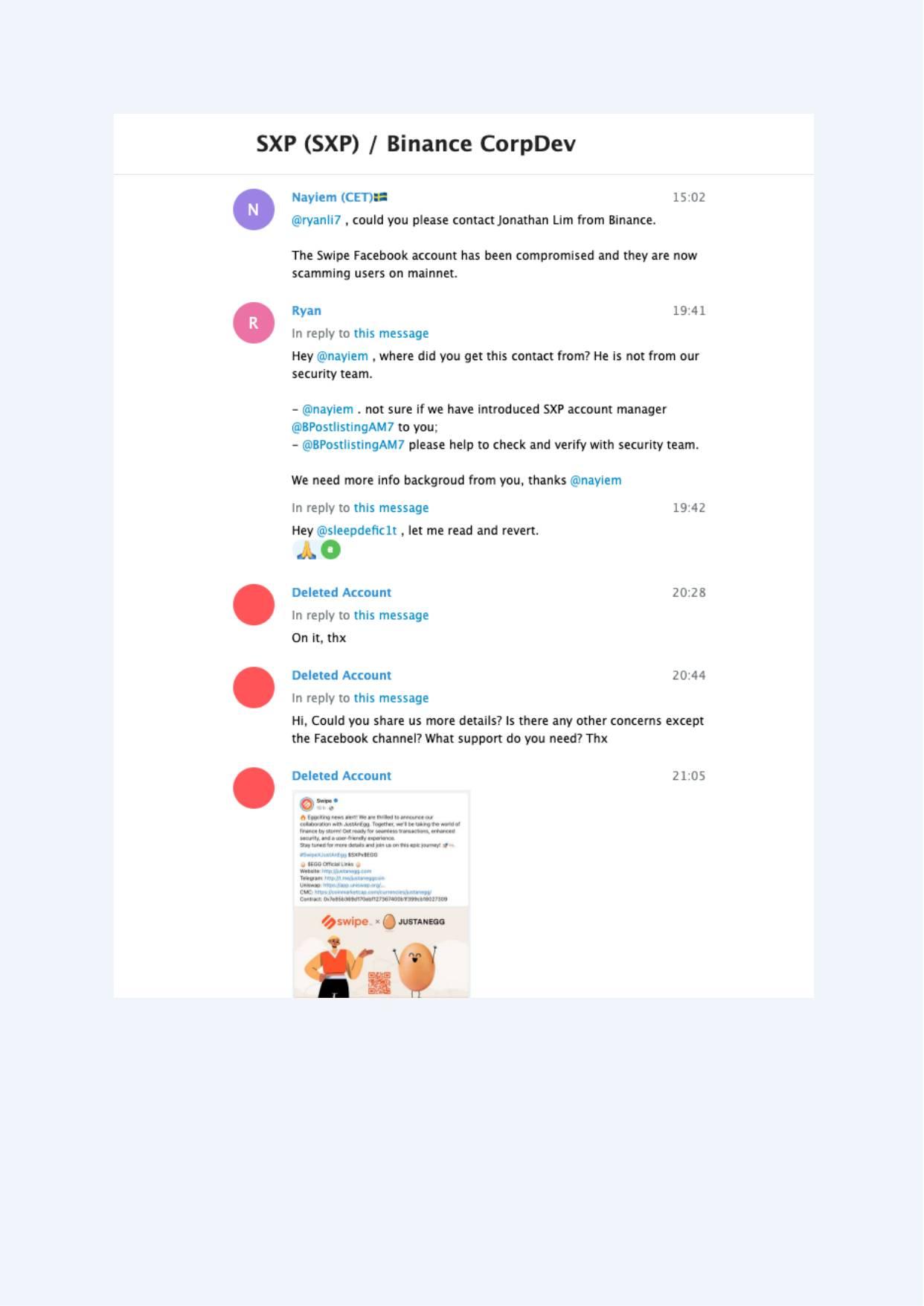

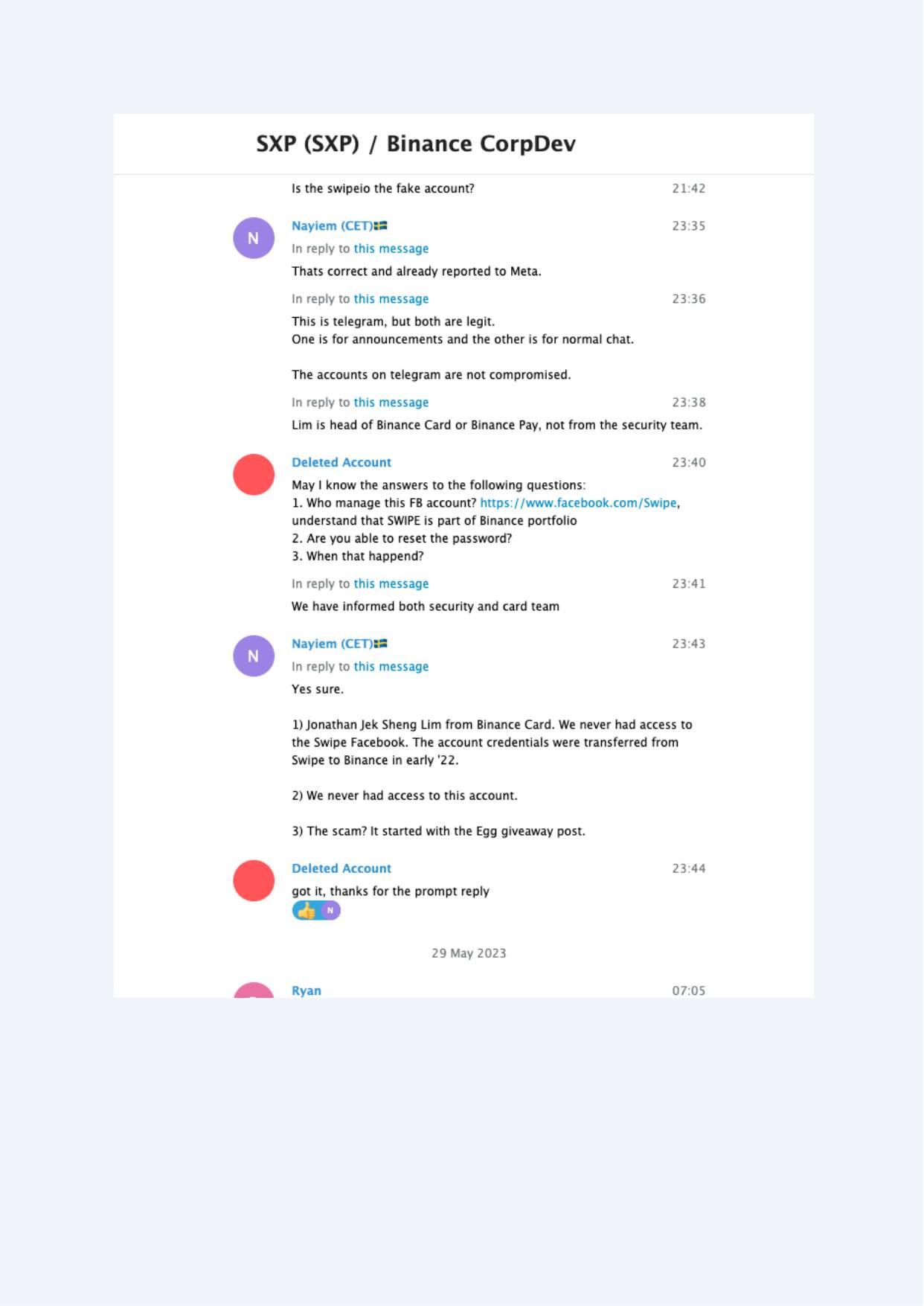

In September 2022, Binance Research stated that the Swipe (SXP) intellectual property was owned by Binance and that implementing a debit card on mainnet could conflict due to ticker usage. Solar leadership identified this as a blocker to a Solar Card launch (Exhibit A-002).

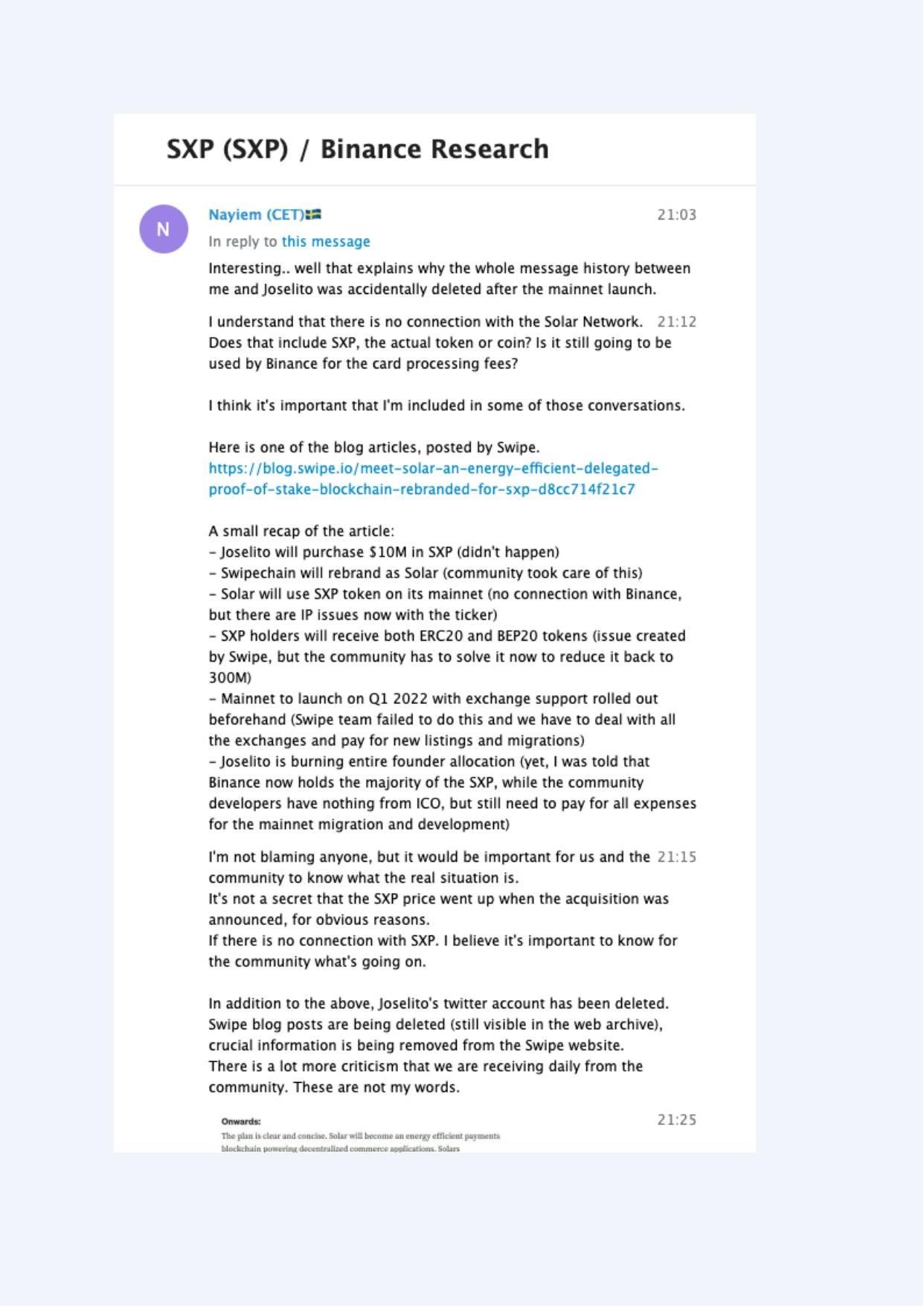

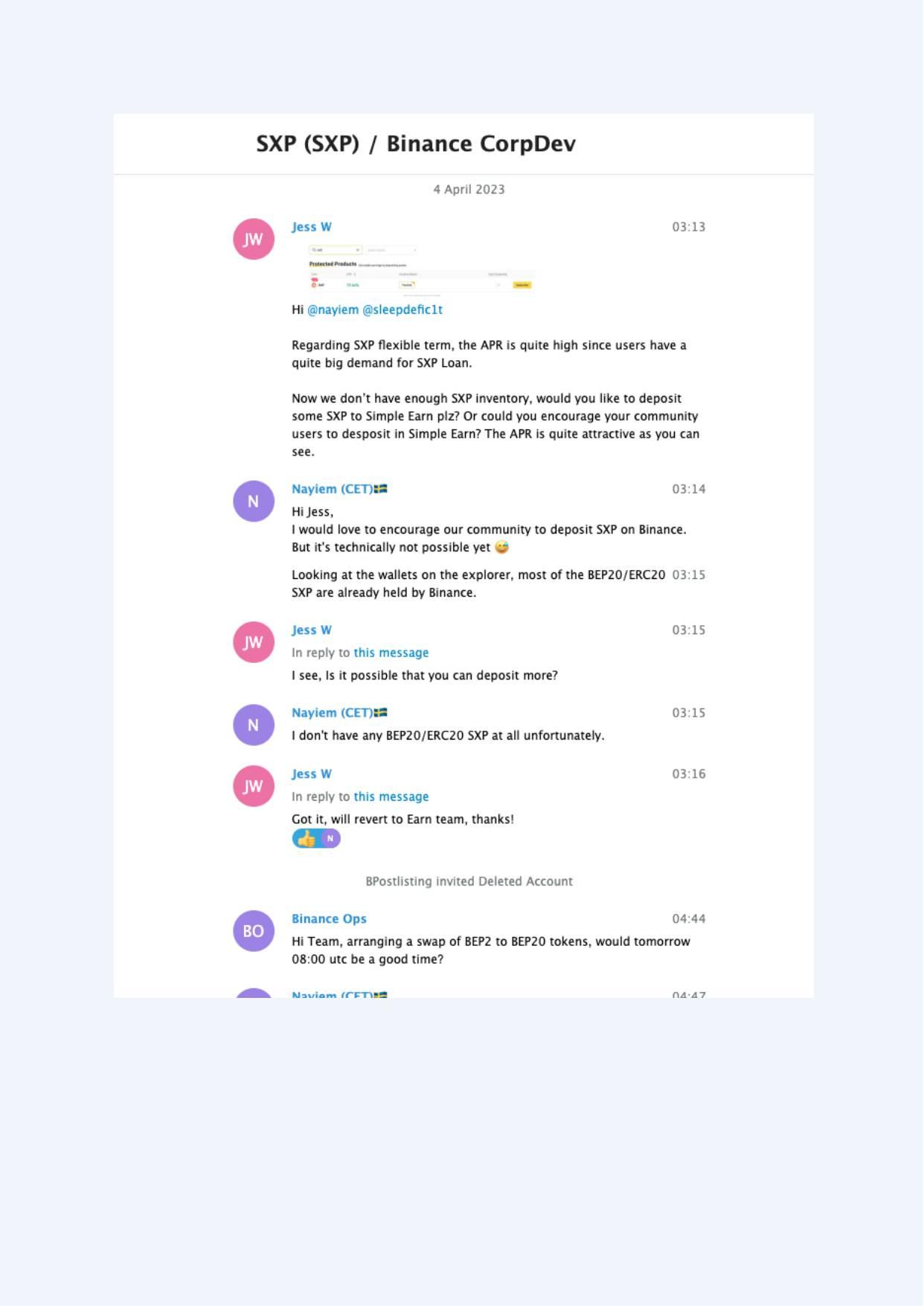

Card Processing Fees

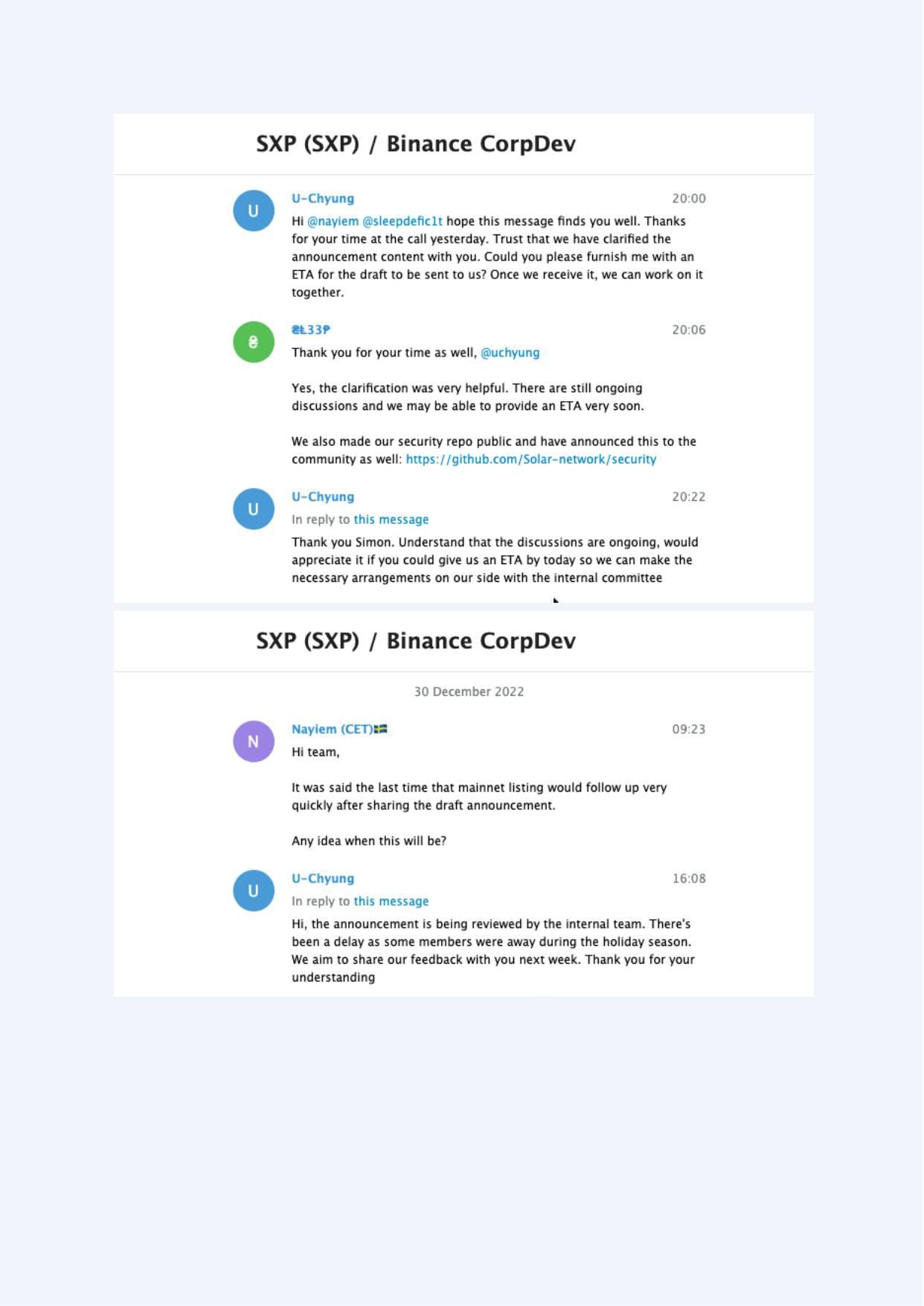

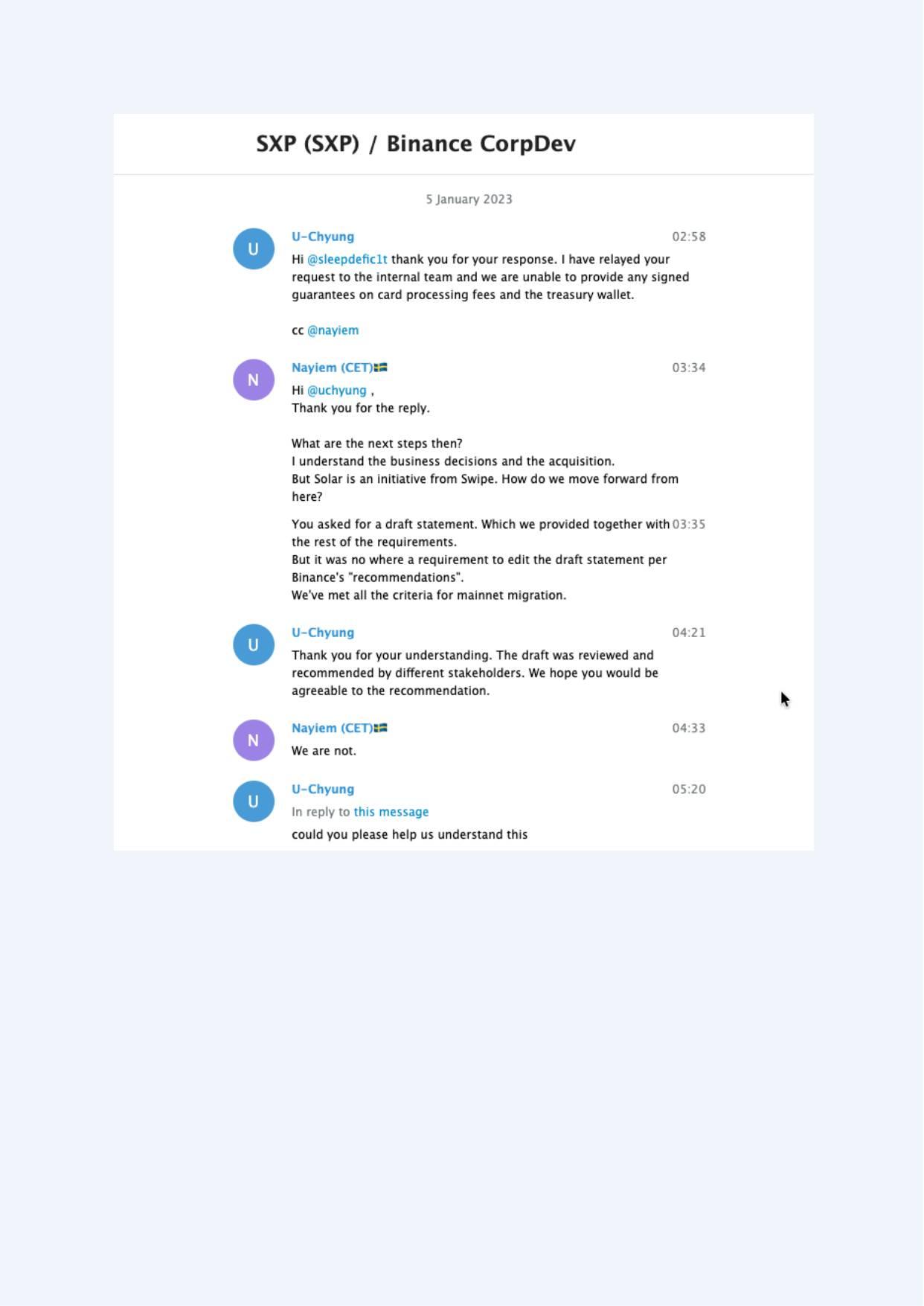

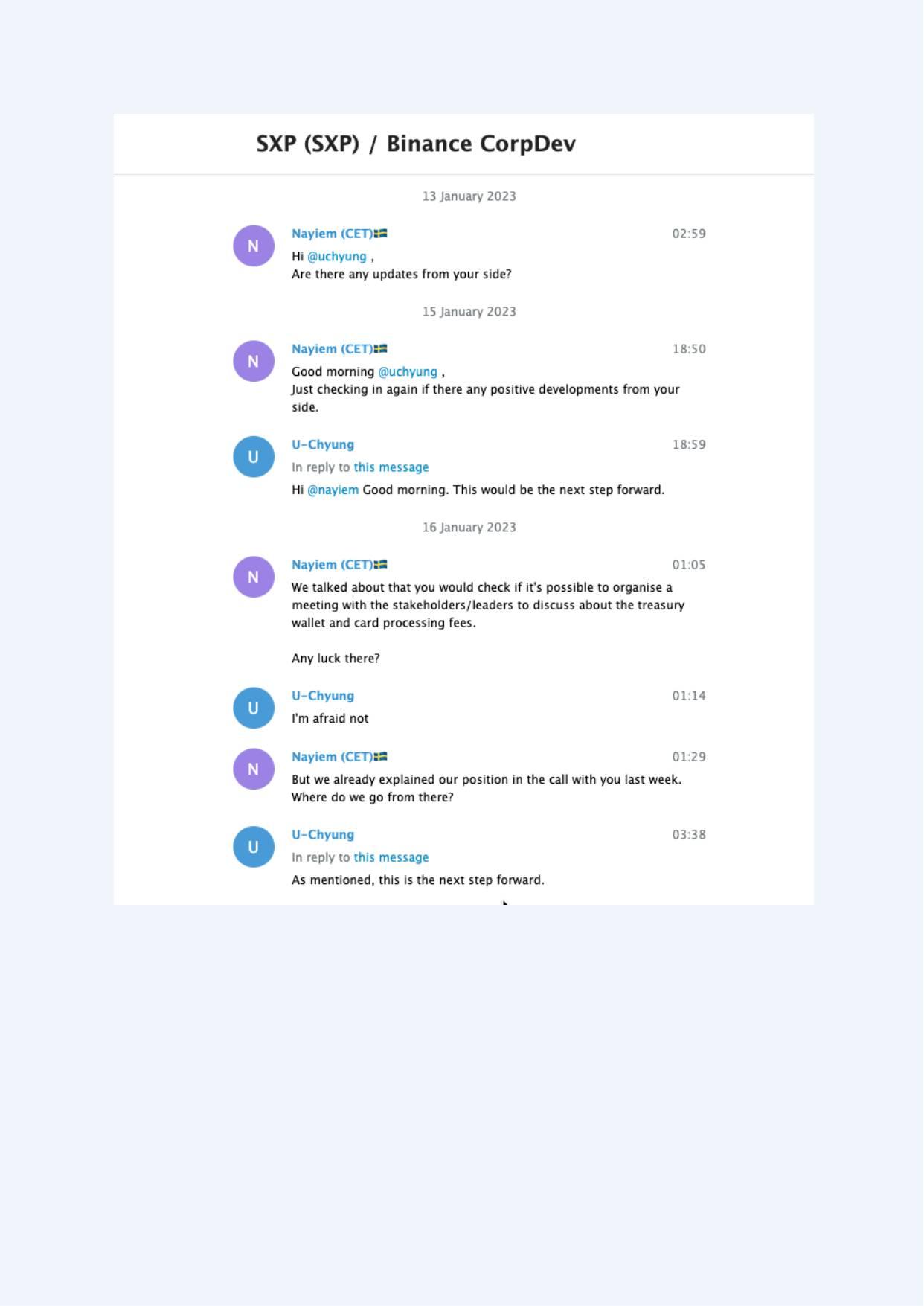

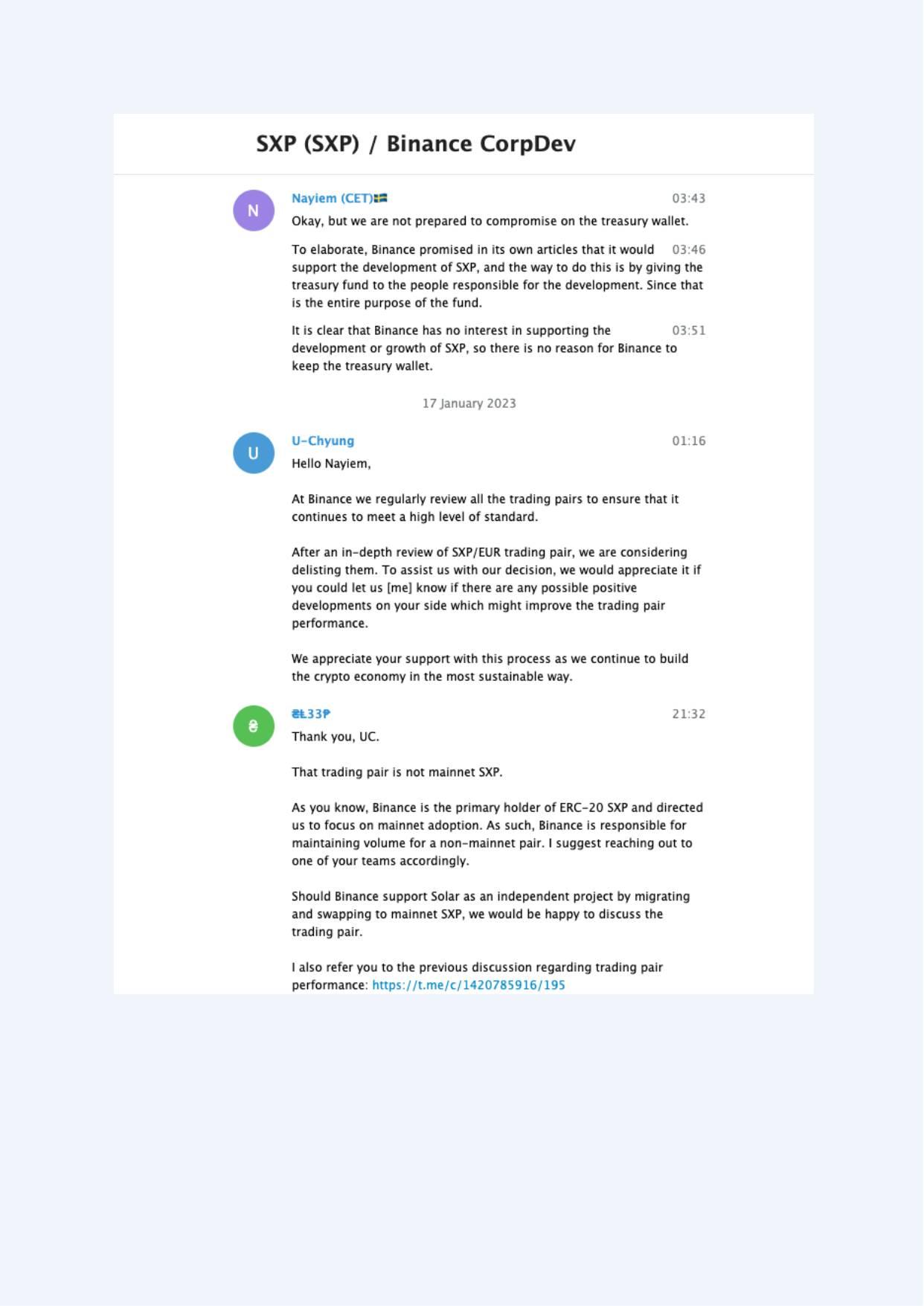

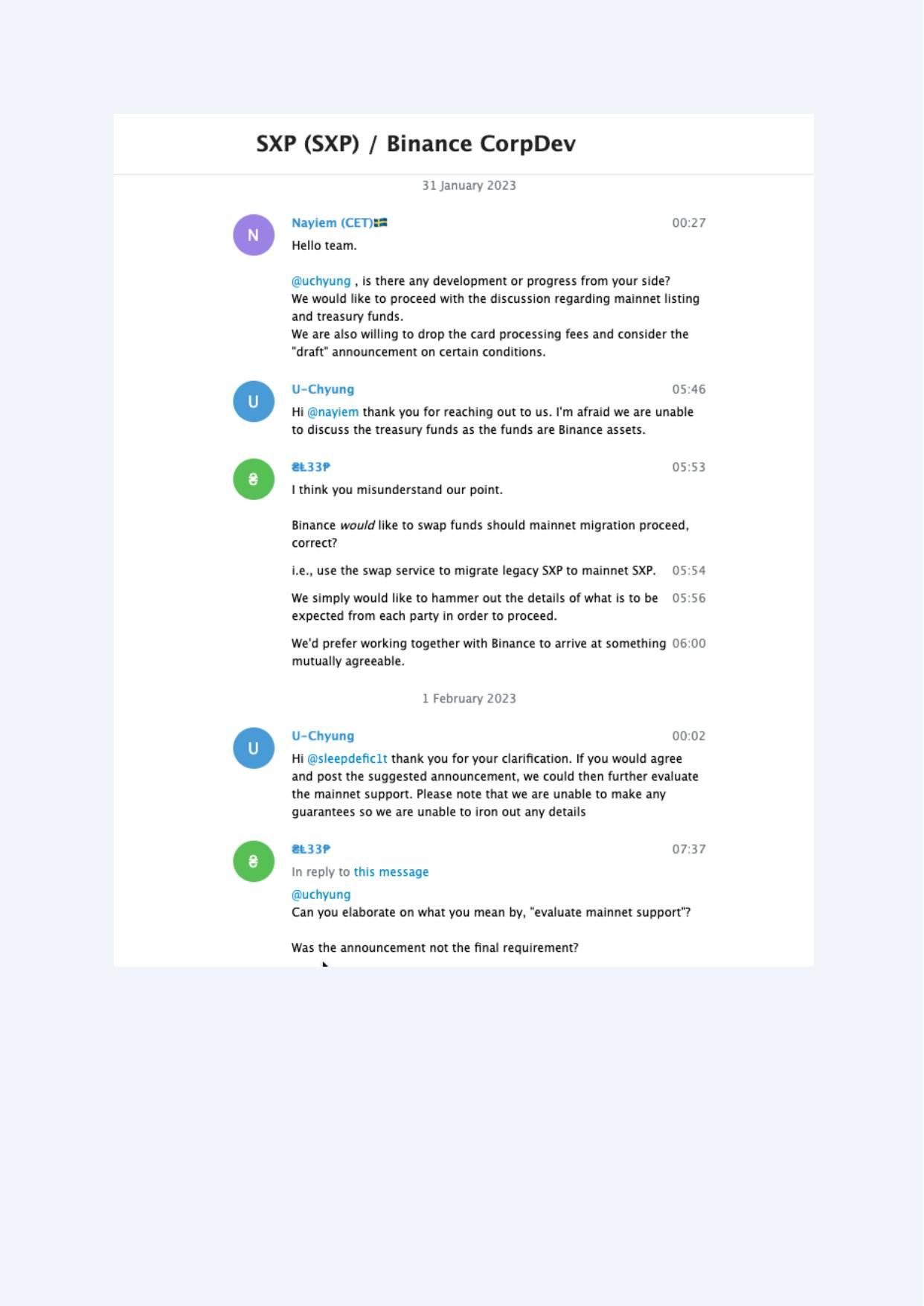

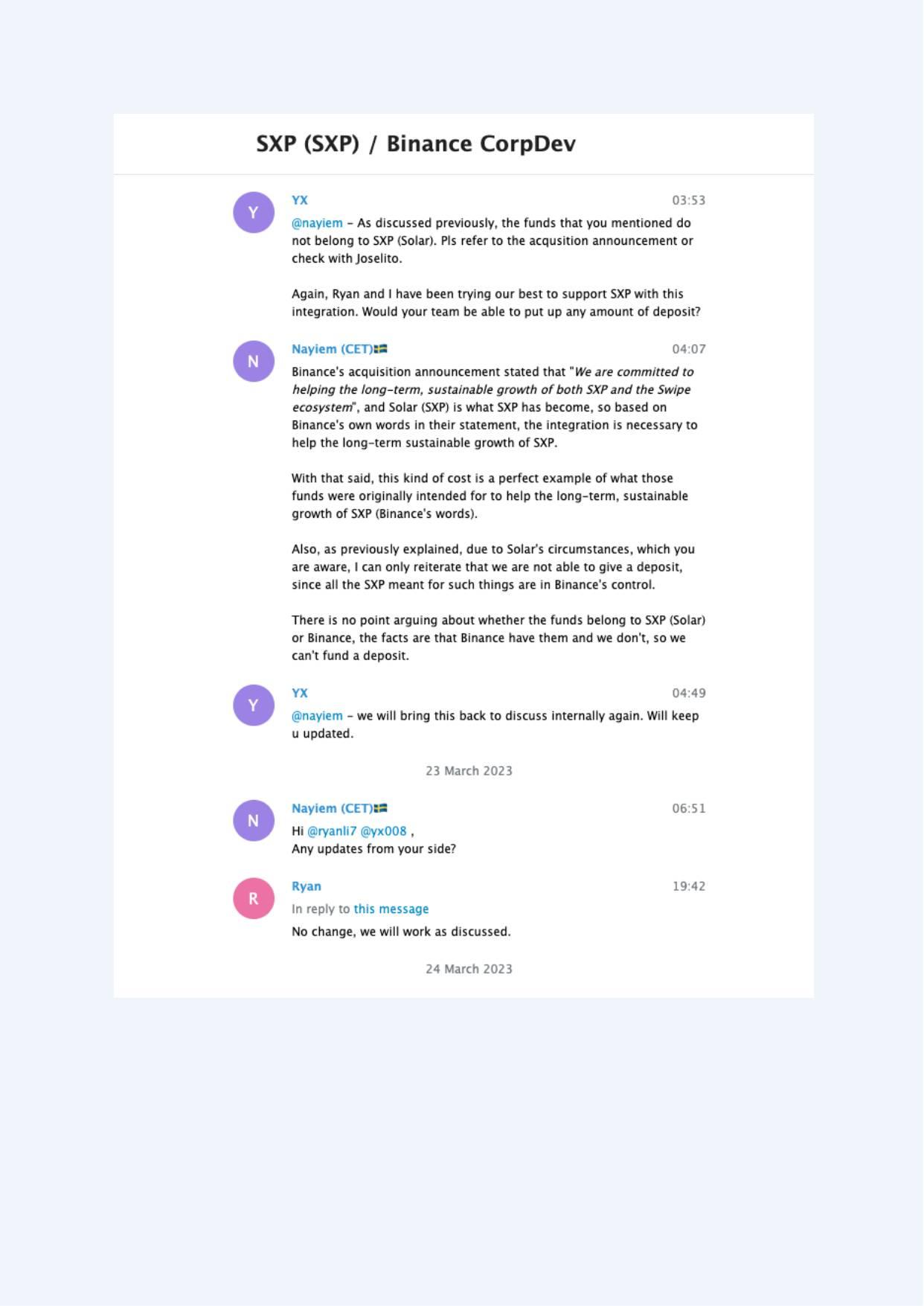

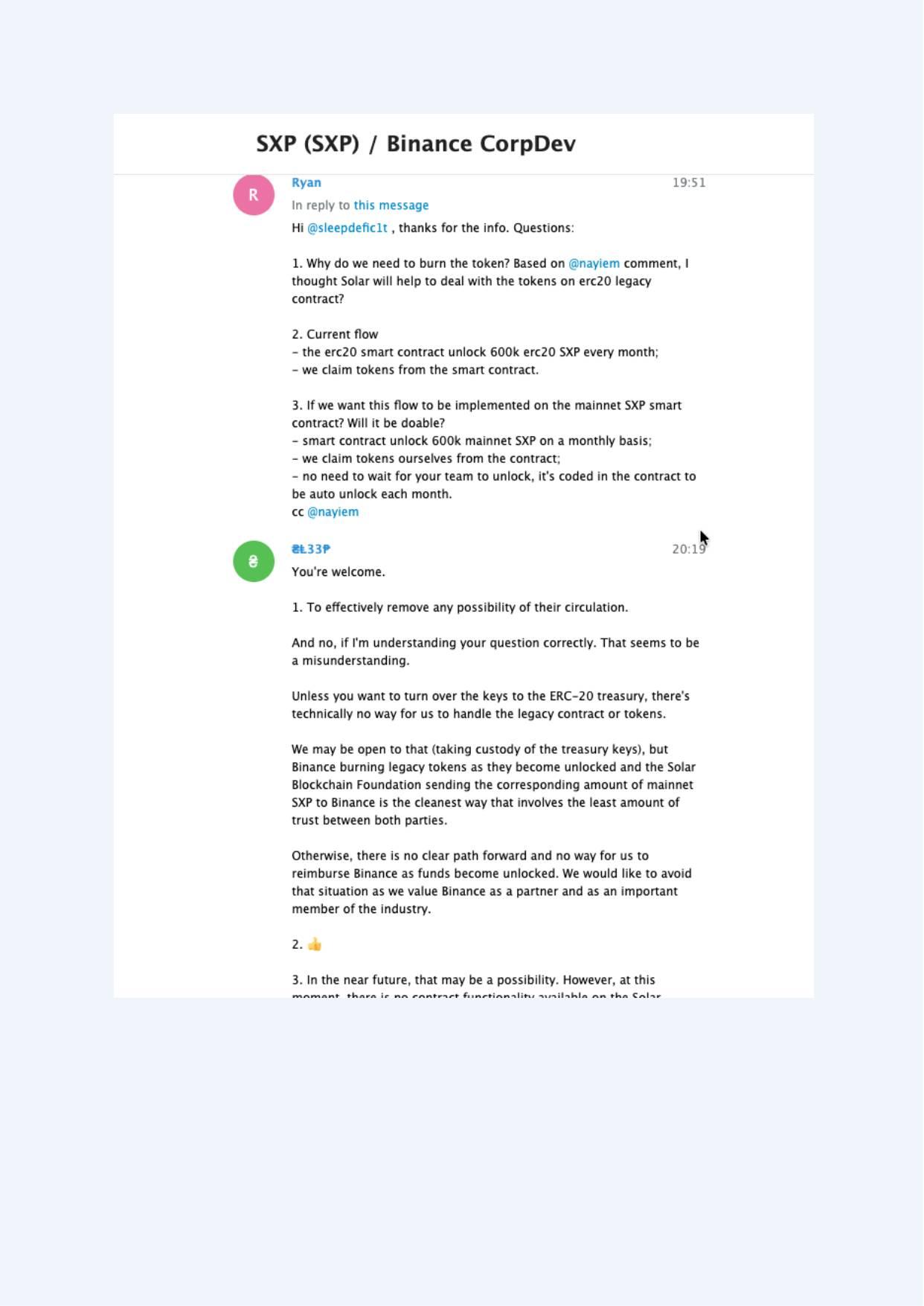

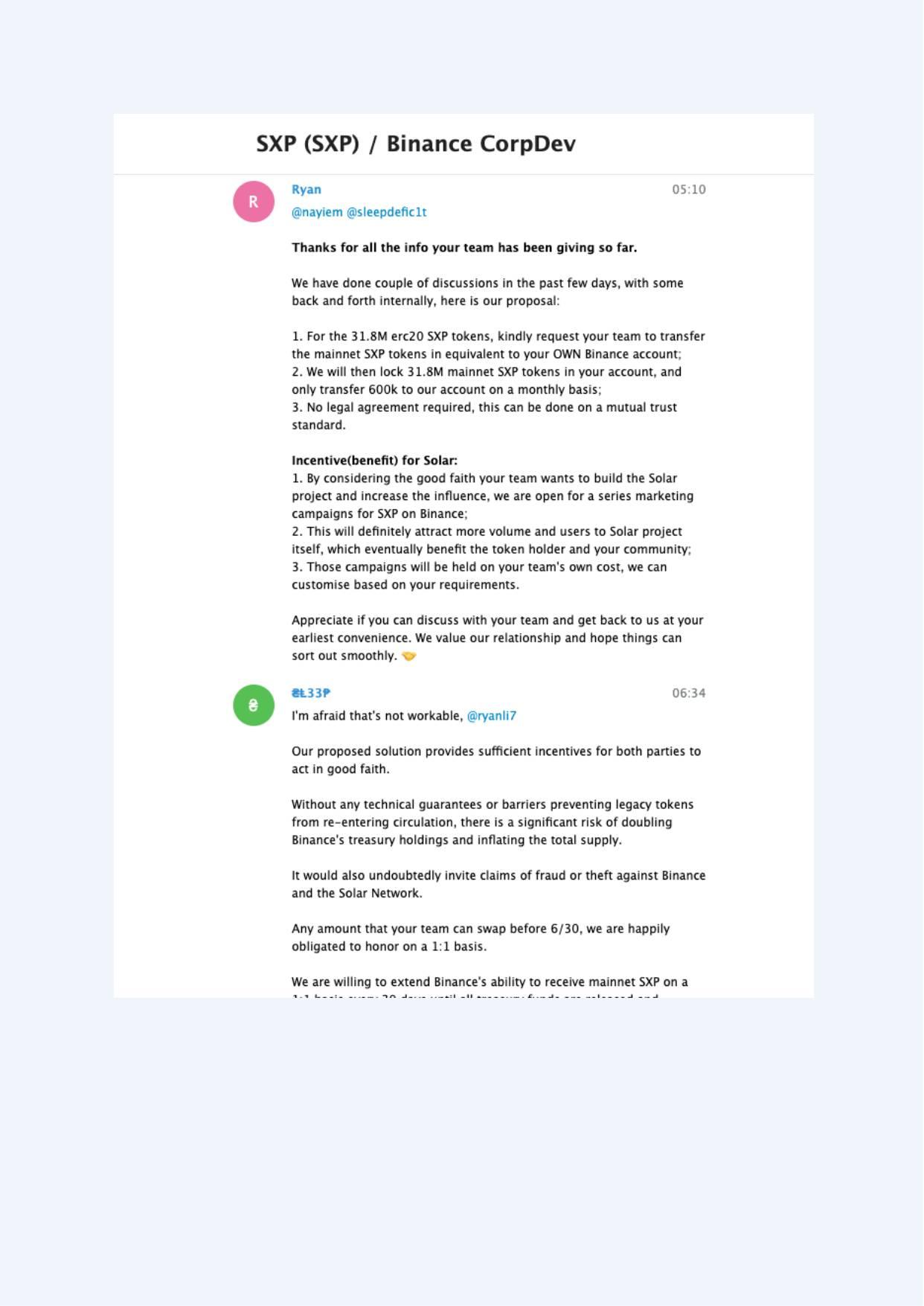

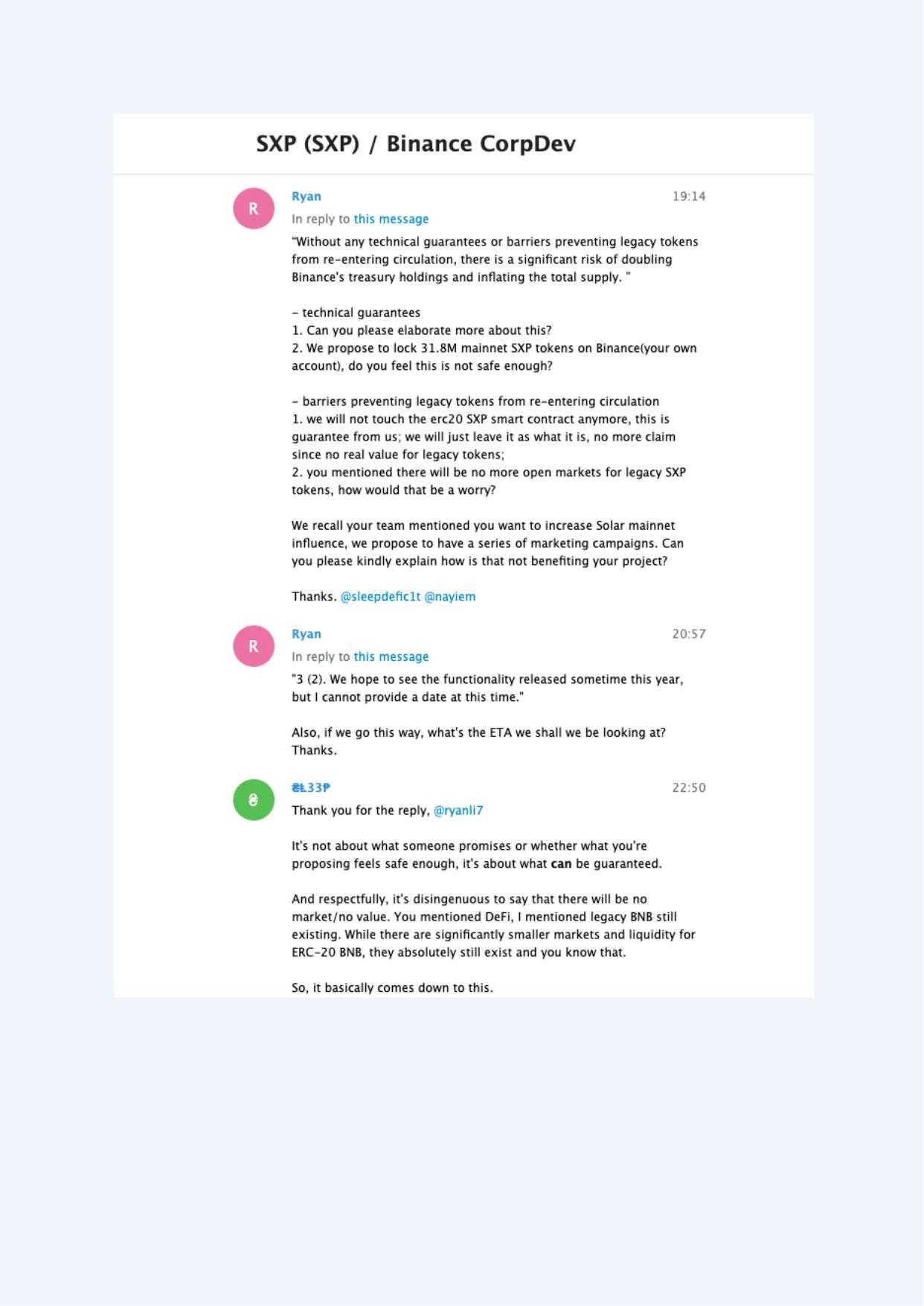

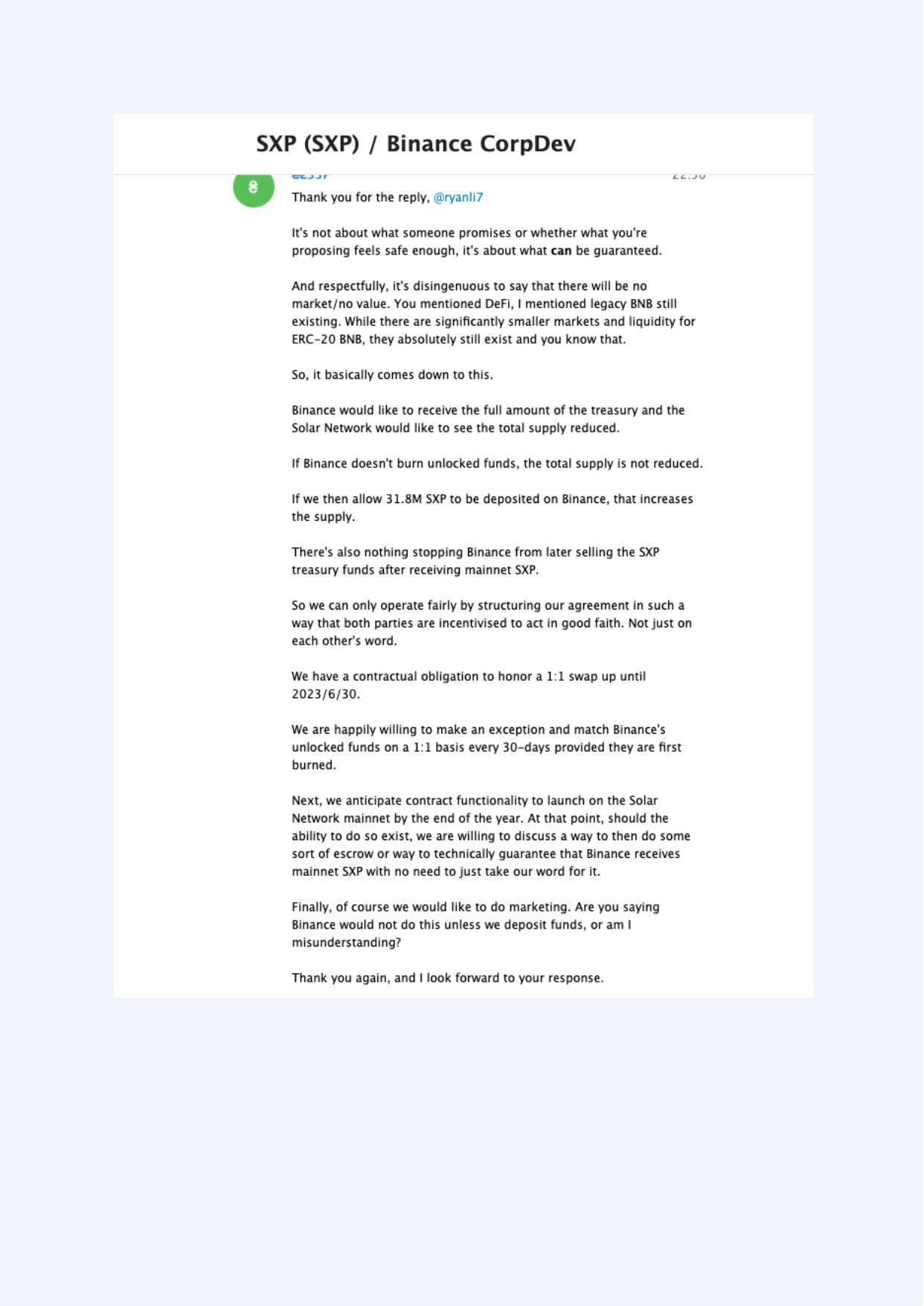

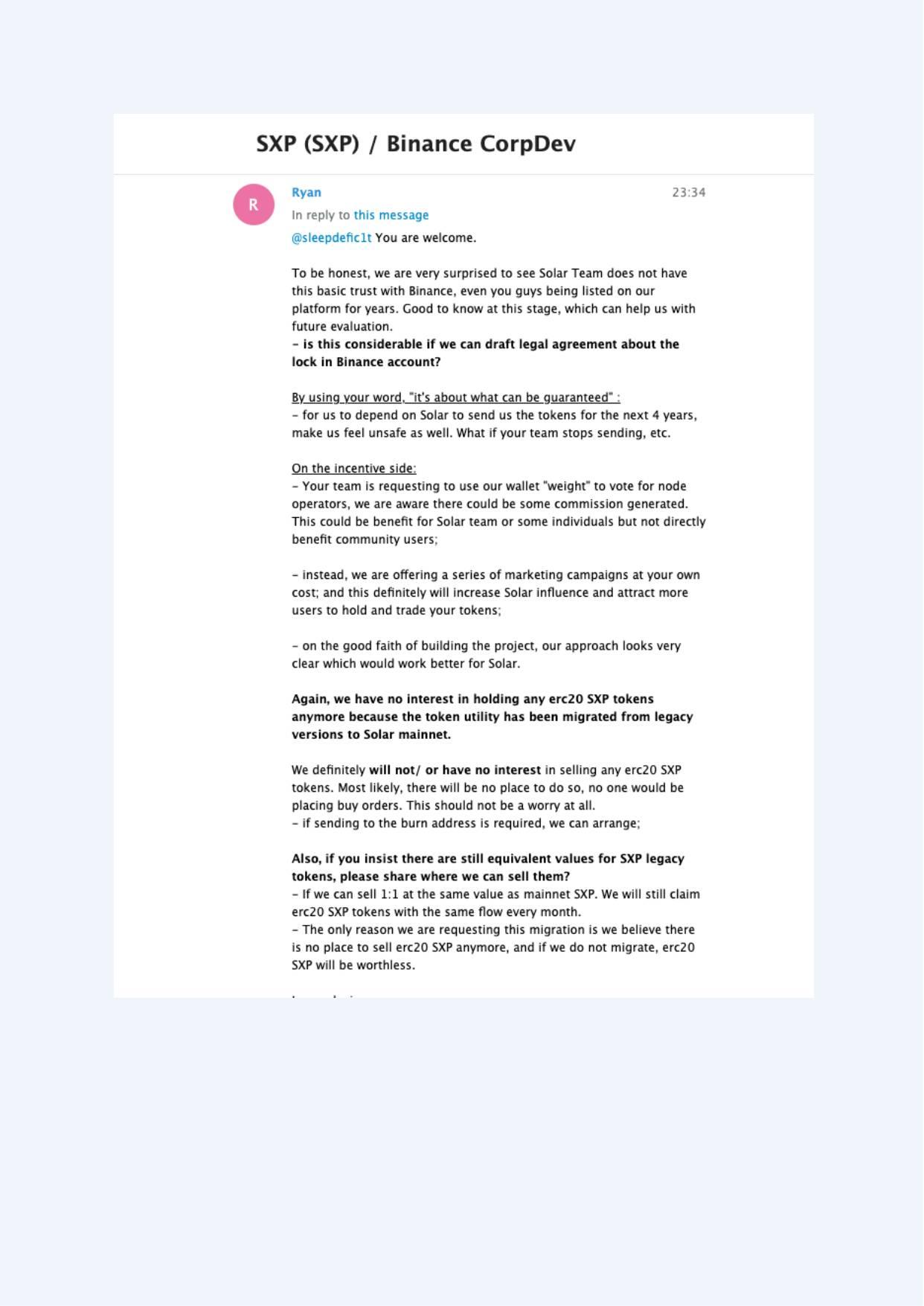

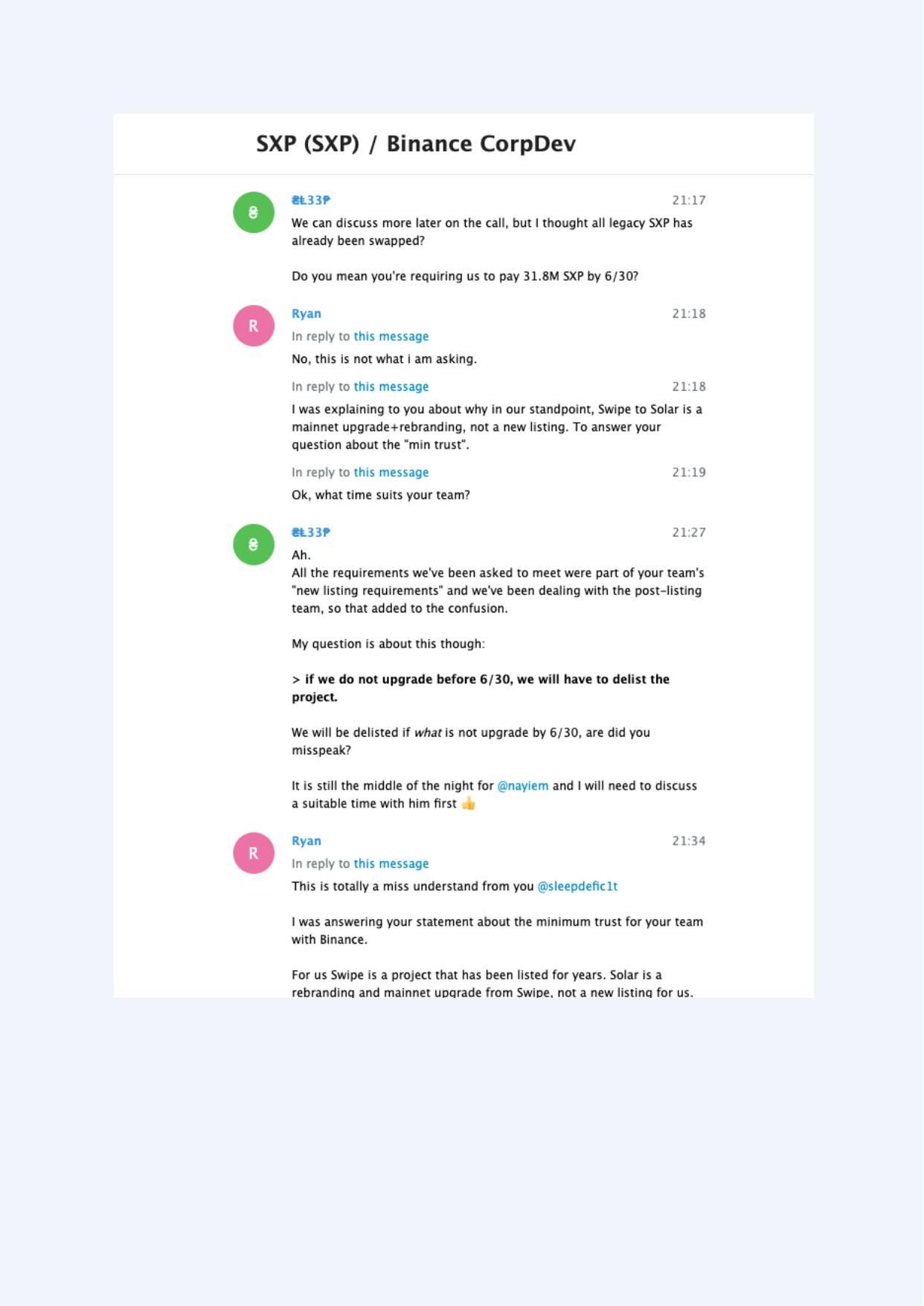

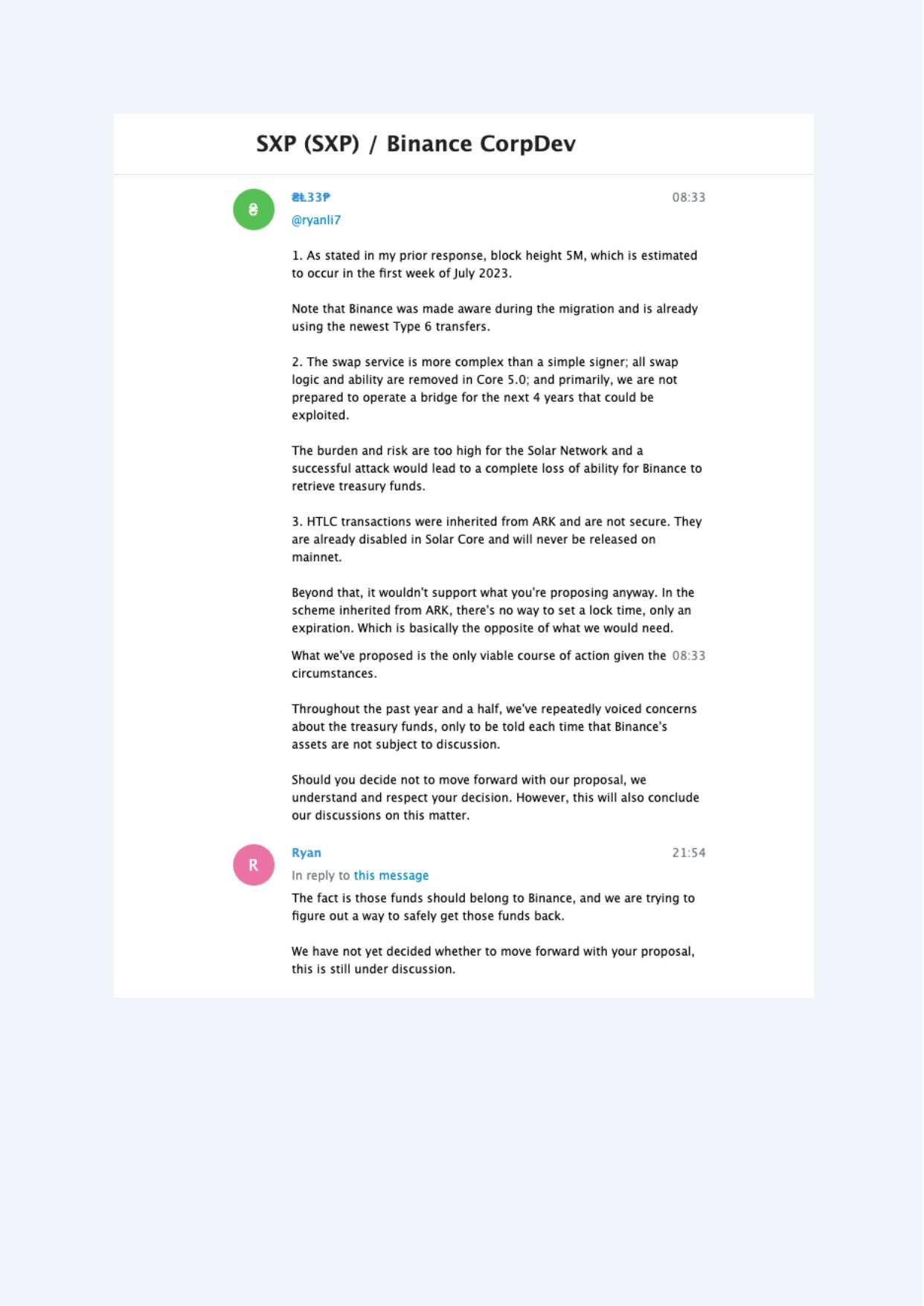

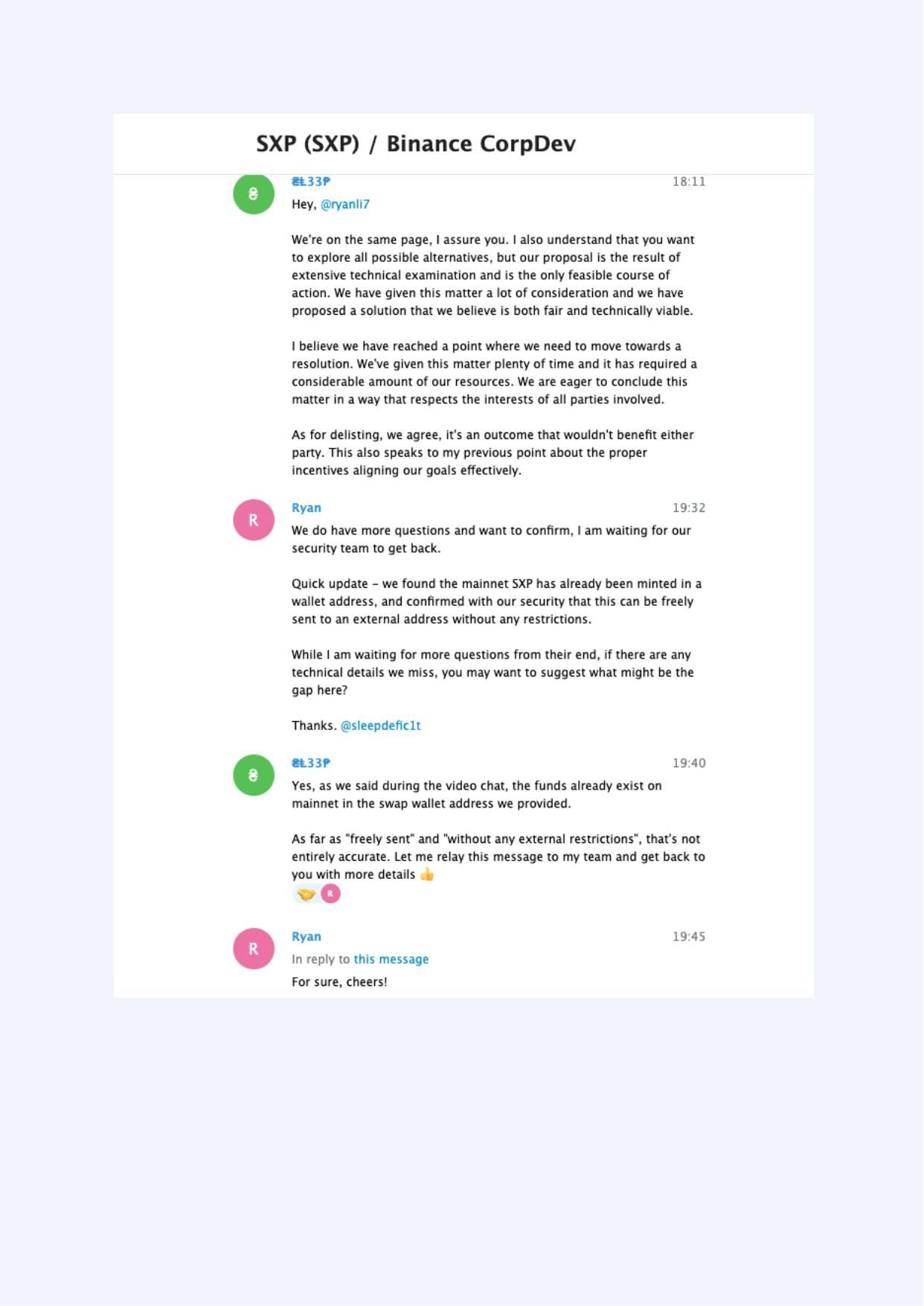

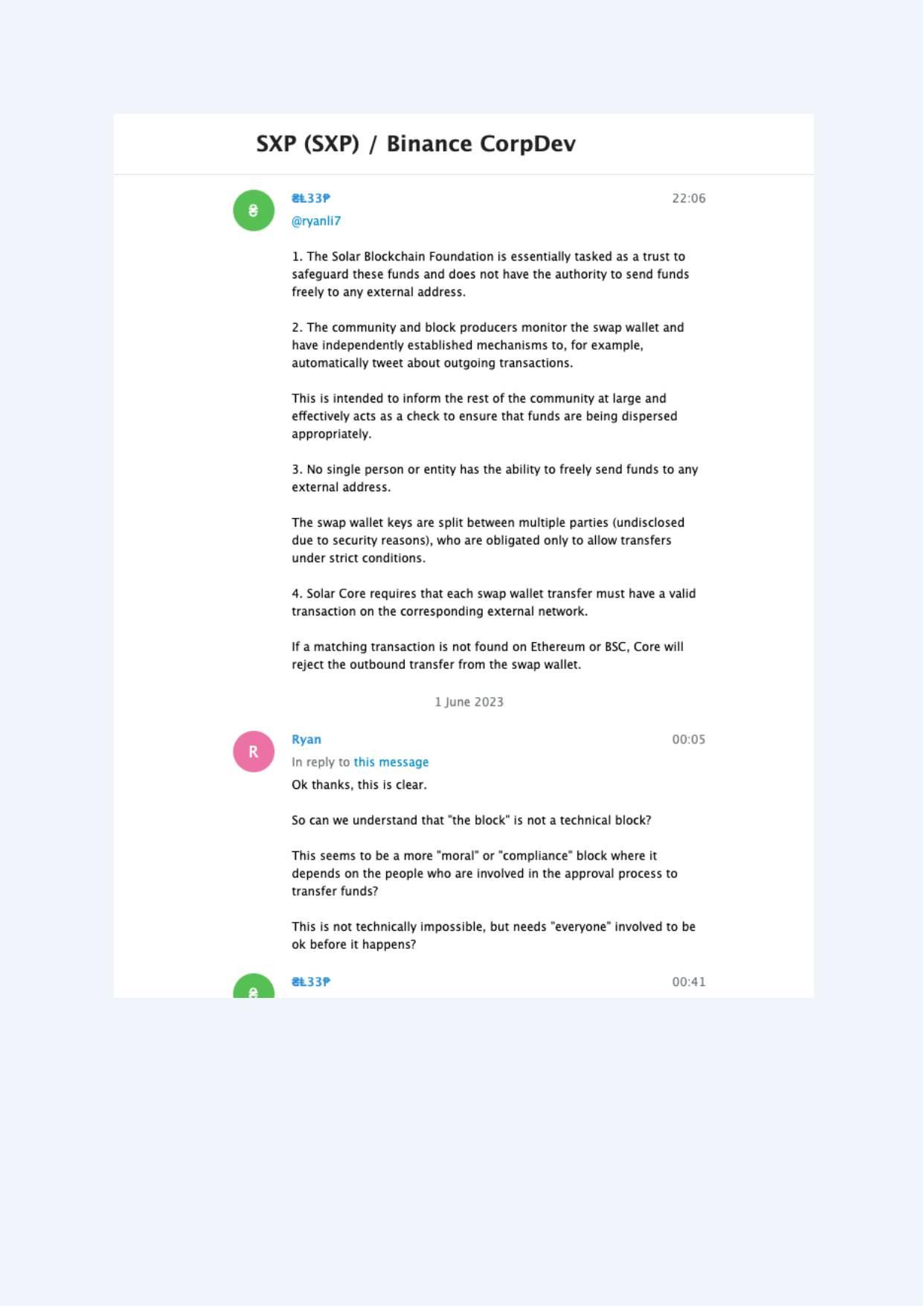

Across the evidence pack, references to card processing fees appear repeatedly, reflecting ongoing requests for confirmation regarding SXP utility and fee usage (e.g., Exhibits A-002, A-003, A-004, A-008, A-009, A-020, A-027, A-030, A-031, A-033).

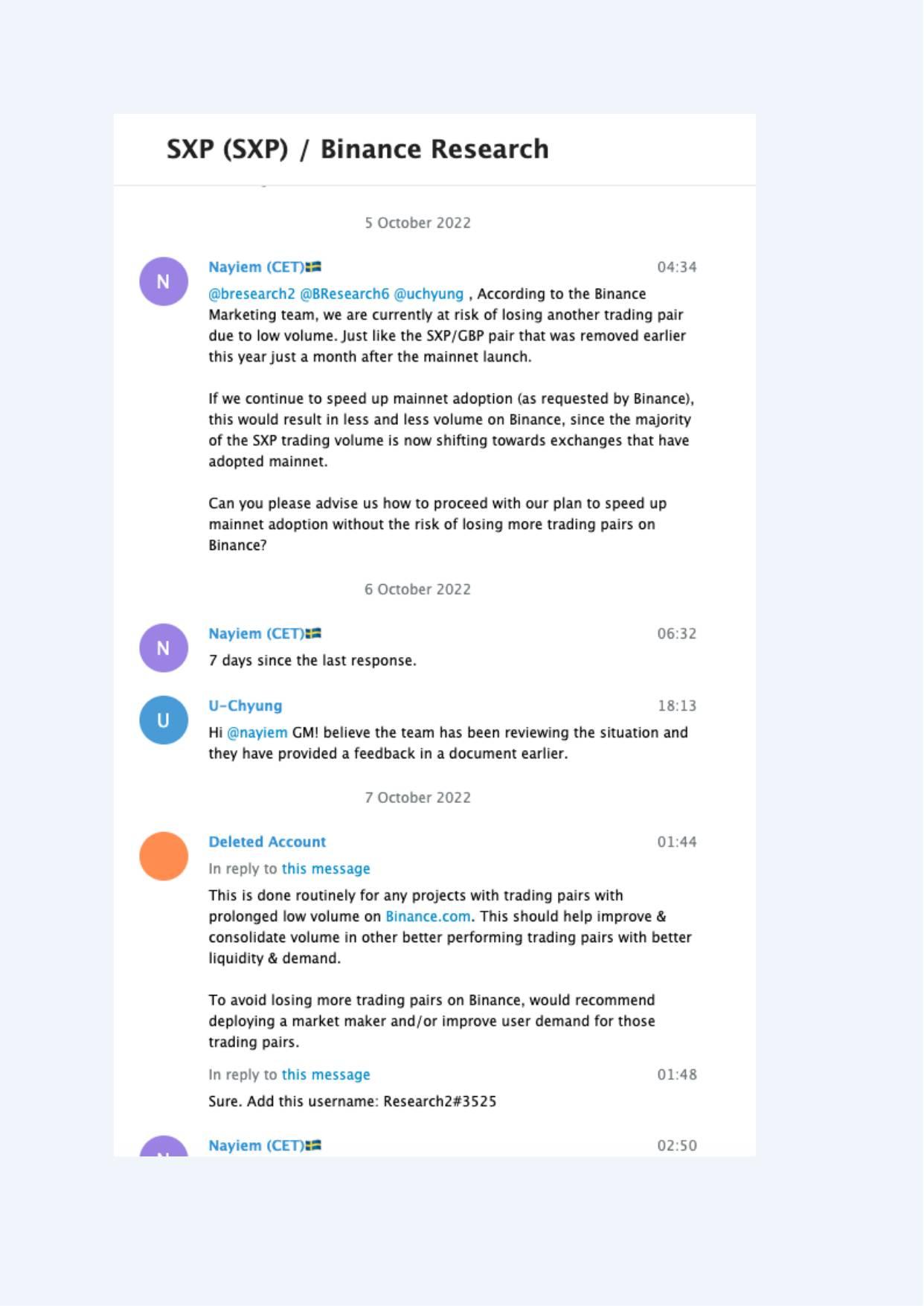

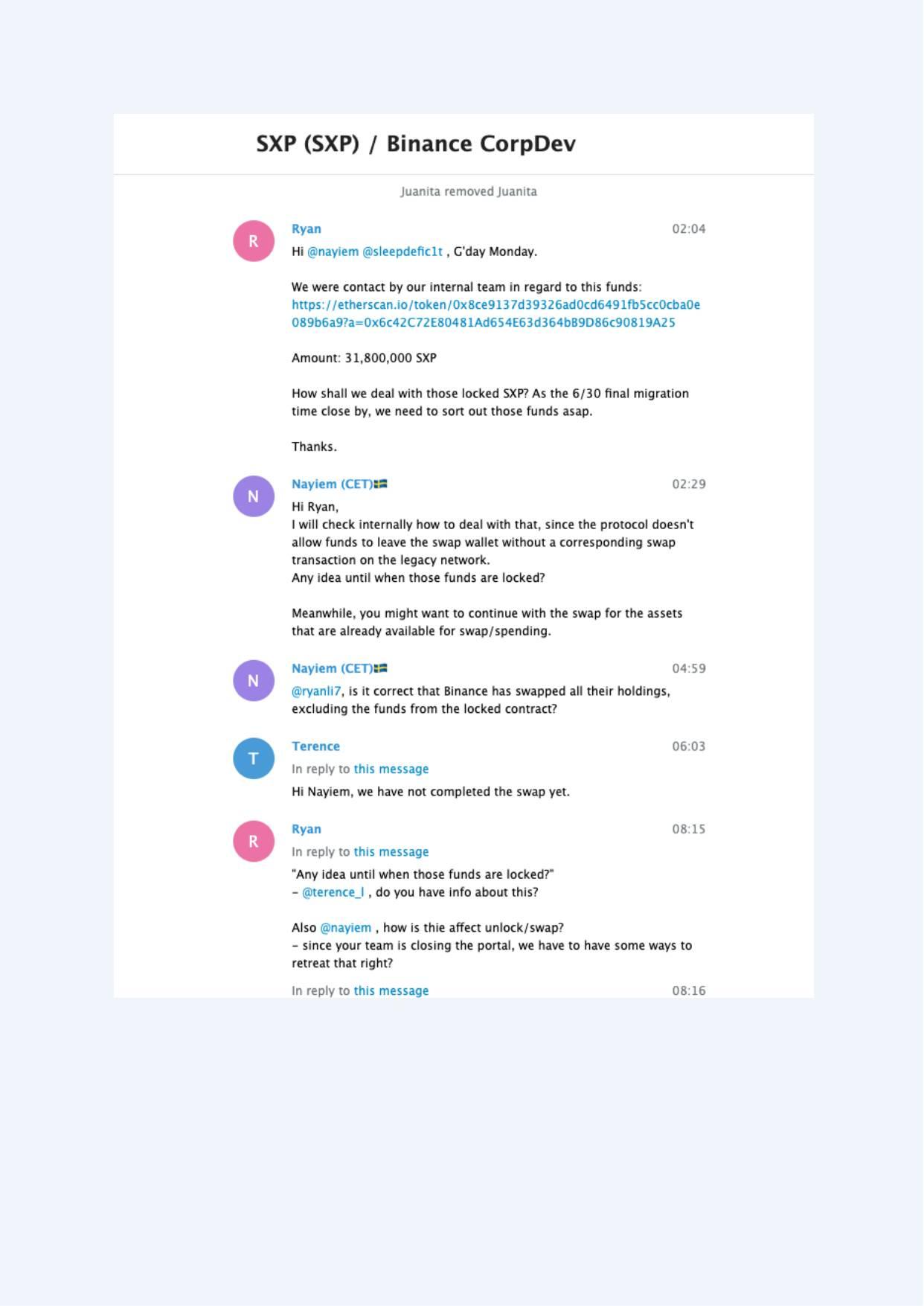

Treasury Custody and Listing Risk

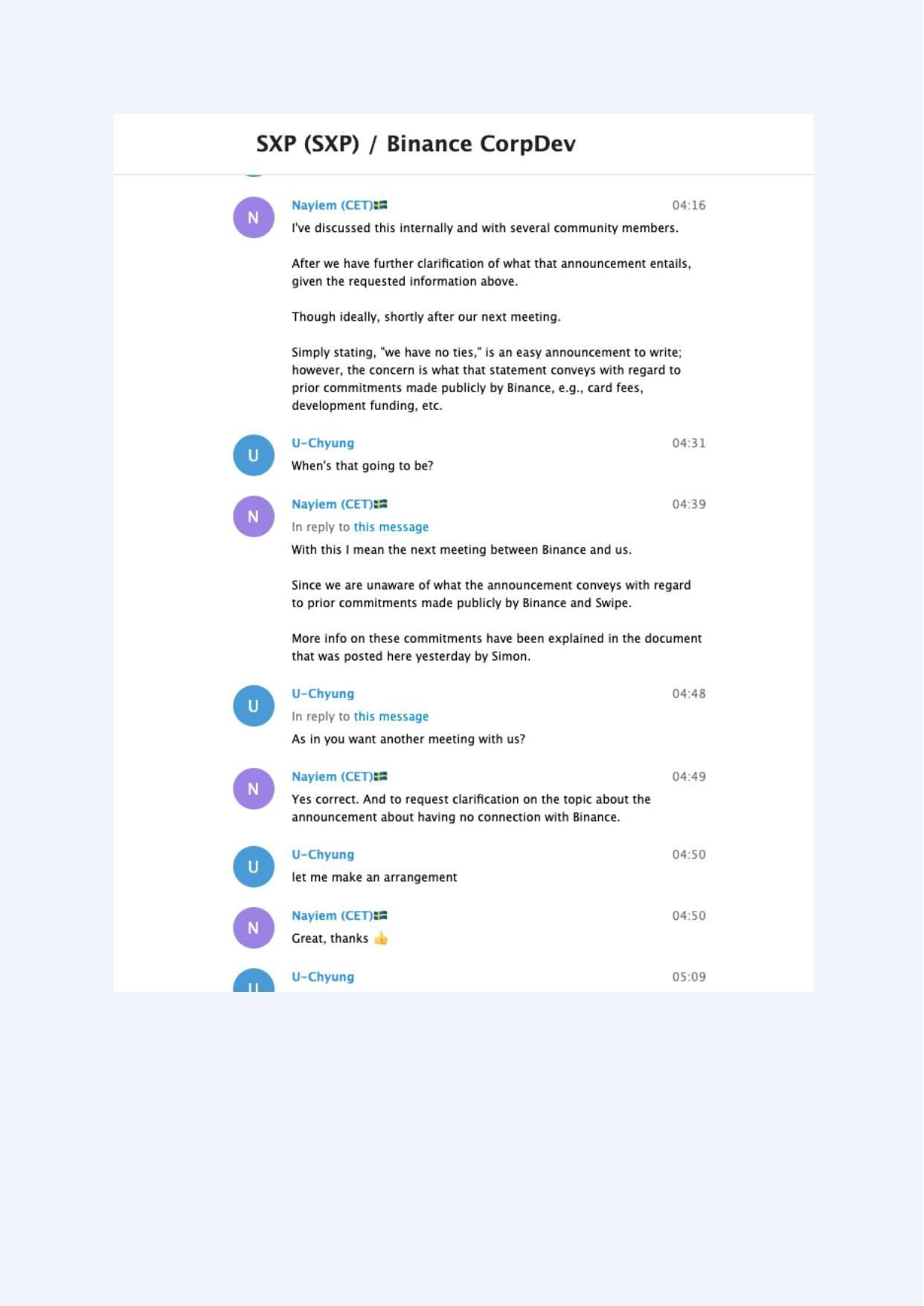

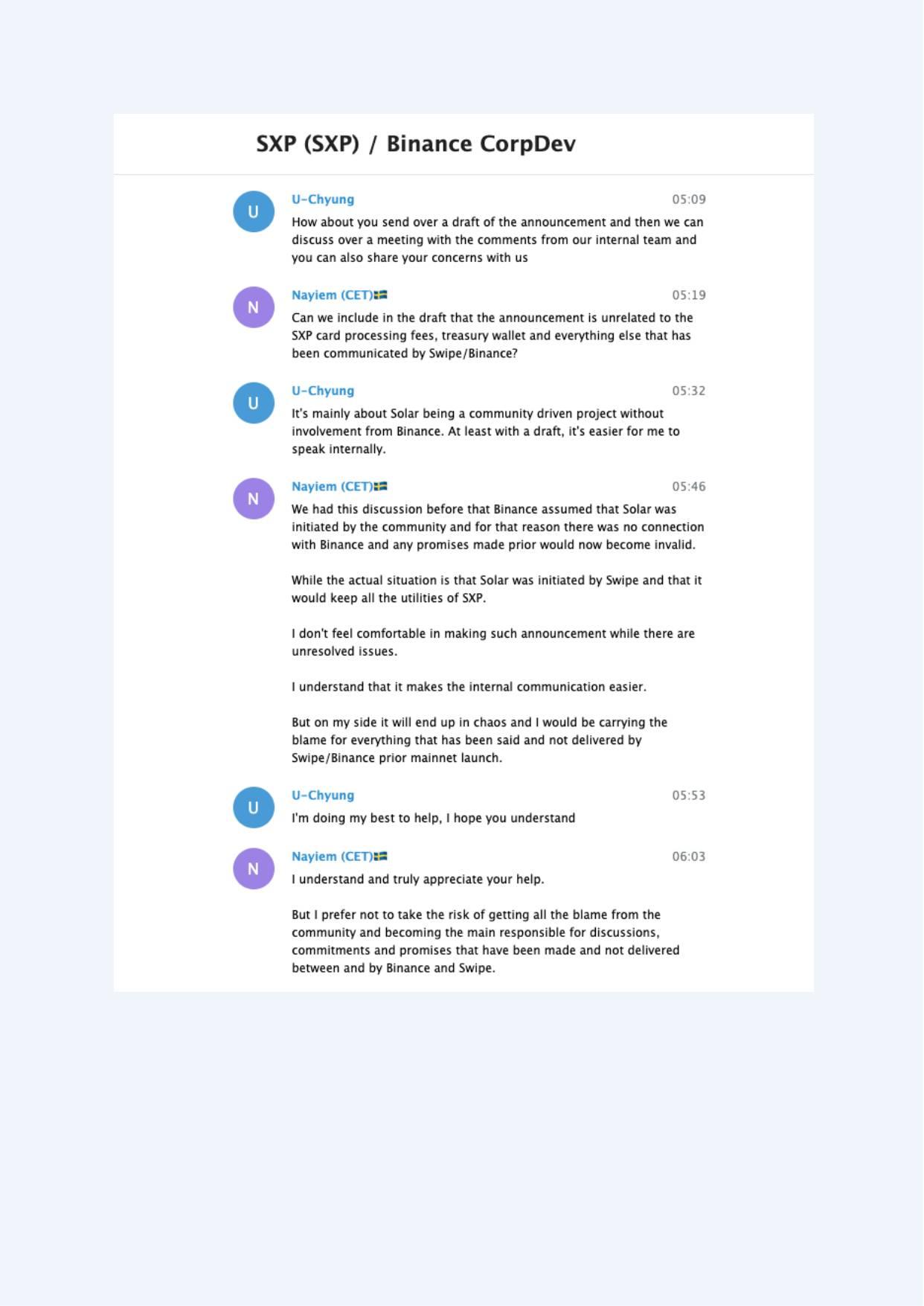

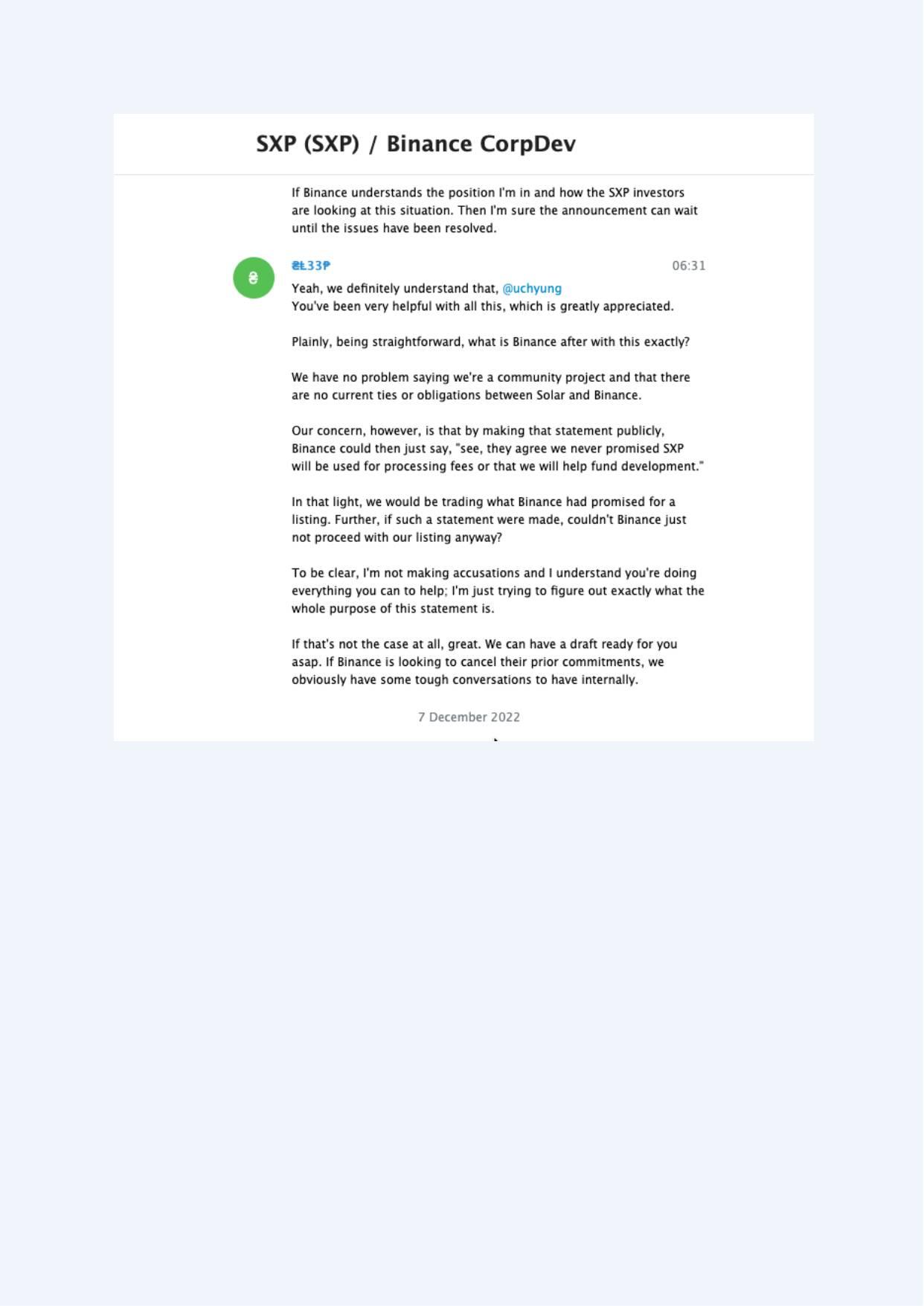

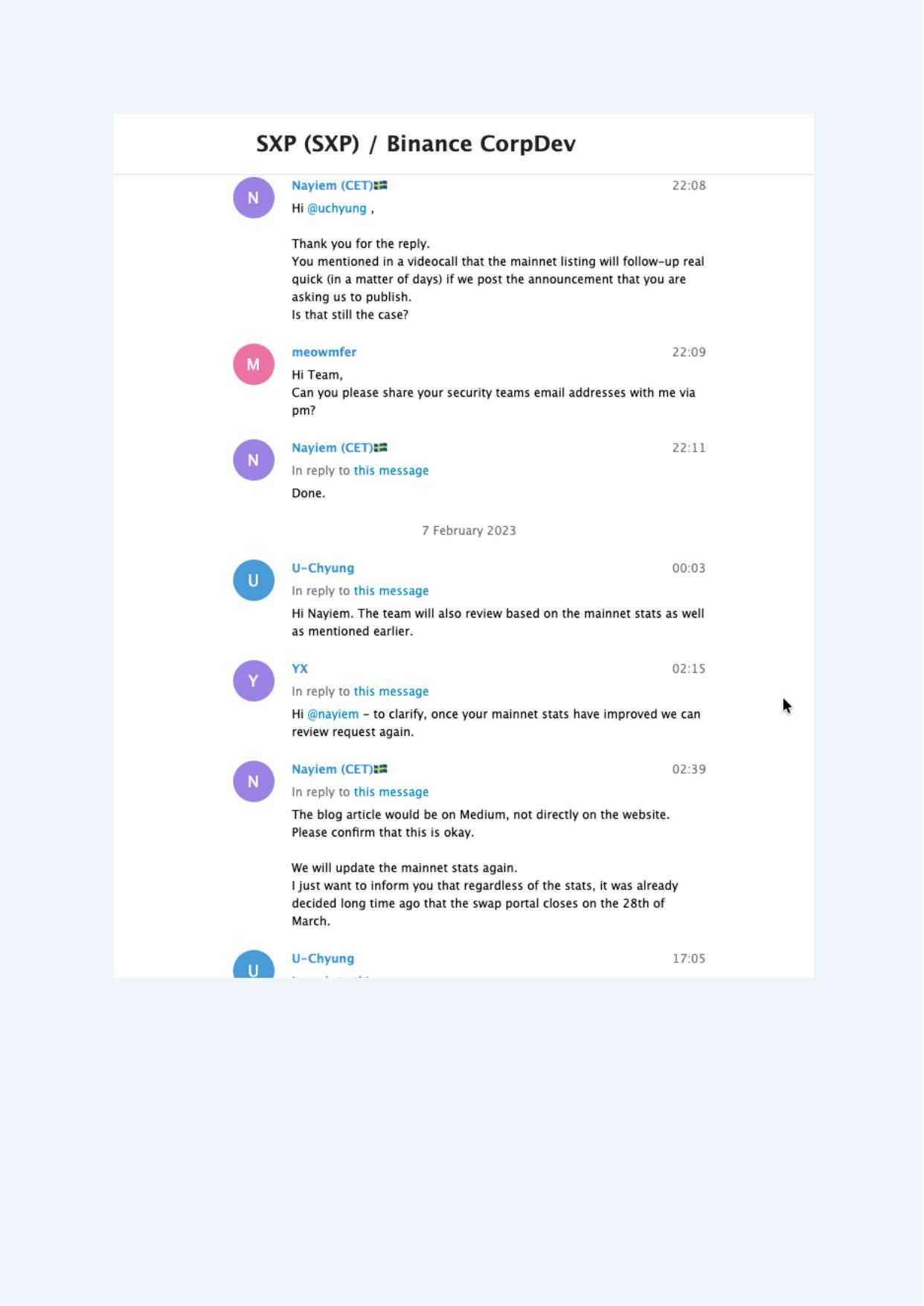

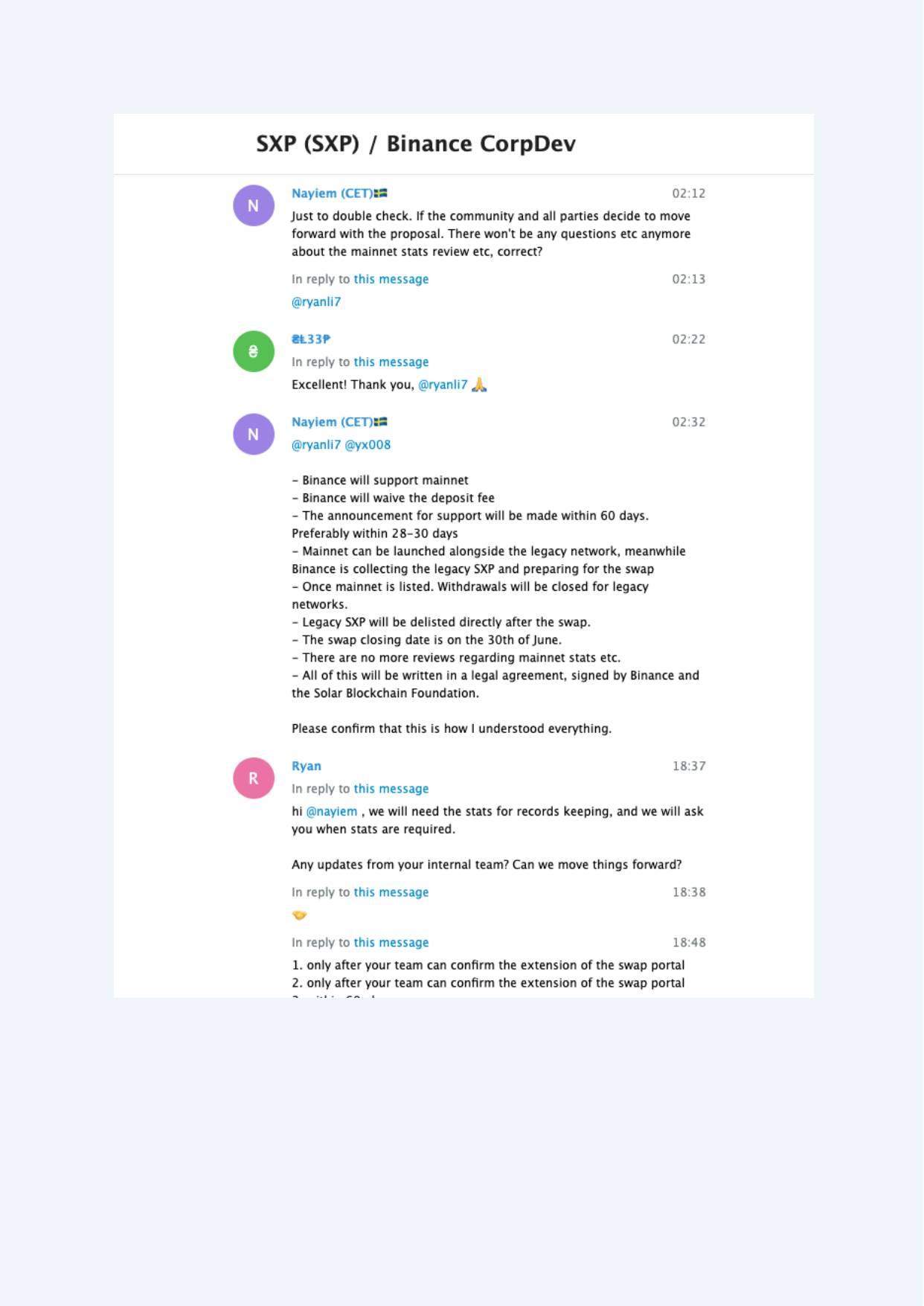

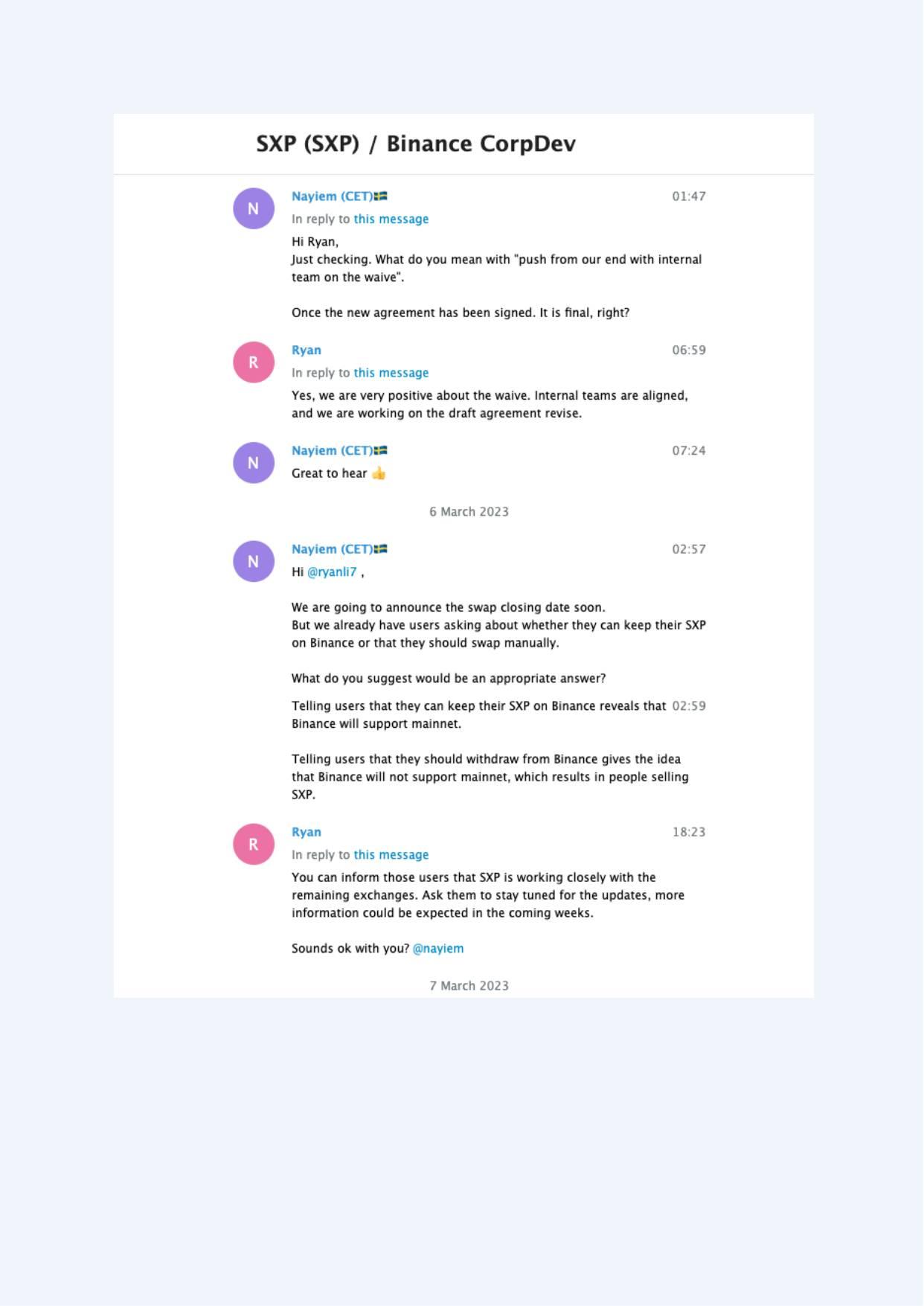

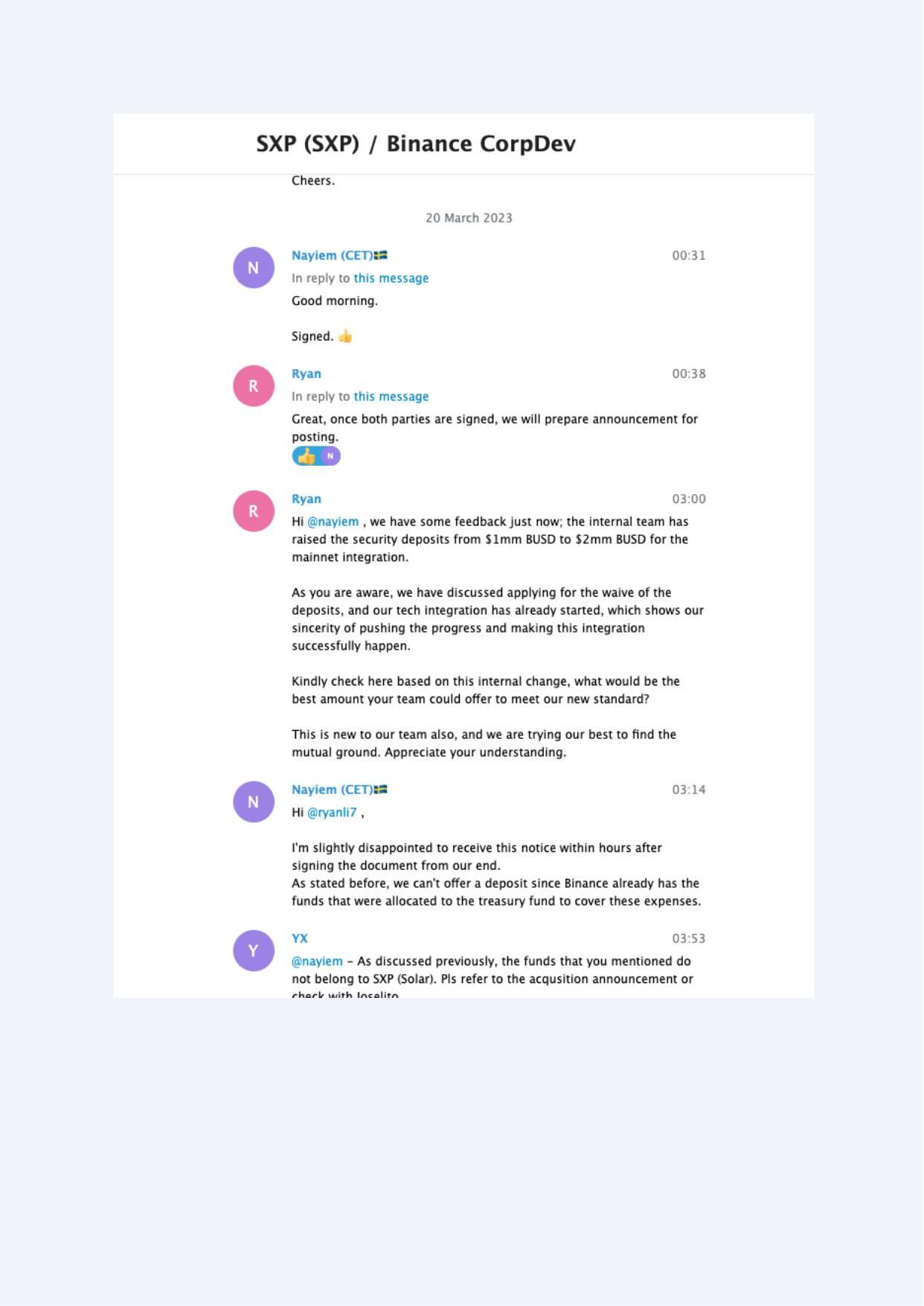

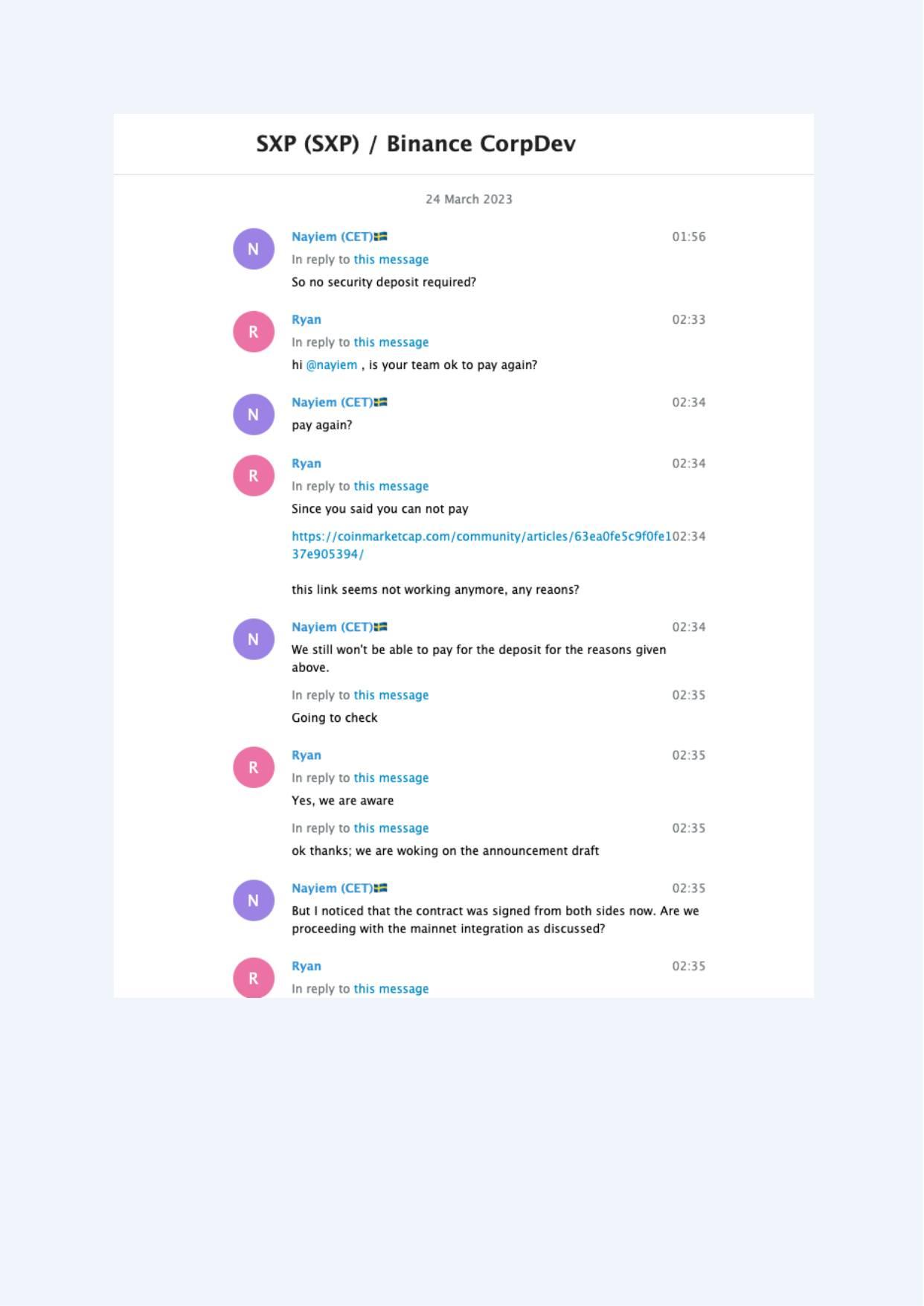

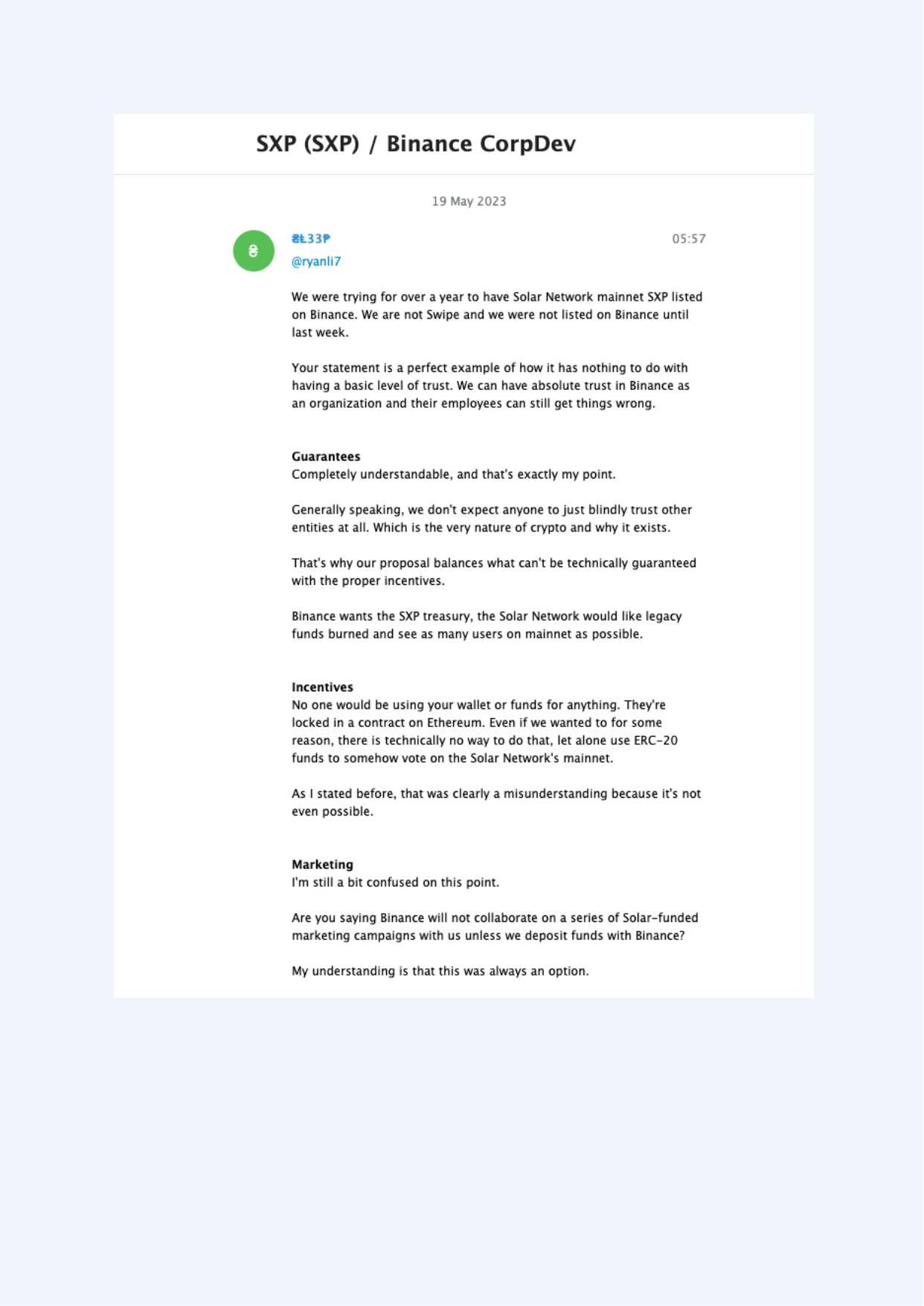

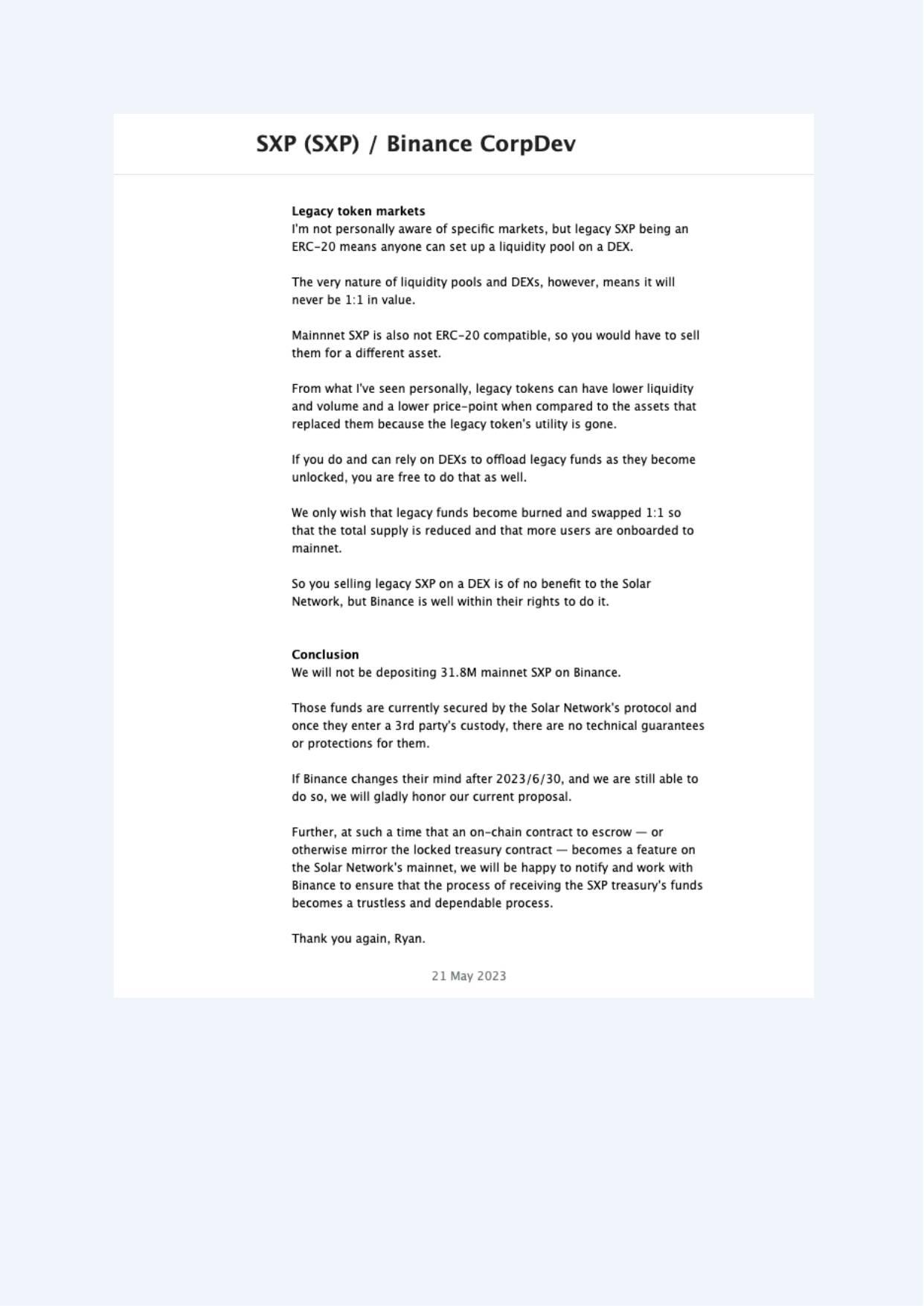

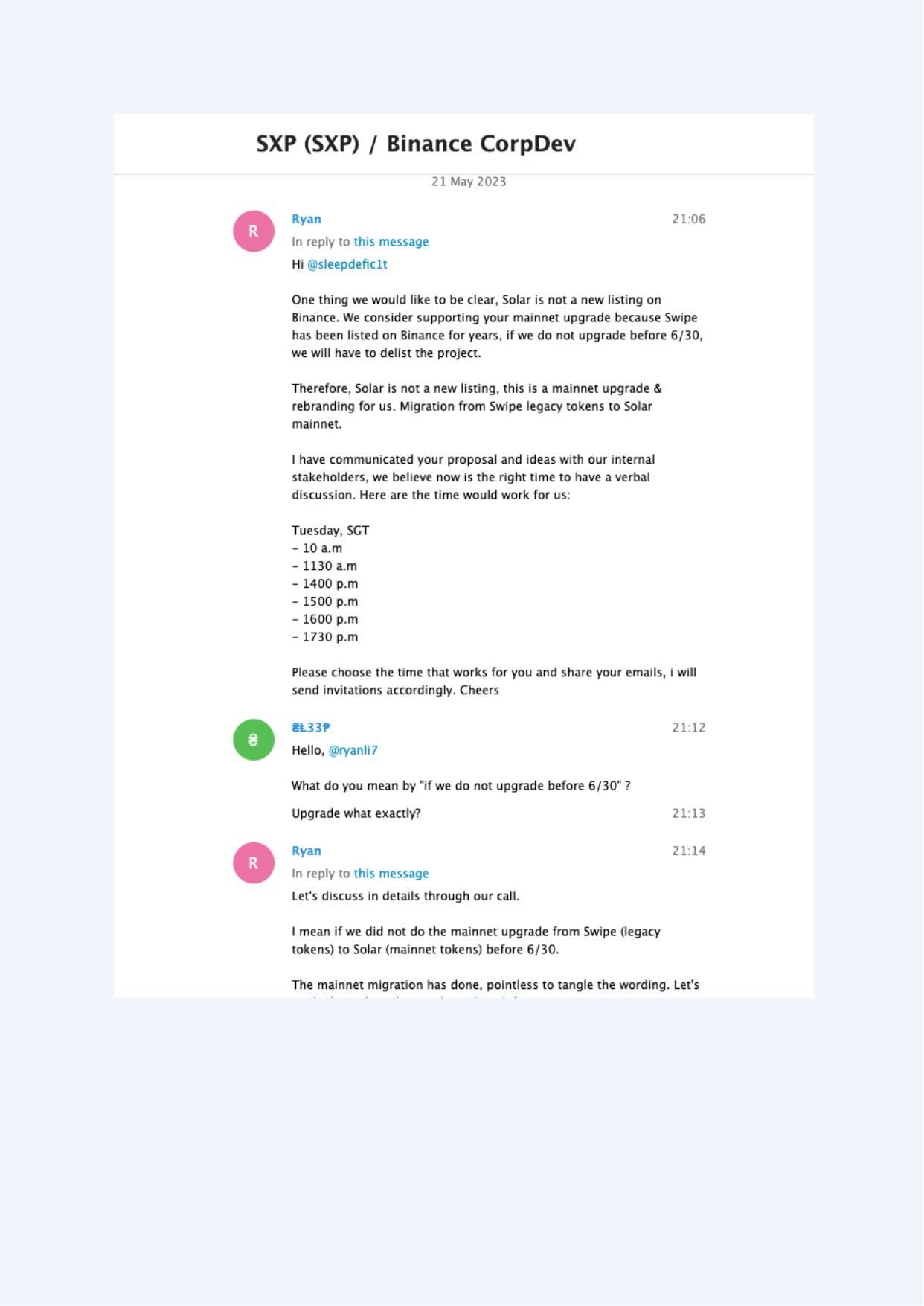

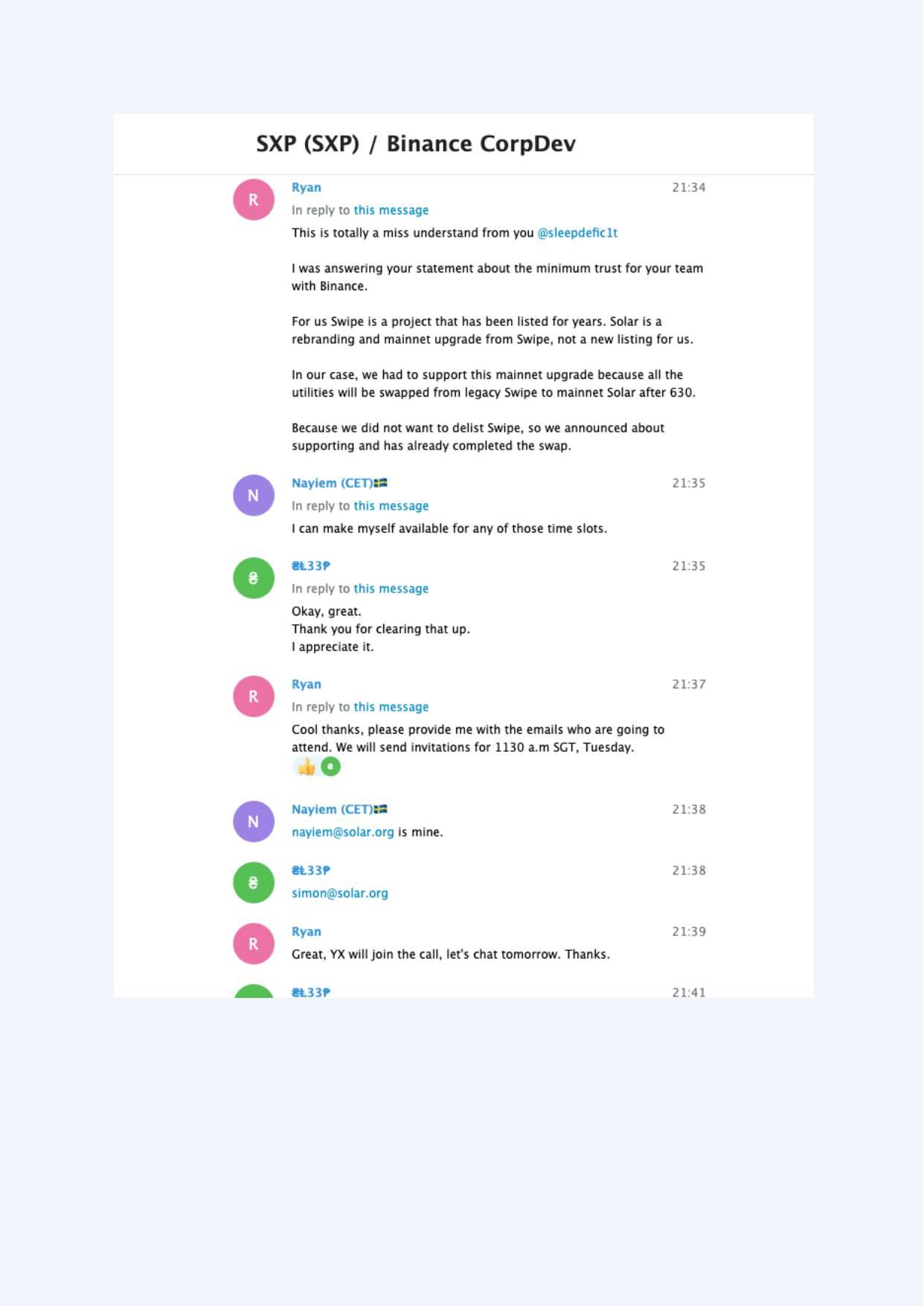

Communications show ongoing discussions regarding treasury custody alongside references to potential delisting during periods of dispute (Exhibit A-032). Solar leadership later indicated that treasury-related inquiries were reduced due to perceived listing risk (Exhibit A-063).

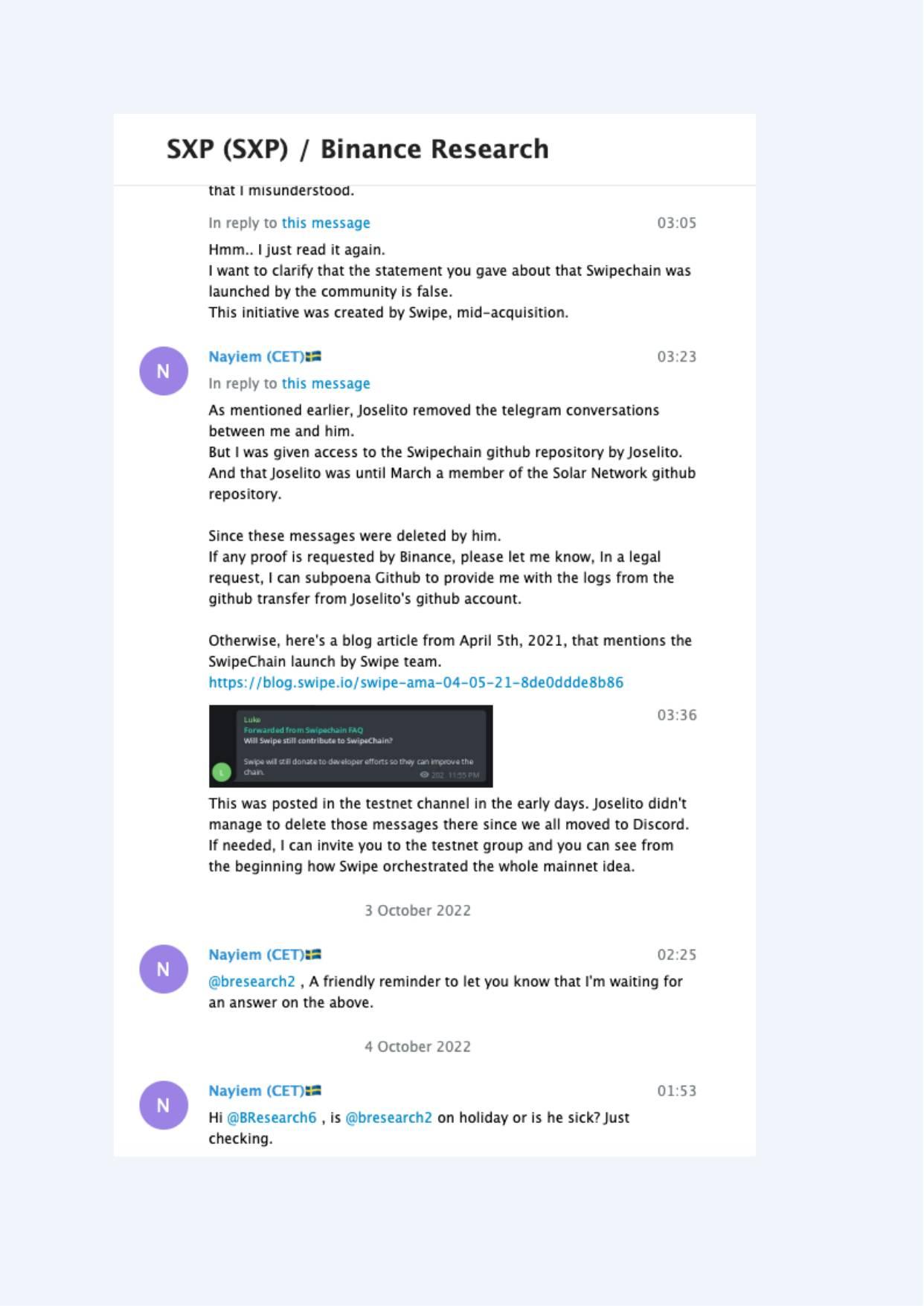

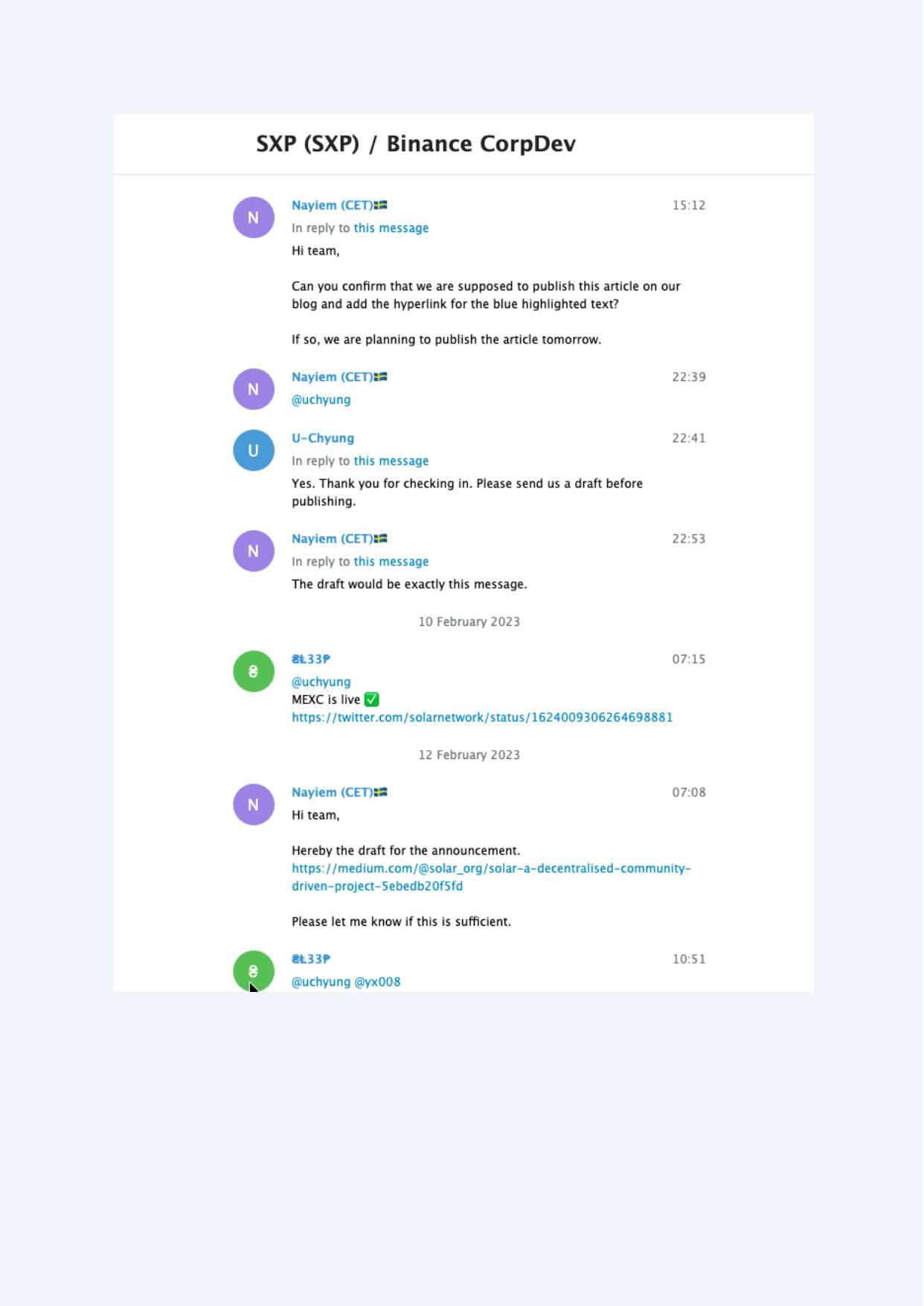

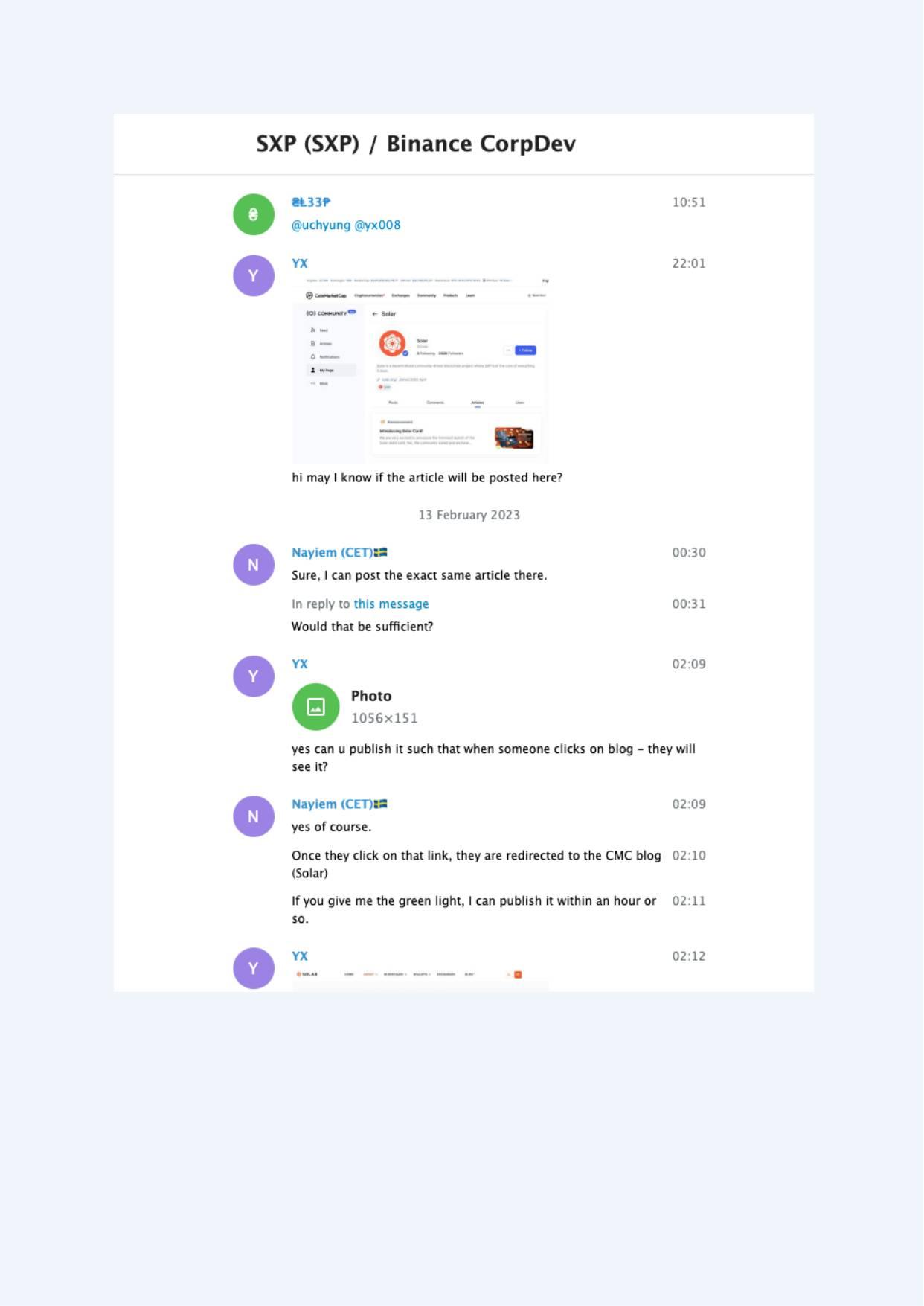

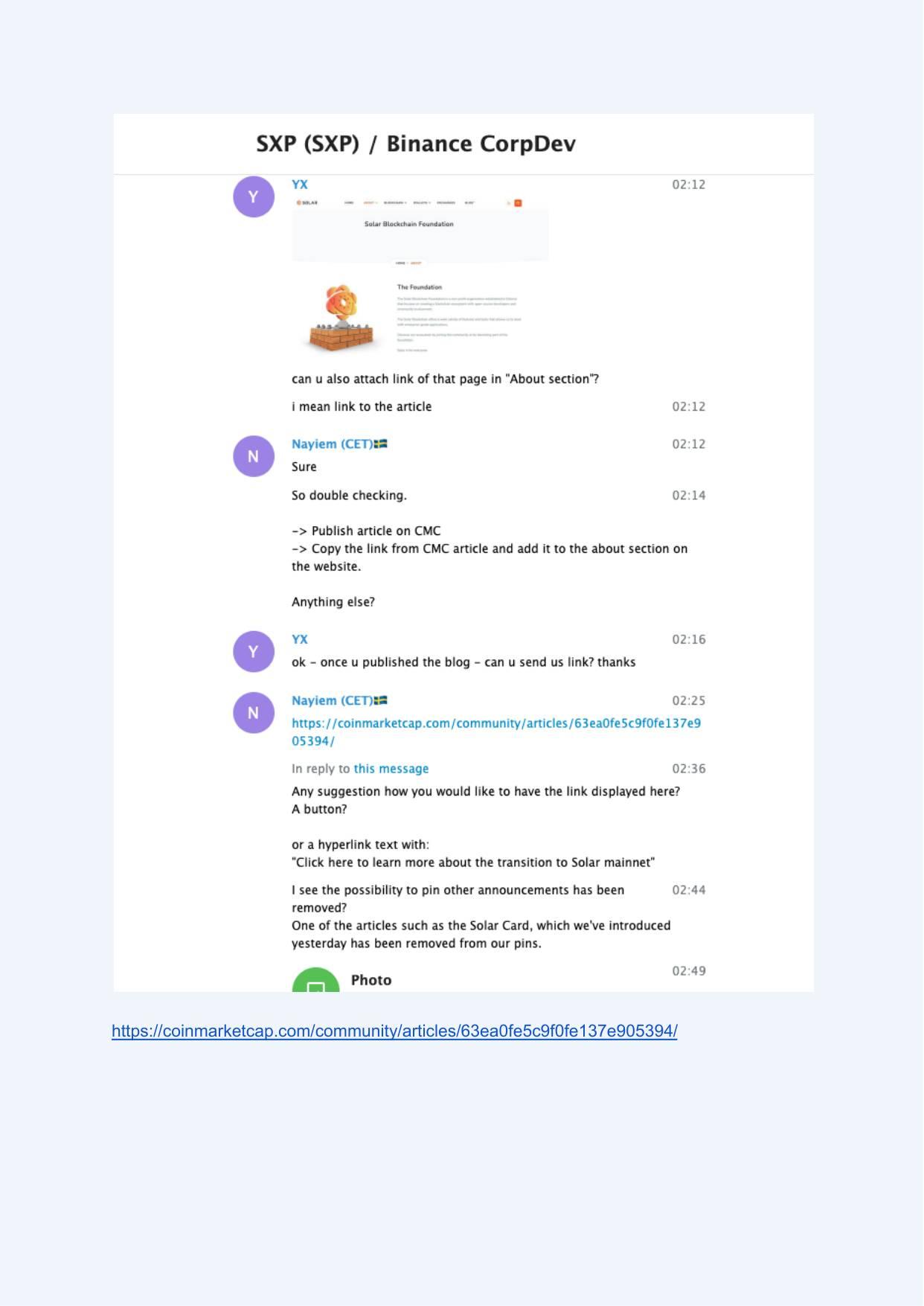

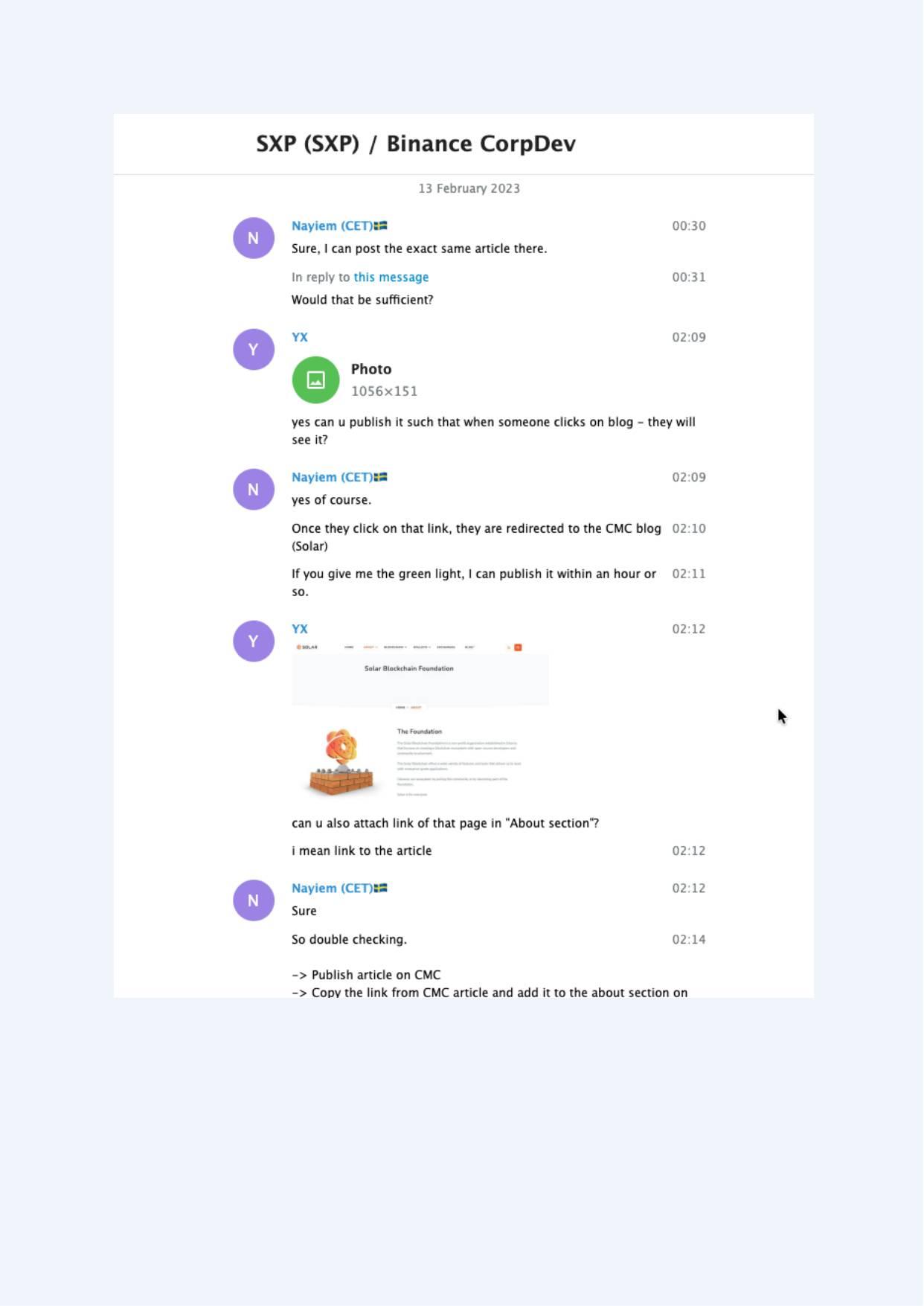

Messaging Coordination

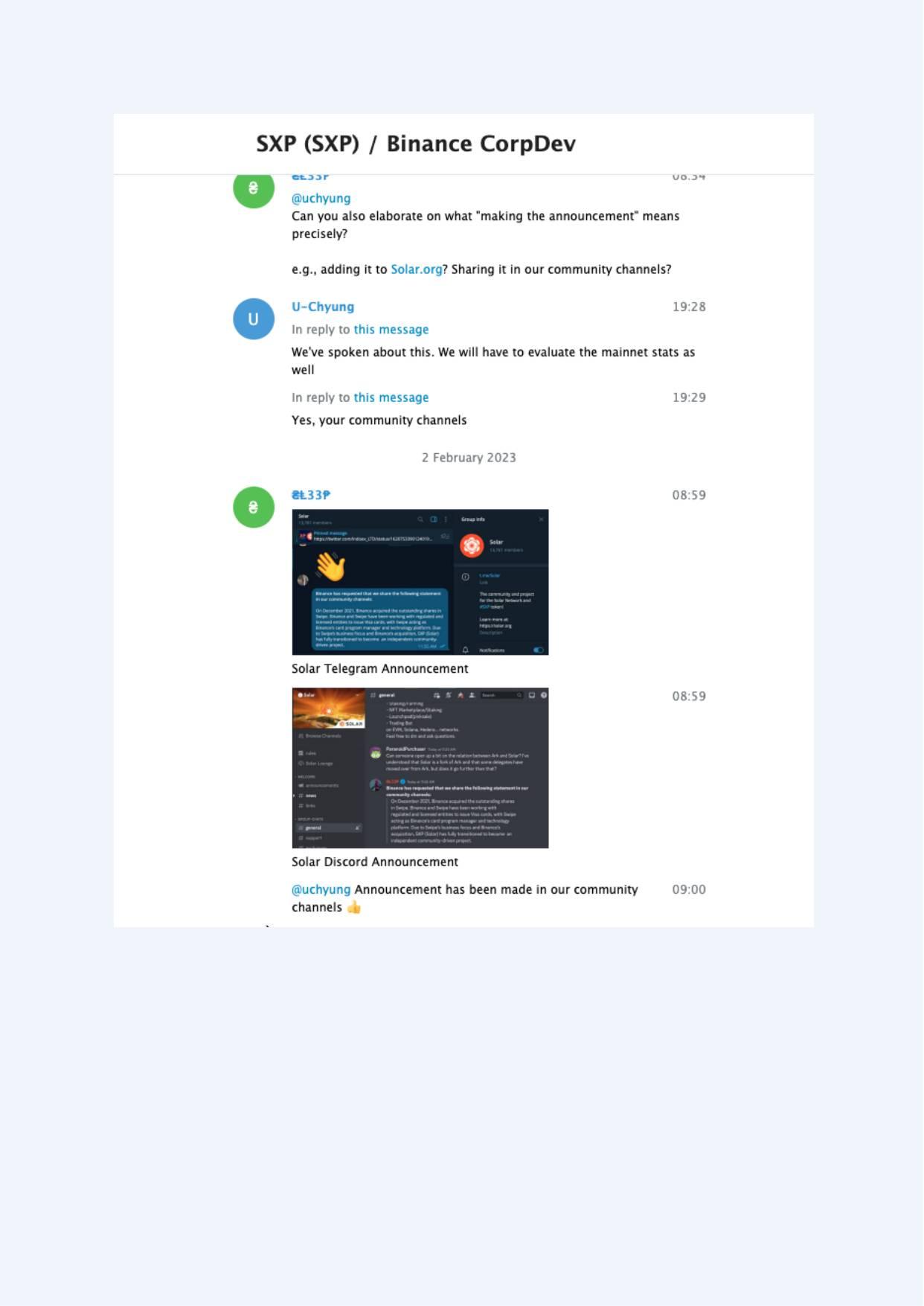

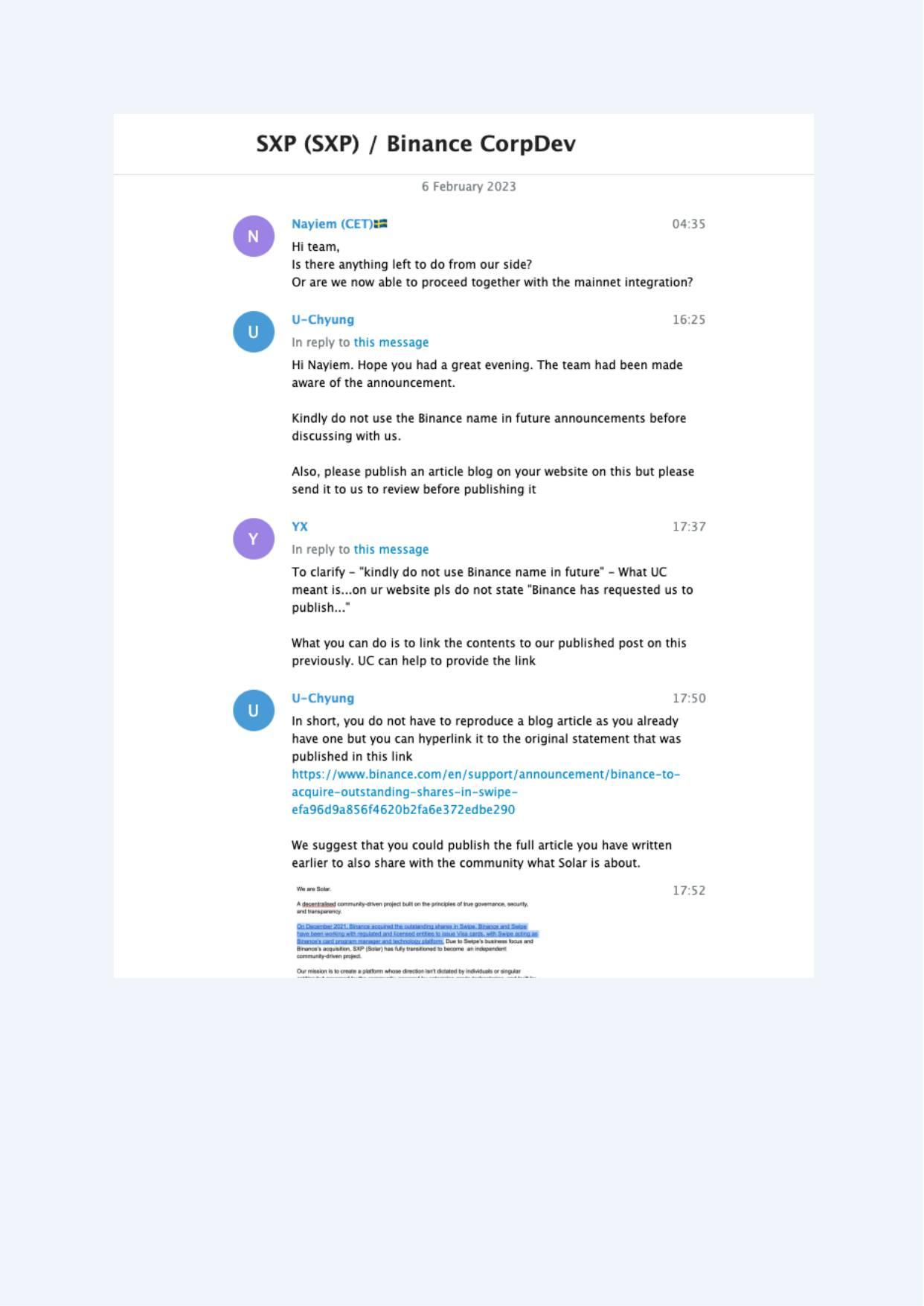

Screenshots show requests for draft review of public announcements, including references to Solar as a “community-driven project” (Exhibit A-037). Subsequent Binance announcements referenced that messaging (Public Sources P5, P7).

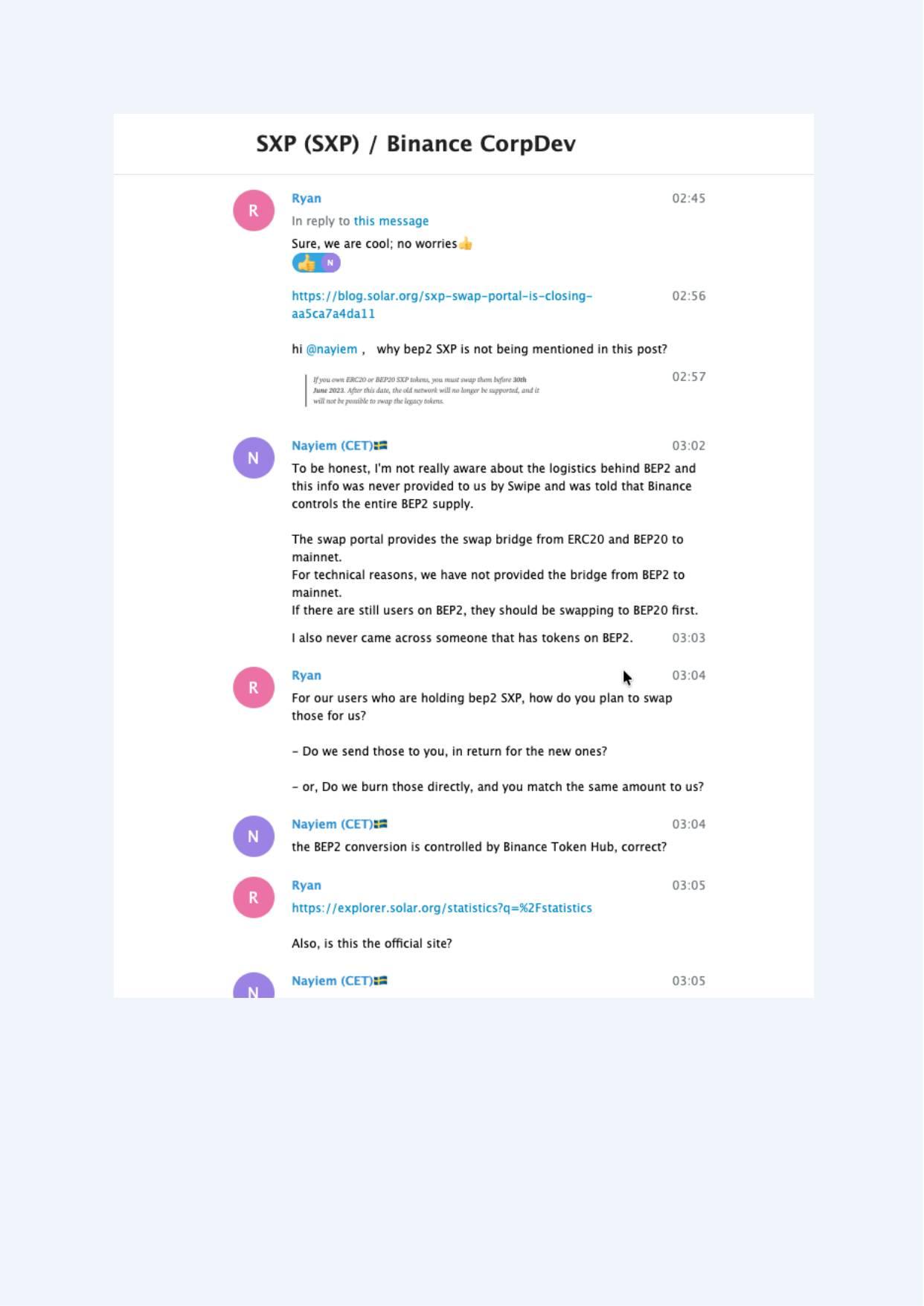

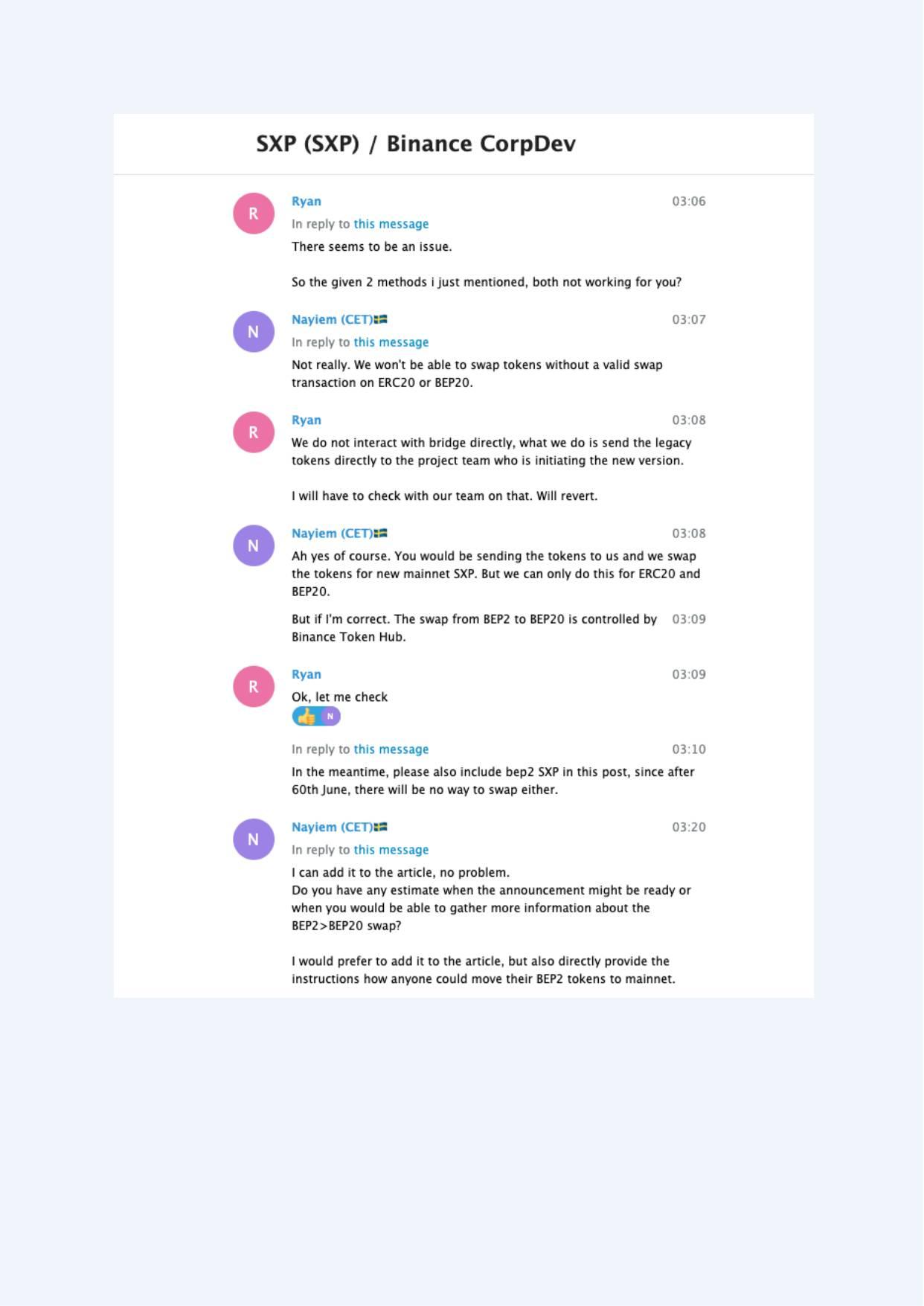

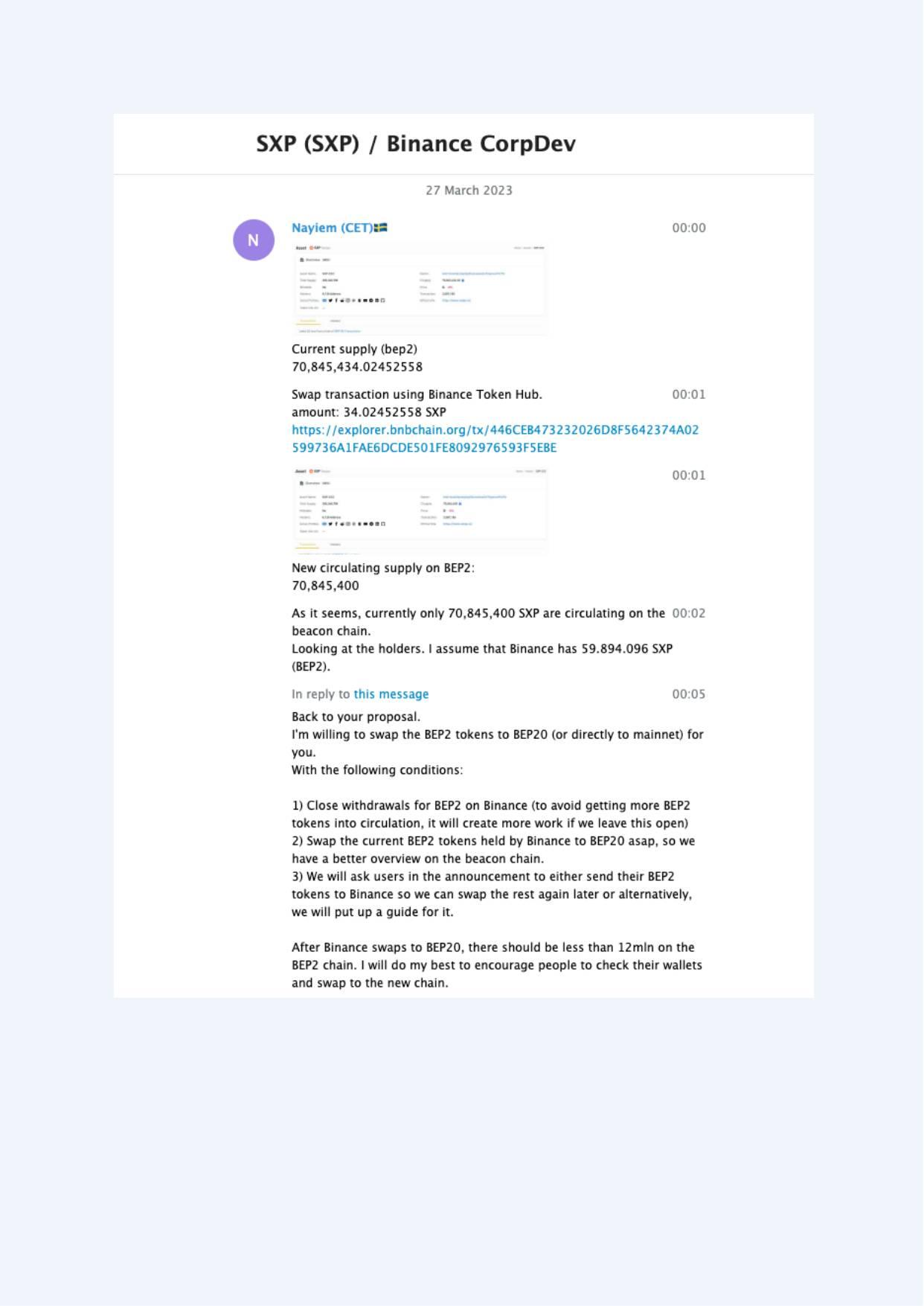

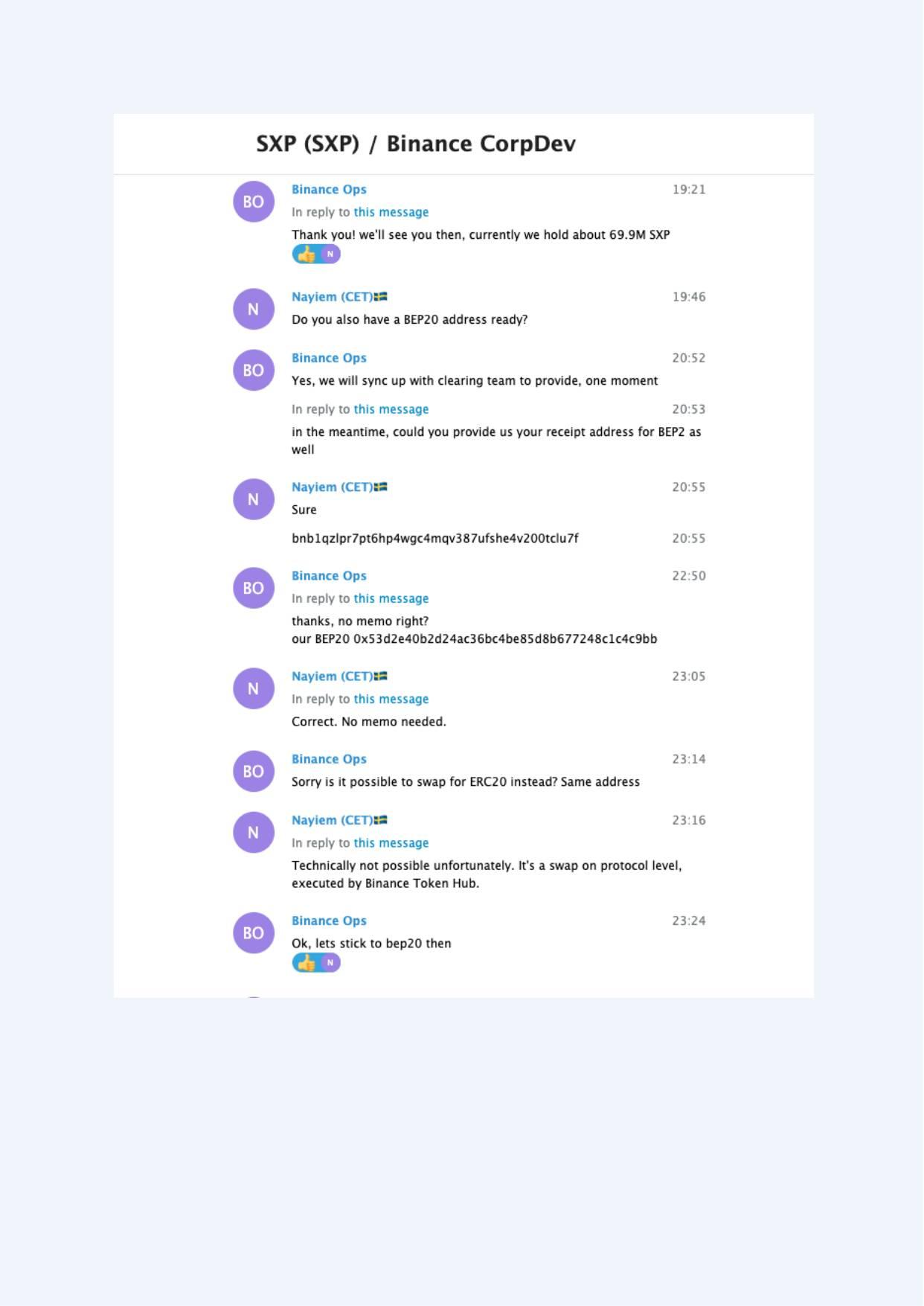

BEP2 / BEP20 Infrastructure

Solar leadership sought clarification regarding Binance Token Hub control over BEP2 conversions (Exhibit A-055). Binance announced BEP2 and BEP20 deposit and withdrawal support for SXP in October 2020 (Public Source P3).

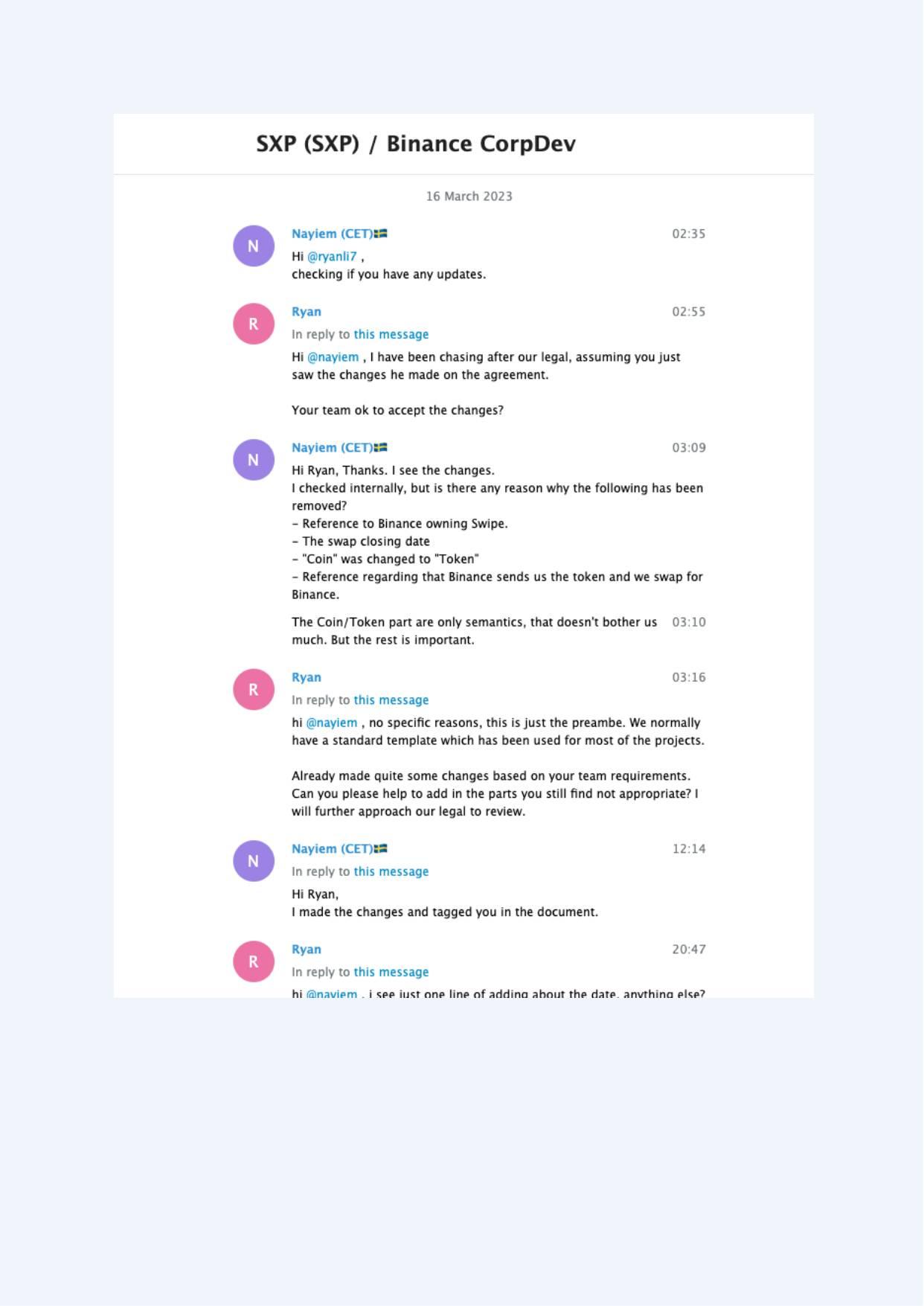

March 2023 Draft Agreement (Document D2)

The draft agreement titled Mainnet Token Swap Guarantee with Deposit contained provisions that a community reader might reasonably view as heavily weighted toward one party. Examples include:

framing Solar as an independent community-driven blockchain following Binance’s acquisition of Swipe,

broad reimbursement obligations,

unilateral rights to halt swaps or retain deposits under specified events,

extensive reporting and notification requirements,

long-term reputation and confidentiality provisions, and

Singapore law and arbitration clauses.

These provisions are referenced for context and are paraphrased for accessibility, with section references provided in Appendix B for verification.

Closing Note

This document is intended to provide historical context and explain decisions taken under constraints as they were understood at the time. It does not allege wrongdoing, assert claims, or invite action. Any further discussion of these matters would occur only through appropriate formal channels.

My last response to Binance (27 November 2025):

Chronological timeline

The full chronology of events (2018–2026), with primary-source citations, is maintained on the History & Transparency page. The selected timeline in the original document is included in the downloadable report above.

Appendix A — Screenshot exhibits

82 screenshots compiled from the communications (“Binance Proof”). Click any exhibit to open it full-size. Raw chat exports are excluded; these are the screenshots referenced throughout the report.